Happy Forgings FY26: A 30% EBITDA Margin to Soften the Blow of Your 44x Valuation

Section 1 — At a Glance

The automotive component sector frequently penalizes companies that fail to transition from low-margin commodity casting to precision engineering. Happy Forgings Limited concludes its financial year 2026 demonstrating a clear structural decoupling from traditional forging peers, anchored by an operating profit margin that breached 30.4% for the full year. Total revenue scale reached ₹1,546 crore, marking a 9.8% expansion against a backdrop of domestic macro cross-currents and slowing infrastructure spending.

However, public market participants are encountering a distinct tension between operational excellence and valuation premium. The stock commands a price-to-earnings multiple of 44.3 times, positioning its valuation well above the broader capital goods and casting peer bands. This premium places an immense burden of proof on the execution of the company’s ₹650 crore heavy forging capital expenditure cycle, which is not slated to monetize meaningfully until fiscal year 2028.

While net profit rose 12.8% to reach ₹302 crore, underlying profitability growth was subtly restricted by unhedged foreign exchange volatility, which compressed non-operating other income line items down to ₹31 crore. Cash generation metrics remain highly robust, with operating cash flow converting at 94% of trailing EBITDA, shielding the balance sheet from material leverage increases despite high asset-heavy deployment. The core vulnerability persists in the near term: asset turnover metrics have compressed to 1.0 times, indicating that capital efficiency is temporarily paying a tax to fund future capacities.

Section 2 — Introduction

Happy Forgings Limited, established in 1979 and headquartered out of the manufacturing hub of Ludhiana, Punjab, has quietly spent the last four decades executing a slow corporate migration. It has evolved from a small-scale manufacturer of basic bicycle crank arms into a safety-critical engineering enterprise.

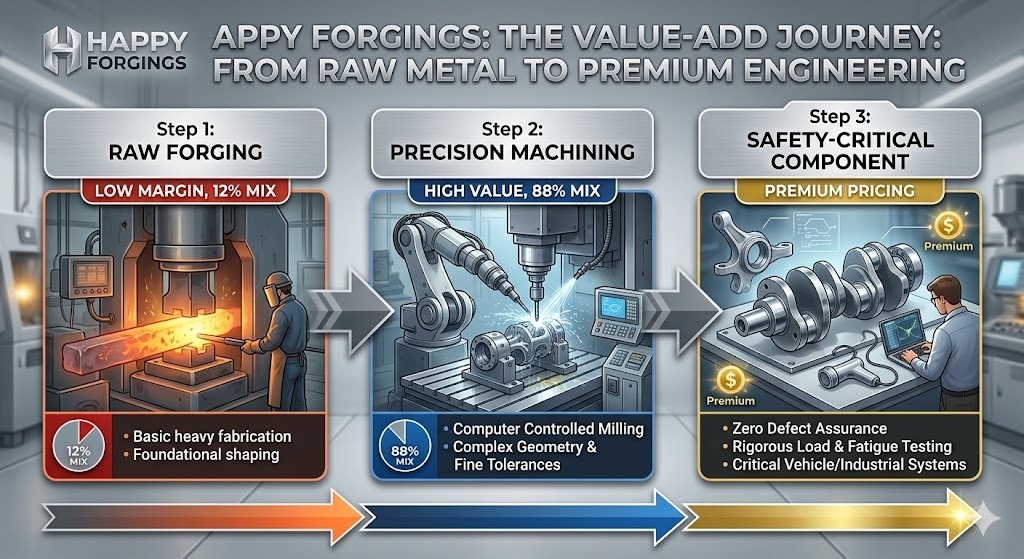

Today, the organization stands as India’s fourth-largest heavy forging entity by installed capacity, operating three integrated manufacturing facilities across Punjab. The narrative surrounding the business has shifted from structural cyclicality to high-value component machining. Instead of selling raw iron shapes by the metric ton, management has repositioned the product mix toward complex, safety-critical engine and drivetrain components where dimensional tolerances are measured in fractions of a millimeter.

Section 3 — Business Model: WTF Do They Even Do?

At its core, Happy Forgings acts as the heavy-metal spine for industrial machines and heavy trucks. They take massive blocks of alloy steel, subject them to intense thermal stress, and strike them with multi-thousand-ton automated presses until they form things like crankshafts, steering knuckles, and differential housings.

If a commercial vehicle OEM needs a front axle carrier that can survive a decade of overloading on poorly maintained highways, they outsource the head injury to Happy Forgings. The corporate strategy hinges entirely on a single metric: value-add. Raw forgings are a low-margin race to the bottom; high-precision machined components are where you get to dictate pricing terms to global industrial clients.

Currently, an overwhelming 89% of their revenue mix comes from fully forged and machined products, leaving only 11% exposed to the commodity-grade raw forging market. Their client list reads like an assembly line of heavy machinery, including Ashok Leyland, Mahindra & Mahindra, JCB, and International Tractors. If it has giant wheels, a diesel engine, or moves earth, Happy Forgings likely machined the components that keep it from snapping in half.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Headline Performance Metrics

Metric

Latest Quarter (Q4FY26)

YoY (%)

QoQ (%)

Revenue

₹424.00

20.4%

8.3%

EBITDA

₹133.00

30.4%

10.7%

PAT

₹84.00

23.6%

5.9%

EPS

₹8.85

23.6%

5.7%

The final three months of fiscal year 2026 registered a sharp volume expansion of 20.6% year-on-year, driving a corresponding revenue jump to ₹424 crore. Operating leverage did most of the heavy lifting this quarter, pulling the trailing three-month EBITDA up by 30.4% to ₹133 crore. High operating margins reflect structural resilience against volatile raw materials, primarily because steel remains an absolute pass-through across 85% of their total sales volumes.

Did Management Walk the Talk?

During the February 2026 conference call, management was explicitly confident about sequential volume recoveries and the realization stability of their high-value automotive mix. They noted that “new product introduction is at better realization rate,” which effectively defended gross margins even as underlying scrap iron pricing mechanics created short-term drag.

Delivery matched the rhetoric; operating margins expanded to 31.5% in Q4FY26, sitting comfortably at the upper boundary of their long-term targeted operating guardrails of 28% to 32%.