Blue Water Logistics Ltd Mar 2026: The ₹141 Crore Collection Crisis

Section 1 — At a Glance

The financial year ended March 31, 2026, presents an extraordinary paradox of blistering topline expansion and severe, systemic balance-sheet strain for the recently listed entity. Headline revenue skyrocketed by an astonishing 96.8% year-on-year to reach ₹386.02 crore, driven by a dramatic surge in shipping volumes, strategic fleet expansion, and high-value international logistics alignments. Profit after tax followed a similar hyper-growth trajectory, expanding by 135.4% to hit ₹25.21 crore. On paper, these metrics paint the picture of a newly public micro-cap comfortably outrunning its industry peers.

However, beneath this polished surface of structural outperformance lies a deeply concerning working-capital reality. Trade receivables have ballooned out of all proportion, surging from ₹45.15 crore to a staggering ₹141.43 crore in a single year. This massive cash lockup means that nearly 37% of the entire annual revenue exists purely as uncollected promises written in ledger books.

The operational consequences are clear. Cash flow from operating activities collapsed deep into negative territory, hitting a record deficit of negative ₹53.43 crore. The business is effectively generating massive accounting profits while burning physical cash to sustain its regular daily operations. To bridge this wide liquidity chasm, total bank borrowings were aggressively expanded from ₹36.73 crore to ₹107.53 crore.

When credit-fueled growth outpaces actual cash collections, a business model transitions from high-performing to dangerously fragile. Investors must now carefully evaluate whether this remarkable volume surge is a sustainable structural expansion, or an aggressive, credit-diluted pursuit of market share that compromises the company’s underlying financial stability.

Section 2 — Introduction

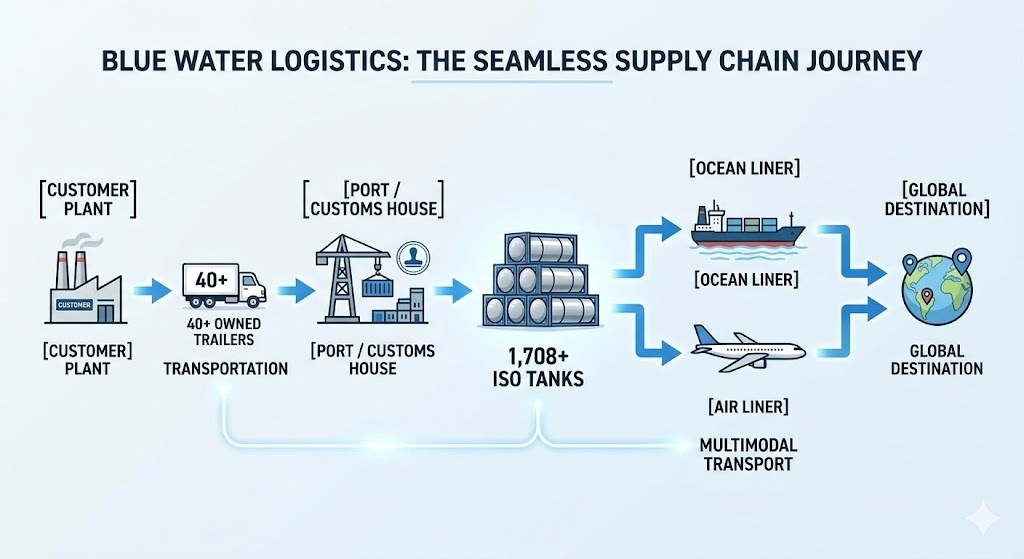

Blue Water Logistics Ltd has officially completed its transition from a humble, localized partnership firm to a newly listed corporate entity on the public markets. Operating out of its corporate headquarters in Hyderabad, the company has spent the last decade building an integrated logistics and multimodal supply chain network across India and key global hubs.

The past year marked a watershed moment, anchored by its initial public offering on the exchange, which injected much-needed growth capital into the balance sheet. Management used these fresh funds to aggressively scale up its asset base, moving away from third-party rental assets and establishing a formidable, owned infrastructure of heavy transport equipment. This aggressive pivot has allowed the company to chase massive volume contracts across ten major Indian states, handling end-to-end cargo movements for some of the country’s most prominent industrial manufacturers.

Yet, the primary challenge of public life is that everything is out in the open. The era of quiet, private growth is over. The financial metrics of the company must now withstand the cold, unsympathetic scrutiny of institutional analysis. The core question is no longer whether this organization can move freight across borders, but whether it can actually collect the cash from the destinations it reaches.

Section 3 — Business Model: WTF Do They Even Do?

To put it bluntly, Blue Water Logistics acts as the complex central nervous system for corporations that need to move massive quantities of physical goods from Point A to Point B without losing their sanity in customs corridors. They are an asset-backed, multimodal freight coordinator.

If a large domestic pharmaceutical or chemical manufacturer needs to ship thousands of liters of liquid compounds to the United Arab Emirates, this company handles the entire logistical journey. They dispatch one of their own 100+ specialized forty-foot container trailers to collect the cargo, pump it into one of their 1,708+ proprietary ISO tank containers, clear the dense documentation at the port via their internal Customs House Agent license, and load it onto an international ocean vessel.

The revenue engine is highly diversified yet heavily anchored, with Ocean Freight driving a dominant 70.0% of the topline, while a high-growth Air Freight vertical has quickly scaled to 13.0% of the mix thanks to a strategic partnership with international carriers. They cater to a broad industrial spectrum, ranging from volatile chemical groups to high-end fitness equipment providers. However, this extensive operation carries a clear systemic vulnerability. The business is highly dependent on a few large relationships, with the top ten customers driving more than half of the total revenue. If even one of these dominant relationships delays a payout, the entire logistical machinery experiences a financial traffic jam.