TeamLease Services FY26: The ₹143 Crore Cash Illusion and the Great Margins Diet

Section 1 — At a Glance

The relationship between structural business transformations and headline accounting performance is rarely straightforward. TeamLease Services Limited’s financial results for the fiscal year ended March 31, 2026, demonstrate how a single, material non-recurring liquidity event can alter surface-level earnings metrics while leaving core operational constraints unaddressed. For the full year FY26, the company reported an apparently robust 33% increase in consolidated profit after tax to ₹147 crore, supported by an operating revenue expansion of 6% to ₹11,791 crore.

However, a deeper evaluation of the quality of earnings reveals that the primary catalyst for this bottom-line acceleration was not systemic margin optimization, but rather a massive ₹143.1 crore income tax refund received in the final quarter.

This structural divergence highlights a critical reality for investors: net profit expansion driven by balance sheet corrections must never be conflated with secular operating leverage. While the headline numbers indicate a major cyclical recovery, the underlying general staffing volume contracted by a net 5,500 associates over the fiscal year, primarily due to the full-quarter impact of a large NBFC client insourcing its workforce.

Net Headcount Variance: -5,500 Associates Operating Profit Margin: 1.33%

Despite the volume compression, management maintained a positive stance, announcing a ₹238 crore equity share buyback at a premium price of ₹1,600 per share. This allocation absorbs nearly 40% of the company’s accumulated free cash balance of ₹600 crore, signaling a clear strategic attempt to support equity valuations. Meanwhile, persistent thin operating margins of 1.33% and deep systemic regulatory claims totaling over ₹570 crore across employee provident fund and indirect tax channels continue to pose a long-term capital preservation risk.

Section 2 — Introduction

TeamLease Services Limited functions essentially as a specialized, high-velocity human utility pipeline. The company operates a business model structured around the mass formalization of India’s unorganized white-collar and blue-collar labor pool. By managing recruitment, deployment, payroll administration, and complex regulatory compliance frameworks for third-party corporations, TeamLease acts as a friction-reducing intermediary within the domestic corporate ecosystem.

Strategically, the company has spent the last 25 years scaling up an infrastructure designed to handle immense volumes of human capital. However, the business faces an enduring architectural challenge: it is structurally restricted to low single-digit operating margins.

In response to this ceiling, the corporate strategy has shifted toward an inorganic expansion playbook. Throughout fiscal 2025 and 2026, the company executed several equity acquisitions, including an 80% stake in Ikigai Enablers in Singapore to expand its IT staffing footprint, alongside full control of TSR Darashaw and a strategic position in Crystal HR. The long-term hypothesis rests on migrating from simple transactional staffing toward specialized tech-enabled human resource ecosystems. Whether these high-margin software-as-a-service expansions can scale fast enough to move the needle on a multi-thousand-crore consolidated revenue base remains the primary open question for long-term equity holders.

Section 3 — Business Model: WTF Do They Even Do?

To understand TeamLease, one must stop thinking of it as a corporate entity and start viewing it as a massive, hyper-automated digital clearing house for human bodies. They are a “people supply chain” factory. Their core operation consists of taking thousands of fresh-faced workers, handling their payroll, shielding enterprise clients from labor law headaches, and collecting a razor-thin fee for the trouble.

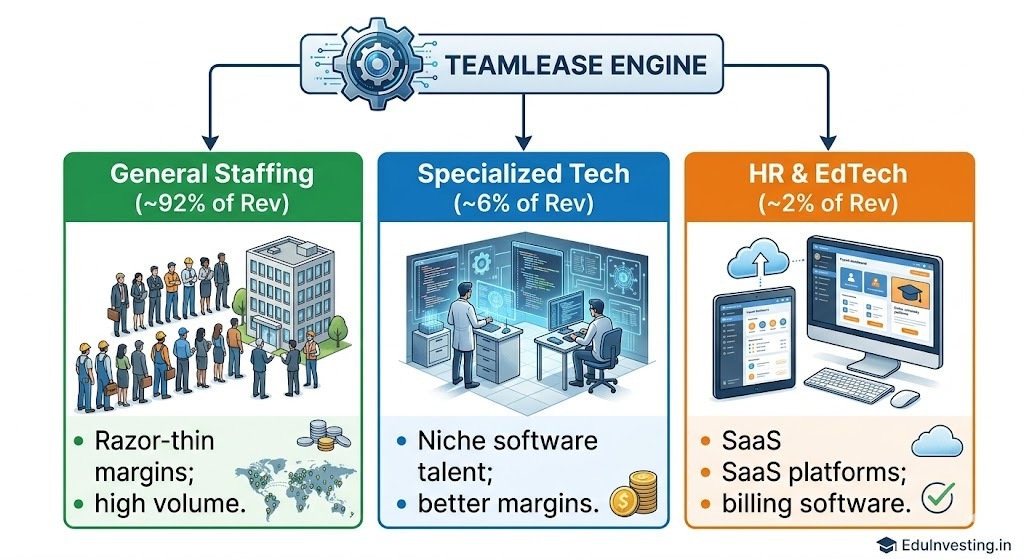

The corporate portfolio is split into three distinct universes of varying financial quality:

General Staffing & Allied Services: This is the absolute muscle of the operation, contributing approximately 92% of FY26 operating revenue. It is a game of pure scale and low leverage, moving 2.86 lakh associates across 7,500 domestic locations.

Specialized Staffing Services: Contributing about 6% of revenue, this division leases niche software developers and telecom engineers to multinational Global Capability Centers (GCCs). This is where the actual double-digit margins live, but the volume is restricted to just 7,500 highly compensated heads.

Other HR Services: A tiny 2% sliver of the top-line pie that bundles together educational technology platforms, compliance automation tools, and SaaS payroll software. It serves as management’s premium narrative center, despite currently acting as a roundoff error on the consolidated profit statement.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Headline Performance Metrics

Metric

Q4 FY26

Q3 FY26

QoQ

Q4 FY25

YoY

FY26

FY25

YoY

Operating Revenue

2,925.0

2,990.0

-2.18%

2,858.0

2.34%

11,791.0

11,156.0

5.69%

EBITDA

46.0

43.0

6.98%

48.0

-4.17%

158.0

138.0

14.49%

Profit Before Tax

52.0

49.0

6.12%

40.0

30.00%

156.0

115.0

35.65%

Profit After Tax

46.0

48.0

-4.17%

38.0

21.05%

147.0

110.0

33.64%

Reported EPS (₹)

26.19

24.88

5.27%

16.39

59.80%

83.30

64.86

28.43%

Note: Quarterly table metrics adapt strictly to locked data fields; EPS calculations reflect actual weighted equity shares outstanding across corresponding periods.

What is Management Promising in the Coming Quarters?

The incoming executive leadership, directed by newly appointed Managing Director and CEO Suparna Mitra, spent the final earnings call attempting to detach the company’s underlying performance narrative from absolute headcount declines. Management explicitly detailed a structural margin cleanup plan scheduled for the first half of fiscal 2027. Specifically, the company is preparing to execute a planned exit of approximately 10,000 low-markup, negative-contribution associate contracts across the General Staffing and Degree Apprenticeship portfolios. The CEO stated that this volume contraction will create “no net margin impact” on gross dollar collection, but will visually clean up operational efficiency metrics.

Furthermore, the Chief Financial Officer communicated high structural confidence regarding profitability targets, stating that TeamLease expects to “maintain year-on-year EBITDA growth