Whirlpool of India Ltd FY26: The Cold Truth About Heat, Royalty, and Regulatory Friction

Section 1 — At a Glance

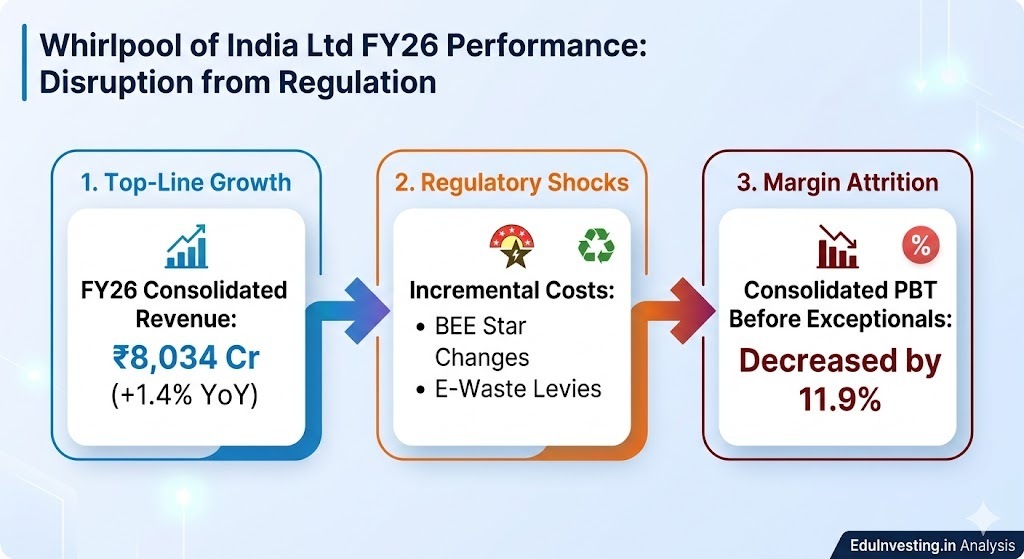

The financial performance of premium appliance giants frequently functions as an early warning indicator for broader consumer discretionary health. Whirlpool of India’s FY26 financial results provide a stark lesson in how regulatory transitions and shifting product mixes can disrupt profit margins even when top-line performance remains intact.

For the full year ended March 31, 2026, the company posted consolidated revenue of ₹8,034 cr, representing a modest increase of 1.4% compared to the previous fiscal year. However, this surface stability conceals significant operational pressure. Consolidated profit before tax (PBT) before exceptional items fell by 11.9% YoY to ₹426 cr, while reported annual net profit dropped to ₹293.75 cr from ₹359 cr in FY25.

This divergence highlights a critical market reality: when inflation or regulatory adjustments alter the underlying cost structure, maintaining top-line revenue is insufficient if the business cannot pass those costs along to consumers.

Investor attention is currently divided between two competing dynamics. On one hand, the company achieved volume growth in its washing machine and air conditioning segments during the fourth quarter. On the other hand, core refrigeration margins faced severe pressure due to competitive industry pricing and Bureau of Energy Efficiency (BEE) star-rating changeovers.

With the parent company’s equity stake reduced and structural agreements locked in through FY29, Whirlpool of India faces an extended operational transition amidst a highly competitive consumer durables landscape.

Section 2 — Introduction

Whirlpool of India Ltd stands as one of the oldest and most recognized brands within the domestic Indian home appliance landscape. For decades, the company built its reputation on consumer utility across core white-goods categories like refrigerators and washing machines.

The operating landscape has fundamentally changed over the past year. Strategically, the corporate umbilical cord connecting the Indian entity to its American parent, Whirlpool Corporation, has been substantially altered. A structural reset executed via a series of long-term transactional packages has redefined the brand’s operational autonomy.

While a 30-year brand license agreement preserves identity continuity in the Indian market, the promoter’s economic stake has been diluted down to 39.76%. Whirlpool of India is navigating this corporate transition while simultaneously defending its market share against aggressive domestic and multi-national competitors who are deploying capacity-led pricing strategies.

Section 3 — Business Model: WTF Do They Even Do?

At its core, Whirlpool of India manufactures machines that either freeze things, wash things, or cool down rooms. Yet, a look at the historical product mix reveals a company experiencing an ongoing identity migration:

The Refrigerator Anchor: Historically the crown jewel, refrigerators accounted for a massive 62% of revenue in FY20. By FY24, that reliance dropped to 33%. The direct-cool segment remains a high-volume category, but it is increasingly vulnerable to commoditization.

The Washer Engine: Washing machines accounted for 25% of the portfolio in FY24. The company has found success premiumizing this segment, achieving high growth in front-load formats.

The Air Conditioner Surge: Air conditioning expanded from a tiny 6% of revenue in FY20 to 26% by FY24. In March 2026, the company cleared an environmental milestone by shipping over 100,000 AC units in a single month.

The Elica Kitchen Subsidiary: By purchasing successive equity tranches, Whirlpool completed its 100% acquisition of Elica India in early 2026. This structural move embeds a premium kitchen hood and hob business directly into the consolidated P&L.

Product Category

FY20 Revenue Mix(Total Base: ₹5,993 Cr)

FY24 Revenue Mix(Total Base: ₹6,830 Cr)

Refrigerators

62%

33%

Washing Machines

22%

25%

Air Conditioners

6%

26%

Others

10%

16%

The underlying economic challenge is that while air conditioners drive top-line volume, they carry structurally lower margins and higher working capital demands than refrigerators. The product mix is expanding into lower-margin segments just as core high-margin categories face increased regulatory compliance costs.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

The fourth quarter provided an operational lift to the top line, but raw material realities and compliance costs impacted profitability.