Honasa Consumer Q4 FY26: A ₹200 Crore Toxin-Free Flex

At a Glance

The narrative surrounding India’s digital-first beauty ecosystem underwent a dramatic fundamental shift during the financial year ended March 31, 2026. Headline revenues scaled new heights, touching ₹2,391.94 crore for the full year, fueled by an unrelenting volume recovery and structural shifts across legacy core categories. Yet, beneath the clean, certified-safe topicals lies an earnings engine that remains aggressively tied to the high-stakes world of performance marketing and inorganic capital deployment.

While corporate messaging spotlights sequential volume growth and a maiden payout strategy, discerning market participants are closely monitoring the balance sheet’s composition. Intangible assets and goodwill have expanded aggressively following the strategic acquisition of BTM Ventures, altering the quality of capital employed. Absolute profitability took a sharp leap upward, with annual net profit landing at ₹199.95 crore —a stark contrast to the historical volatility that characterized the company’s early fiscal years.

The primary friction point for the investment community remains the structural reconciliation of growth. The gap between reported billing mechanics and true organic underlying expansion is widening due to shifts in marketplace fulfillment channel relationships. Earnings execution is finally aligning with operational promises, but the cost of sustaining a multi-brand architecture across fragmented trade channels leaves little room for execution missteps.

Introduction

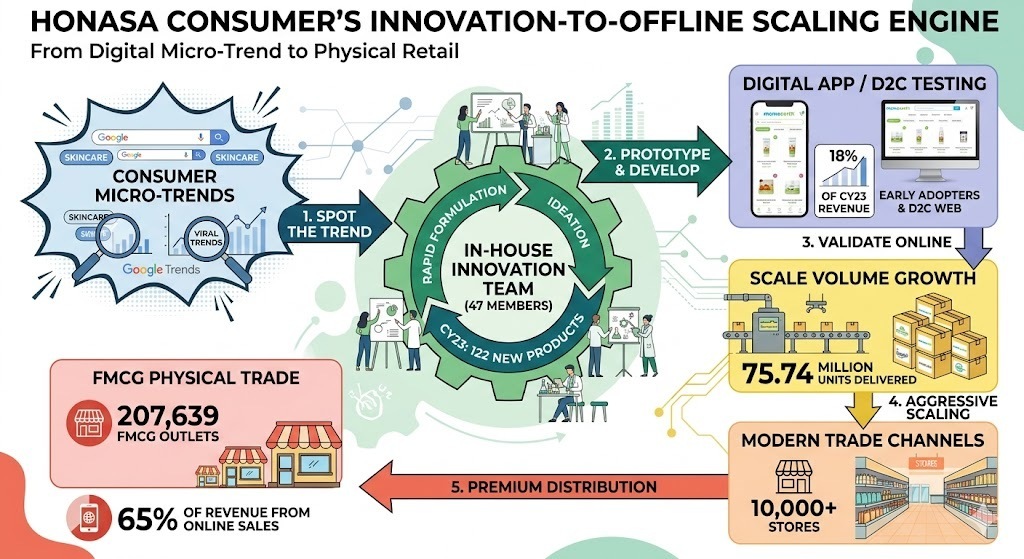

Honasa Consumer Limited has spent the last few years trying to convince the public markets that it is a serious personal care powerhouse rather than just an aggregation of viral internet trends. Operating a digital-first playbook that has now aggressively spilled onto physical general trade shelves, the entity has built its entire identity around clean, toxin-free formulations. The operational architecture is built upon rapid product experimentation cycles and a heavily institutionalized influencer amplification network.

With its flagship brand stabilizing into a mature growth phase, strategic focus has pivoted toward building a self-sustaining multi-brand portfolio. The integration of younger brands like The Derma Co., Aqualogica, and recent acquisitions represents an explicit attempt to move away from single-brand concentration risk. As the organization aggressively builds out senior management tiers to handle this multi-brand complexity, the core narrative shifts from pure customer acquisition to long-term distribution channel economics.

Business Model: WTF Do They Even Do?

At its core, Honasa functions as a rapid-prototyping factory masquerading as a beauty and personal care giant. The internal machinery relies on an in-house innovation unit that spots consumer micro-trends, concocts a formulation, and puts it up for trial with early internet adopters within weeks. If a specific serum or shampoo generates sufficient traction on digital marketplaces or D2C applications, the distribution engine moves it into traditional multi-tier physical FMCG retail networks.

The brand portfolio is neatly partitioned to capture targeted consumer cohorts: Mamaearth owns the natural, baby-safe sandbox; The Derma Co. tackles active chemical ingredients for problematic skin; Aqualogica claims clinical hydration; while BBlunt runs salon-grade hair styling. It’s an elegant “horses for courses” architecture designed to capture the modern consumer’s vanity from multiple angles. However, keeping six distinct brand narratives running simultaneously requires a staggering amount of capital spent on ad tech platforms just to maintain basic brand recall.

Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4 FY26)

YoY Change (%)

QoQ Change (%)

Revenue

₹657.08

39.48%

9.23%

EBITDA / Operating Profit

₹77.09

132.82%

17.73%

PAT

₹69.19

127.00%

37.83%

EPS

₹2.13

126.60%

38.31%

The financial performance of the fourth quarter was heavily shaped by an accounting change regarding marketplace fulfillment models. A structural shift in how transactions are settled on platforms like Flipkart caused approximately ₹25 crore of logistical charges to be netted directly off top-line revenues, with zero impact on ultimate profitability. On a true like-for-like organic basis, management noted that underlying volume growth stood at an impressive 30% for the quarter.

Did Management Walk the Talk?

During older corporate briefings, management laid out an explicit framework promising a steady 100-basis-point annual expansion in operational EBITDA margins. Looking