Saatvik Green Energy FY26: The Sun Shines Brightest on fixed-price contracts?

Section 1 — At a Glance

The transition from a domestic solar module assembler to an integrated clean energy player is rarely a quiet affair. For Saatvik Green Energy Limited, the fiscal year ended March 31, 2026, delivered a stunning top-line expansion that captured institutional attention, even as sharp raw material and foreign exchange crosswinds exposed the structural vulnerability of its manufacturing base. Total annual sales surged by an extraordinary 111% year-on-year to reach ₹4,548.44 crore, up from ₹2,158.39 crore in FY25, riding a wave of unprecedented domestic utility demand fueled by aggressive regulatory mandates. Yet beneath this blistering growth engine lies a clear warning signal: operating profit margins collapsed sequentially in the final quarter of the year, sliding to a meager 7% as a sudden shock in commodity input prices collided with long-duration, fixed-price procurement contracts.

The company’s capital structure underwent a foundational resetting following its initial public offering on September 26, 2025, which injected ₹700 crore in fresh equity, lifting its net worth and drastically bringing down its headline debt-to-equity ratio from a precarious 1.34x to a far more palatable 0.65x. However, the cash flows paint a far more restrictive reality. Massive capital deployment into backward integration lines turned free cash flow deeply negative, while working capital requirements ballooned as state-backed power undertakings elongated collection cycles to over 90 days. Volume expansion cannot completely mask processing vulnerabilities. When multi-year supply commitments outpace structural raw material cover, top-line hyper-growth acts as a double-edged sword that amplifies commodity price volatility directly into structural margin compression.

Section 2 — Introduction

Saatvik Green Energy Limited, incorporated in 2015, has spent its first decade scaling up from a modest 125 MW regional module supplier in Ambala, Haryana, into one of India’s most ambitious private sector solar equipment manufacturers. Operating at a current module capacity of 4.80 GW, the company manufactures high-efficiency solar photovoltaic (PV) modules, primarily focusing on Mono PERC and next-generation N-TopCon technologies.

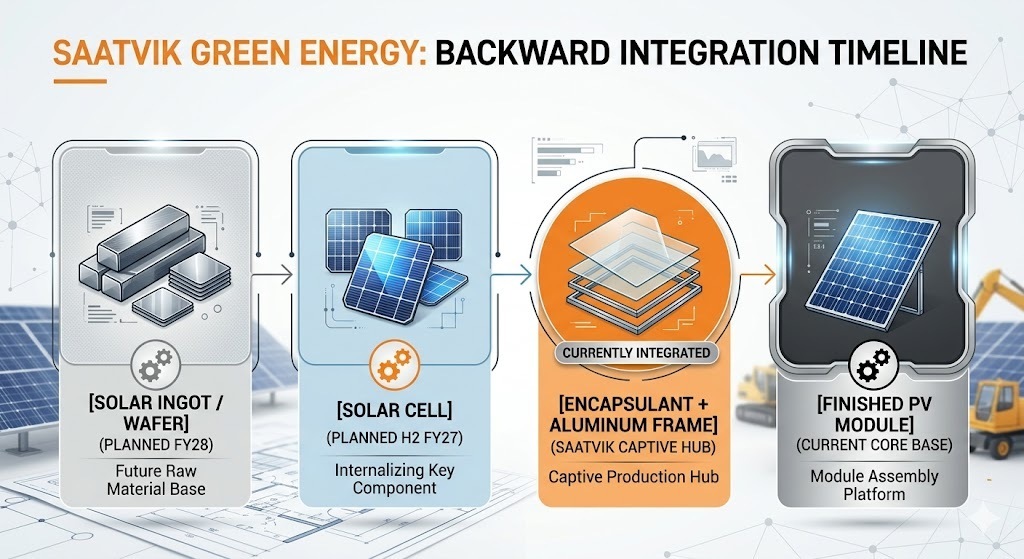

The company’s operational center revolves around its massive single-location manufacturing hub in Ambala, which spans over seven lakh square feet. While its historical focus was purely on assembling imported cells into completed solar panels for large-scale utility developers, Saatvik has recently embarked on an aggressive corporate transformation. The capital raised during its listing is being entirely thrown into the furnace of backward integration, as the company seeks to build massive solar cell, ingot, and wafer plants to insulate itself from global supply chain shocks. It is a high-stakes race to stop being a simple assembler and start being a true vertically integrated clean technology platform.

Section 3 — Business Model: WTF Do They Even Do?

At its core, Saatvik Green Energy is a giant solar kitchen. They buy incredibly expensive, highly sensitive solar cells—mostly from international suppliers—and wrap them inside protective sheets, frame them in aluminum, and sell them as finished solar modules.

The revenue mix for FY25 tells a very specific story of where the money actually comes from:

Manufactured Solar PV Modules: 70.5% of the top line. This is their bread and butter.

Traded Goods: 26.0%. Essentially buying someone else’s equipment and flipping it for a quick trading margin.

Engineering, Procurement, and Construction (EPC) Projects: A tiny 3.4%.

Management has openly admitted that EPC is not their core business, treating it as an elite, high-margin hobby where they only accept projects that don’t give them operational headaches. Product-wise, the company has completed a massive migration away from legacy technology: next-gen N-TopCon solar modules made up 57% of their FY25 product mix, while older Mono PERC modules stood at 39%.

The client roster includes corporate heavyweights like Shree Cement, Megha Engineering, and Dalmia Bharat. However, diversification is a work in progress: the top ten customers command a massive 58% of total revenue. Perhaps the most hilarious part of their business design is that despite being a renewable energy darling, 99.88% of their customer base sits squarely in the private sector, leaving them practically untouched by direct government utility orders, though completely dependent on government policy.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4 FY26)

YoY (vs Q4 FY25)

QoQ (vs Q3 FY26)

Revenue

₹1,607.66

+74.95%

+27.90%

EBITDA / Operating Profit

₹107.64

-31.46%

-28.78%

PAT (Net Profit)

₹60.61

-36.00%

-37.46%

EPS (Reported)

₹4.77

-43.55%

-37.48%

A multi-year evaluation confirms that quarter-on-quarter earnings quality can be a fickle beast when macro variables misbehave. While Saatvik’s full-year performance looks like a vertical line going up, Q4 FY26 was an absolute horror show for operational efficiency. Revenue reached a record quarterly high of ₹1,607.66 crore, but operating profits collapsed by over 31% year-on-year.

Did Management Walk the Talk?

During the May 2026 earnings call, management had to face the music regarding this margin destruction. The CEO noted that a structural margin drop in the fourth quarter was driven by an extraordinary convergence of input cost and forex shocks. Specifically, solar cell procurement costs exploded because of a massive surge in global silver prices, alongside sharp price increases in copper and aluminum frames.

Worse, the outbreak of geopolitical tensions on February 20 caught their long-duration, fixed-price domestic contracts completely unprotected. “It was simply not possible for us to pass on the increase to customers immediately,” management