The financial landscape of the fluorochemical sector is witnessing a high-stakes transition, and Stallion India Fluorochemicals Ltd is positioning itself as the aggressive protagonist. While the broader market grapples with supply chain volatility and cooling demand in certain segments, Stallion has posted a net profit of ₹43.84 crore for FY26, a massive 35.6% jump over the previous year. This isn’t just organic growth; it is the result of a calculated pivot from being a mere middleman to a backward-integrated manufacturer.

The company is currently sitting on a powder keg of expansion. With a ₹364 crore rights issue recently concluded and a massive 10,000 MTPA R-32 plant in Bhilwara on the horizon, the management is betting the farm on self-reliance. Investors are watching closely as the company attempts to double its footprint while maintaining a nearly debt-free balance sheet—a rare feat in a capital-intensive industry. However, the drop in promoter holding to 47.8% and the repeated delays in the Khalapur helium project serve as a grim reminder that even the boldest plans face friction.

1. At a Glance

Stallion India is no longer just “selling gas.” It is evolving into a specialized infrastructure play within the high-precision chemical space. The numbers tell a story of rapid scale: revenue grew to ₹431 crore in FY26, yet the real intrigue lies in the margins. By aggressively targeting the aftermarket segment, where it claims a dominant 80% market share, Stallion is extracting higher profitability than those tethered solely to low-margin OEM contracts.

But let’s talk about the elephants in the room. The company has a low Return on Equity (ROE) of 8.93%, which is underwhelming for a company growing its bottom line by 35%. Furthermore, the promoter group has seen its holding slashed from 67.9% to 47.8% within a year. While the management attributes this to funding requirements and “failed preferential routes,” such a sharp decline often leaves seasoned auditors squinting at the fine print.

The strategy is clear: use the proceeds from the IPO and the massive ₹364 crore Rights Issue to build a captive manufacturing base for R-32 gas. If successful, they stop importing expensive molecules from China and start dictating their own margins. If they stumble on the October 2026 commissioning deadline, they’ll be left with a bloated asset base and underutilized capacity. The stakes are quantified: they are chasing a 30-35% CAGR target, but the path is littered with regulatory hurdles and the inherent volatility of the chemical cycle.

2. Introduction

Stallion India Fluorochemicals started its journey in 2002, initially acting as a vital cog in the supply chain for refrigerant gases. For years, it operated as a “processor”—buying bulk gases, blending them into specific formulations, and distributing them across India. It was a safe, service-oriented business.

