Life Insurance Corporation of India FY26: The Elephant Learns to Cha-Cha with a 1:1 Bonus

At a Glance

A structural transformation is quietly unfolding inside India’s state-backed insurance monolith. For decades, this massive entity operated under a simple, heavy-set mandate: gather premium capital through traditional participating products and maintain an army of individual agents. While its absolute footprint remains unparalleled, its vast size historically constrained rapid product innovation and left it exposed to shifting regulatory regimes.

The financial landscape of FY26 indicates a sharp operational transition. Total premium income crossed the threshold of ₹5,35,984 crore, representing a 9.8% year-on-year expansion. More significantly, the institutional shift toward non-participating structural contracts accelerated, with the non-par share of individual Annualized Premium Equivalent (APE) moving from 27.69% in FY25 up to 35.11% in FY26. This structural optimization drove the Value of New Business (VNB) margin up by 360 basis points to a peak of 21.2%.

However, structural complexities remain embedded within this scale. Balance sheet current liabilities sit against a massive asset allocation mix that remains deeply exposed to equity market volatility. At the same time, individual policy persistency at the critical 61st-month mark soft-landed down to 59.31%, highlighting long-term customer retention hurdles. Operational delivery metrics further show an impending maturity payout wave from older, high-sum-assured legacy policy cohorts that will continue to drain short-term liquidity through early 2027.

Introduction

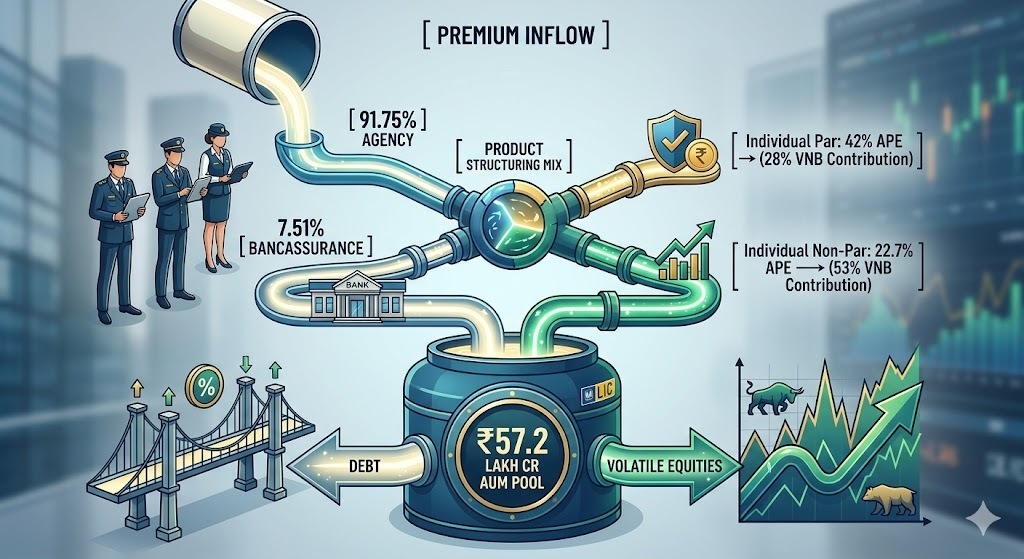

Life Insurance Corporation of India (LIC) occupies an anomalous position in the global financial architecture. It functions simultaneously as a commercial life insurer, a macro-stabilizing capital pool, and a sovereign wealth vehicle holding assets under management (AUM) worth a staggering ₹57,29,396 crore. Founded as a consolidated public entity, it has spent generations defending a dominant domestic market position.

The modern corporate era for LIC has introduced a demanding multi-variable optimization problem: how to satisfy the return metrics required by public equity markets while fulfilling its legacy role as the nation’s foundational insurer. The company’s recent strategic maneuvers—ranging from the aggressive rollout of its digital “DIVE” platform to the institutional scaling of its “Bima Sakhi” rural framework—indicate that the organization is actively trying to restructure its distribution dynamics.

Business Model: WTF Do They Even Do?

At its core, LIC is a massive capital-gathering machine that converts Indian household risk aversion into long-duration investment capital. It operates via an unparalleled distribution network containing over 14.57 lakh active agents, effectively placing its brand footprint across 92% of all domestic districts.

The corporate structure relies on two distinct product engines:

Participating (Par) Products: The legacy base where policyholders share in the underwriting and investment profits of the corporation via annual bonuses.

Non-Participating (Non-Par) Products: The high-margin frontier where return guarantees are locked in, allowing the corporation to retain the residual underwriting profitability.

While individual agents still bring in 91.75% of individual new business premiums, corporate bancassurance and alternate sales channels expanded by 45.19% in FY26. The objective is simple: pivot from low-margin par products toward guaranteed high-margin non-par structures, utilizing bank branches to lower traditional distribution friction.

Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Mar 2025

Jun 2025

Sep 2025

Dec 2025

Mar 2026

Revenue (Sales)

2,43,134.49

224,671.49

241,524.29

235,954.23

276,743.77

Operating Profit

21,513.90

10,473.63

9,492.25

12,365.98

11,222.38

PAT

19,038.67

10,957.05

10,098.48

12,930.44

23,467.18

Reported EPS (₹)

30.10

17.32

15.97

20.44

37.10

The final quarter of FY26 delivered a sharp surge in headline volume, with sales hitting ₹276,743.77 crore—a clear 13.8% step up over the prior year’s corresponding quarter. This year-end volume acceleration pushed quarterly profit after tax to ₹23,467.18 crore.

Financial volatility in insurance operations often stems from the timing of investment realizations rather than core premium changes. Real earnings quality reveals itself in the underlying stability of net asset backing over time.

What is Management Promising in the Coming Quarters?

During the May 2026 earnings interaction, management adopted a conservative posture regarding forward margin targets. Refusing to issue explicit quantitative guidance