01 — At a Glance

The Merger Honeymoon Is Getting Weird

- 52-Week High / Low₹260 / ₹111

- Q3 FY26 Revenue₹858 Cr

- Q3 FY26 PAT₹47.9 Cr

- Q3 FY26 EPS₹0.88

- Annualised EPS (Q3×4)₹3.52

- Book Value₹18.6

- Price to Book10.6x

- Debt / Equity0.61x

- 9M FY26 Revenue₹2,500 Cr

- 9M FY26 EBITDA Margin20.1%

The Merge-and-Pump Auditor’s Note: Viyash Scientific reported Q3 FY26 with a ₹858 crore revenue and ₹47.9 crore PAT. Sounds impressive until you realise this is the first combined quarter of a December 2025 merger between Sequent and Viyash. The 134% profit growth and 34.7% sales growth are real—but comparing apples to fractured oranges from last year. ROE of 3.21%? That’s what happens when you merge two struggling entities and call it synergy. P/E 67.6x means the market is betting on management’s promises to deliver 20%+ margins sustainably. Management is betting on INR 50–60 crore synergies kicking in by December 2026. Both sides are gambling. The real question: who’ll blink first?

02 — Introduction

When Two Loss-Makers Become One Profit-Teller (Allegedly)

Sequent Scientific Limited was a middle-child animal health company quietly assembling APIs and formulations across turkey, Brazil, Europe, and India. Decent product pipeline. Terrible returns on capital. Viyash Life Sciences was a private equity-backed companion animal bet with slightly better margins but smaller scale.

Then, on December 16, 2025, they merged. Not joined. Not consolidated. Merged. One entity. One platform. One team. One massive integration headache wearing a 67.6x P/E multiple as a crown.

The February 2026 concall was basically management saying: “We’re combining two things that were separately underperforming, and now they’ll synergise!” The market responded with enthusiasm. Investors responded with skepticism and open Google sheets. Our job: break it down without the marketing polish.

This is a first-quarter-of-merged-entity story. That means: exceptional items are flying around like confetti (INR 48–49 crore), synergies are “not yet reflected” in margins, working capital is a mess (70 days from 49), and management is on a charm offensive saying 20% EBITDA margins will “sustain 100%.” We’re here to translate that into English.

Concall Highlight (Feb 2026): Management: “Synergies are not factored much at this level.” Translation: Everything you’re seeing is organic growth. Wait until we double-count savings and call them adjusted EBITDA.

03 — Business Model: Two Businesses That Lost Money Separately, Now Lose Money Slower Together