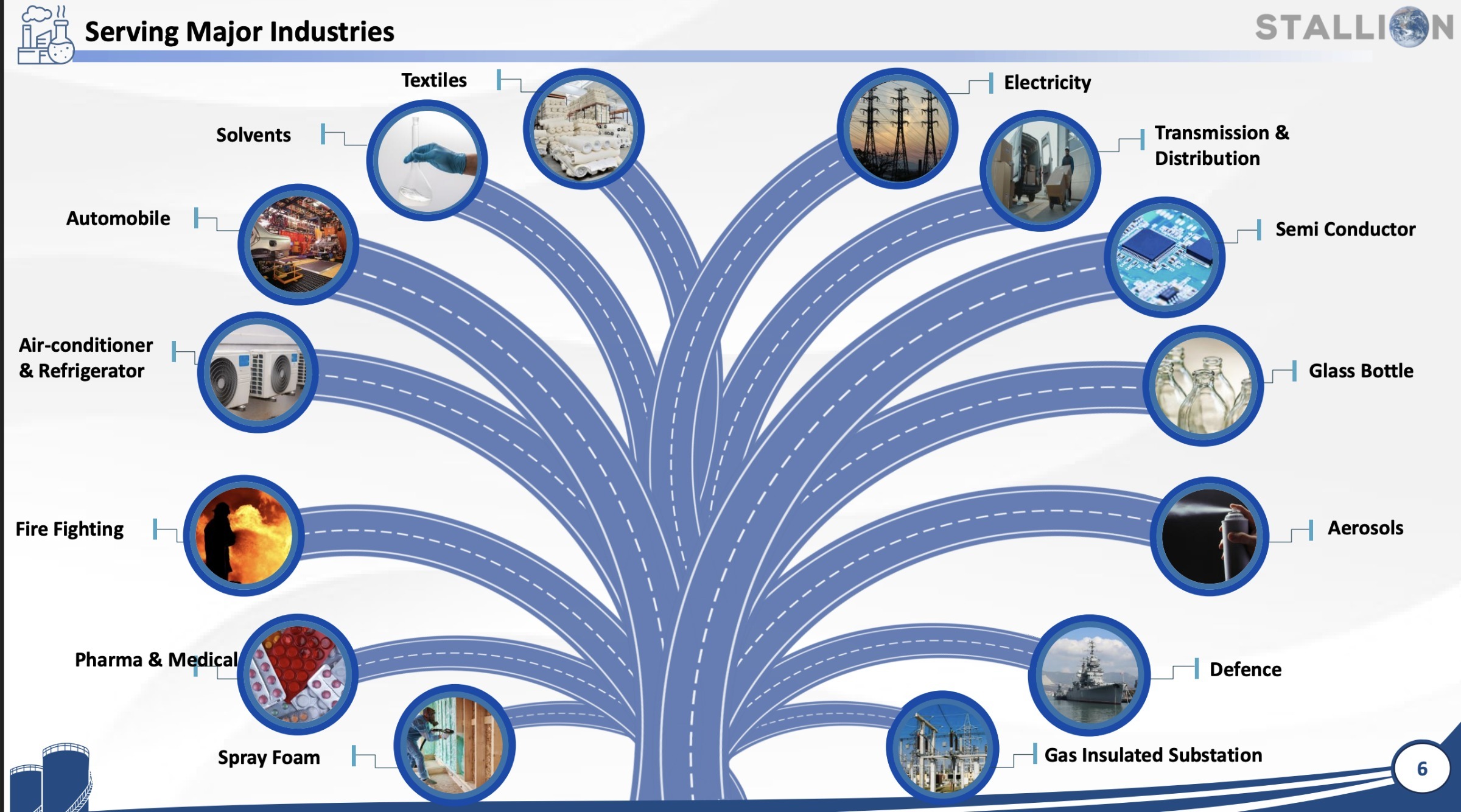

That “safe” era ended recently. Today, the company is aggressively transforming into a manufacturer. They serve over 200 customers across 15+ industries, including critical sectors like defense, pharmaceuticals, and the burgeoning semiconductor industry. Their footprint spans four operational facilities in Maharashtra, Rajasthan, and Haryana, with a fifth mega-facility in Andhra Pradesh nearing completion.

The narrative here is one of import substitution. India’s reliance on Chinese imports for refrigerant molecules is a strategic weakness that Stallion aims to exploit. By moving into HFOs (Hydrofluoroolefins) and High-Purity Helium, they are moving up the value chain where the technical barriers to entry are high and the competitors are few.

3. Business Model – WTF Do They Even Do?

To the uninitiated, Stallion looks like a logistics company with fancy tanks. In reality, they are “Gas Chemists.” They take raw refrigerant molecules (the stuff that makes your AC cold) and industrial gases, then “debulk” them from massive ISO tanks into smaller, usable cylinders.

Their secret sauce is Blending. Many modern cooling systems don’t run on a single gas; they run on precise cocktails. Stallion owns the recipes and the blending infrastructure to create these. They also produce ancillary products like washer pumps and refrigerant cans, ensuring they own the “last mile” of the HVAC (Heating, Ventilation, and Air Conditioning) maintenance market.

The Roast: They essentially play a high-stakes game of “Chemistry Tetris.” They buy molecules from global giants, mix them up, and sell them to people whose ACs have stopped working. It’s a great business until your raw material costs—which are mostly imported—spike because of a trade war or a shipping container shortage in the Middle East.

Are they a tech-leader or just a very efficient warehouse operator? The upcoming R-32 plant will provide the final answer.

4. Financials Overview

The latest results show a company that is growing fast but facing quarterly turbulence. While the annual numbers are stellar, the latest quarter saw a dip in sales compared to the previous year.

Performance Snapshot (Figures in ₹ Crore)

| Metric | Latest Quarter (Mar 2026) | Same Quarter Last Year (YoY) | Previous Quarter (QoQ) |

| Revenue | 110.00 | 152.00 | 110.00 |

| EBITDA | 16.00 | 19.00 | 12.00 |

| PAT | 11.00 | 13.00 | 11.00 |

| EPS (Annualised) | 3.76 | 4.56 | 3.84 |

Note: Annualised EPS for Q4 is taken as the actual full-year EPS of ₹3.78.

Financial Wisdom: Revenue is vanity, profit is sanity, but cash is reality. Stallion’s EBITDA margins have hovered around 13-15%. Management “walked the talk” on their FY26 guidance, hitting the ₹430 Cr revenue and ₹40 Cr PAT targets they set earlier in the year. However, the 27% YoY drop in quarterly sales suggests that the “base business” might be hitting a temporary ceiling until the new capacities kick in.

5. Valuation Discussion – Fair Value Range

Calculating the value of a company in transition requires looking at where they will be once the Bhilwara plant is live.

Method 1: P/E Multiple

- Current EPS: ₹3.78

- Industry Average P/E: 38.0

- Stallion Current P/E: 38.4

- Valuation: The stock is trading exactly at par with its peers (Linde India, Refex). It is “fairly priced” based on historical earnings.

Method 2: EV/EBITDA

- Enterprise Value (EV): ₹1,282 Cr

- EBITDA (FY26): ₹58 Cr

- Multiple: 22.1x

- Compared to high-growth specialty chemical peers, this multiple is aggressive but supported by the 35% profit CAGR.

Method 3: DCF (Discounted Cash Flow)

Considering the management’s projection of ₹550 Cr revenue from R-32 in FY27 and a 24% PAT margin, the forward-looking cash flows are significantly higher than today’s reality. When we discount these back at a 12% cost of capital, we see a value range that factors in the execution risk of the new plant.

Fair Value Range: ₹135 – ₹165

Disclaimer: This fair value range is for educational purposes only and is not investment advice.

6. What’s Cooking – News, Triggers, Drama

The drama at Stallion is more intense than a soap opera.

- The Rights Issue Saga: The company just closed a massive ₹364 Crore Rights Issue. Why? Because the stock was hitting upper circuits so fast that a “preferential allotment” became legally impossible.

- Helium Delays: The Khalapur helium plant has been delayed because the management decided to upgrade the system from 200 bar to 300 bar. They claim it’s for “global standards,” but investors hate schedule slips.

- The R-32 Milestone: They finally secured the Environmental Clearance (EC) for the 10,000 MTPA plant. This is the “Golden Ticket.” Without this, the Rights Issue money would just be sitting in a bank.

Question for the readers: Do you trust a management that changes plant designs mid-construction to “upgrade standards,” or is that just a cover for poor initial planning?

7. Balance Sheet

The balance sheet has undergone a massive expansion following the Rights Issue and IPO.

| Row | Mar 2025 (₹ Cr) | Mar 2026 (₹ Cr) |

| Total Assets | 334.00 | 737.00 |

| Net Worth | 301.00 | 681.00 |

| Borrowings | 2.00 | 34.00 |

| Other Liabilities | 31.00 | 22.00 |

| Total Liabilities | 334.00 | 737.00 |

- The Net Worth has more than doubled, thanks to the massive infusion of capital.

- Borrowings are negligible; this is basically a debt-free fortress.

- The “Other Assets” (likely cash from the Rights Issue) is a staggering ₹667 Cr. They are armed for a massive capex war.

8. Cash Flow – Sab Number Game Hai

The cash flow statement reveals the aggressive reinvestment phase the company is in.

| (Figures in ₹ Cr) | Mar 2024 | Mar 2025 | Mar 2026 |

| Operating Cash Flow (CFO) | -73 | -13 | 39 |

| Investing Cash Flow | -13 | -20 | -253 |

| Financing Cash Flow | 76 | 76 | 667 |

Stallion was a “cash burner” until FY25, primarily because their money was locked in working capital and small capex. In FY26, they finally generated ₹39 Cr from operations. However, look at that ₹253 Cr investing outflow—that’s the sound of money being poured into concrete and stainless steel.