Animal Health APIs and Formulations: The Global Spread, Local Struggle

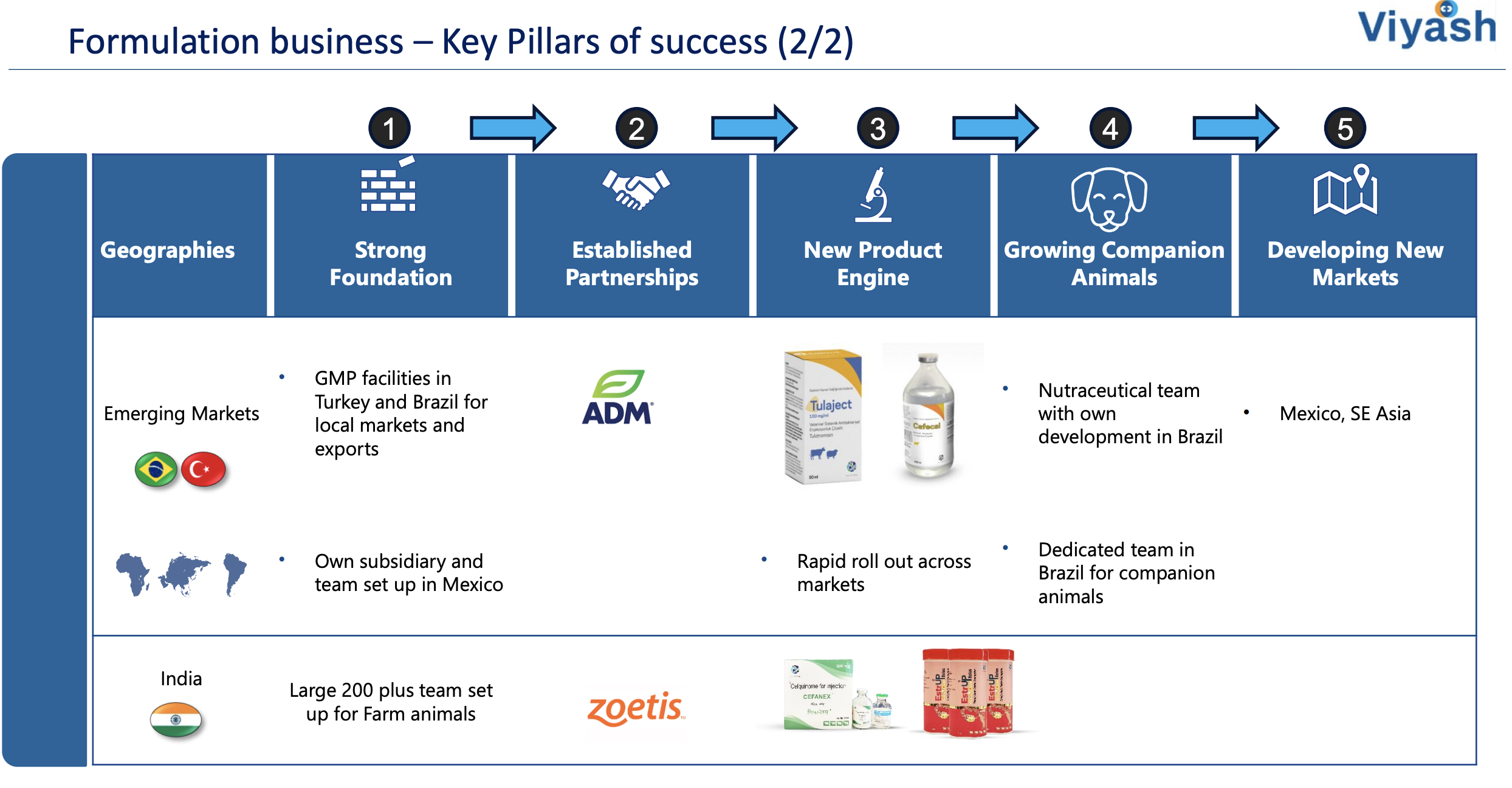

Viyash Scientific operates two segments: (1) Animal Health Formulations — veterinary medicines for cattle, poultry, companion animals across 90+ countries, and (2) Active Pharmaceutical Ingredients (APIs) — raw material powders for other pharma companies, exporting to 50+ countries.

Geographic revenue split (FY24/FY25): Europe ~29% (growing), Latin America ~19%, Turkey ~9% (turnaround story), India ~7%, Emerging Markets ~6%. They’ve got manufacturing in Spain, Turkey, Brazil, and India. 7 facilities. 35 commercial APIs. 1,000+ finished dosage formulations. 100+ countries reached.

Sounds like a global animal health powerhouse, right? Here’s the thing: they’re consistently underlevering capital. ROE of 3.21%. ROCE of 8.47%. These aren’t ratios; they’re indictments. You could put cash in an FD and do better. But management says new products, companion animal expansion, and CDMO (contract development and manufacturing) will fix it. Sure. We’ll monitor.

The 9M FY26 picture (merged entity): Revenue ₹2,500 crore (+12% YoY). EBITDA ₹500+ crore with 20.1% margin. Looks pristine. But this is after INR 48–49 crore in merger-related one-time costs already taken. Without the merger, both entities separately were running at 5–7% EBITDA margins. So yes, 20% is impressive. Also yes, it’s a combination story, not an operational miracle.

💬 Here’s the key question: Is the 20% EBITDA margin real operational improvement, or is it just the new entity dropping legacy loss-making operations (like the Germany facility closure)? You tell us in the comments!

04 — Financials Overview

Q3 FY26: The Numbers (And Why They’re Wearing An Asterisk)

Continue reading with a premium membership.