9. Ratios – Sexy or Stressy?

| Ratio | Value | Verdict |

| ROE | 8.93% | Stressy. Too low for a growth stock. |

| ROCE | 11.8% | Meh. Needs to improve post-integration. |

| Debt to Equity | 0.05 | Sexy. Cleaner than a new lab coat. |

| Debtor Days | 66 | Improving. Down from 111 days. |

The low ROE is a side effect of the “Equity Overhang.” They just raised a ton of money, which expands the equity base before the profits from that money start flowing. It’s a classic “wait and watch” scenario.

10. P&L Breakdown – Show Me the Money

| (Figures in ₹ Cr) | Mar 2024 | Mar 2025 | Mar 2026 |

| Revenue | 233 | 377 | 431 |

| EBITDA | 24 | 48 | 58 |

| PAT | 15 | 32 | 44 |

The revenue has grown like a teenager on a growth spurt—up nearly 85% in two years. The PAT margins are expanding from 6% to 10%. Management wants to take this to 24%. That’s like saying you’re going to run a marathon in under two hours—bold, but the world is skeptical until they see the finish line.

11. Peer Comparison

| Company | Sales Qtr (₹ Cr) | PAT Qtr (₹ Cr) | P/E |

| Linde India | 701 | 191 | 108.0 |

| Refex Industries | 576 | 52 | 20.7 |

| Stallion India | 110 | 11 | 38.4 |

Linde India is the undisputed king with a P/E that suggests it’s powered by magic. Stallion is the “hungry underdog.” It’s much smaller than Refex but is valued more aggressively. Refex is winning the revenue race, but Stallion is crying about “quality of earnings” and “backward integration.”

12. Miscellaneous – Shareholding and Promoters

The shareholding pattern is where the “Auditor” in me gets nervous.

| Category | Mar 2025 | Mar 2026 |

| Promoters | 67.9% | 47.8% |

| FIIs | 3.3% | 1.8% |

| DIIs | 4.7% | 4.0% |

| Public | 24.1% | 46.4% |

Promoter Roast: MD Shazad Rustomji sold a chunk of his stake to provide “interest-free loans” to the company to jumpstart the R-32 plant. While that sounds noble, the public now owns nearly half the company. It’s starting to look less like a family business and more like a public experiment.

13. Corporate Governance – Angels or Devils?

The governance record is a mixed bag. On the plus side, they appointed a new Independent Director (Swati Ghosh) and maintain an unmodified audit report. On the down side, the Monitoring Agency (CARE) flagged a ₹3.99 crore excess issue expense and capex delays.

Management’s habit of “varying the use of IPO proceeds” (moving money from capex to land acquisition) via postal ballots shows they are “flexible,” which can be a polite word for “making it up as they go.”

14. Industry Roast and Macro Context

The fluorochemical industry is currently a geopolitical football. With the Montreal Protocol forcing a shift from old HFCs to new HFOs, companies have to constantly reinvent their product lines or go extinct.

The Sarcasm: Every chemical company in India currently claims they are the next “import substitution” hero. The reality? They all buy their precursor chemicals from the same three factories in China. If China sneezes, the Indian fluorochemical sector gets pneumonia. The “Semiconductor Gas” buzz is the latest carrot being dangled in front of investors—everyone is “planning” to enter the segment, but very few have actually shipped a cylinder to a fabrication plant.

15. EduInvesting Verdict

Stallion India is a classic “Execution Play.”

Past Performance: They have delivered on their revenue guidance and successfully transitioned into a listed entity with a clean, debt-free balance sheet. Their grip on the aftermarket segment is a genuine competitive advantage.

The Headwinds: They are facing massive dilution. The public float has doubled, and the promoter skin in the game has thinned. Any further delay in the Bhilwara plant or the Andhra facility will be punished severely by the market.

SWOT Analysis:

- Strengths: Debt-free; 80% aftermarket market share; backward integration roadmap.

- Weaknesses: Low ROE; high dependence on Chinese raw materials; promoter stake dilution.

- Opportunities: Entry into high-margin liquid helium and semiconductor gases.

- Threats: Regulatory changes in refrigerant gases; execution delays in mega-projects.

Final Thought: Stallion is no longer a small-time blender. It has the cash and the permits to become a significant manufacturing player. However, in the stock market, you don’t get prizes for “planning”—you get prizes for “commissioning.” October 2026 is the date that will define this company’s decade.

Fair Value Range Disclaimer:

This fair value range is for educational purposes only and is not investment advice. All data is based on official filings and latest available results.