Vadivarhe Speciality Chemicals Ltd H1 FY26 – ₹17 Cr Half-Year Sales, ₹-3.85 Cr Loss, ROE at a Casual -495%: When Chemistry Meets Accounting Horror

1. At a Glance – The Stock That Refuses To Behave

If stock markets had a “most stubborn underperformer” award, Vadivarhe Speciality Chemicals Ltd would at least make the longlist. Here’s a company with WHO-GMP certification, exports to the US and Europe, marquee pharma clients, and yet… numbers that look like they were audited during a power cut. The market cap sits at roughly ₹22.6 crore, the stock price hovers around ₹17.6, and the return over the last year reads a painful -60%. Book value is negative, ROCE is -22.7%, and ROE is a headline-grabbing -495%, which frankly deserves its own documentary series.

The latest half-year (H1 FY26) numbers show sales of ₹17.04 crore with a net loss of ₹3.85 crore. Sales are growing quarter-on-quarter, but profits remain allergic to positivity. Debt stands tall at ₹31.37 crore against eroded net worth, making lenders far more confident than equity investors. Promoters still hold ~66.8%, which suggests belief, patience, or sheer emotional attachment.

This is not a sleepy microcap. This is a hyperactive balance sheet thriller where every quarter asks the same question: will chemistry finally beat arithmetic? Curious already? Good. Because the story only gets messier from here.

2. Introduction – Welcome to Nashik’s Most Confused Chemistry Lab

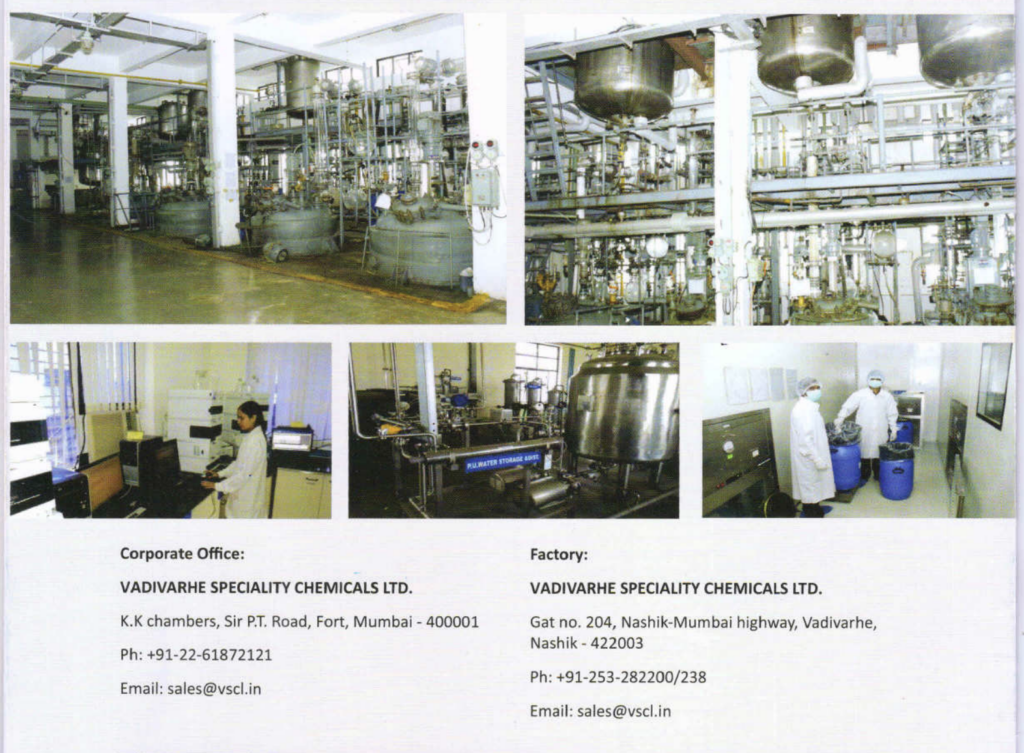

Vadivarhe Speciality Chemicals Ltd (VSCL) was incorporated in 2009 with a simple dream: make speciality chemicals, APIs, and intermediates for global pharma companies, earn respectable margins, and live happily ever after. Fast forward more than a decade, and the company is still manufacturing… but the “happily ever after” part seems stuck in regulatory approval.

On paper, VSCL looks like a serious chemical manufacturer. WHO-GMP certified plant in Nashik. Clients like GlaxoSmithKline, USV, Mankind Pharma, and Hetero Labs. Exports to the US, UK, Switzerland, and Malaysia. If resumes were stocks, this one would at least get shortlisted for an interview.

But then you open the financials. And suddenly, the vibe changes from Breaking Bad to CID. Losses appear year after year. Cash flows oscillate like a chemistry student before exams. Net worth has gone from positive to deeply negative. Auditors have politely cleared their throats and used the phrase “going concern emphasis,” which is audit-speak for “boss, please survive.”

So what exactly is going on here? Is this a temporary rough patch for a speciality chemicals player, or a structural profitability problem dressed up in GMP certificates? Let’s put on our lab coats and investigate.

3. Business Model – WTF Do They Even Do?

Vadivarhe Speciality Chemicals is not your neighbourhood bulk chemical vendor. The company operates in multiple chemical verticals:

Speciality chemicals, APIs, bio-chemicals, drug intermediates, organic and inorganic chemicals, personal care ingredients, and bulk drugs. Yes, that list is long. And yes, that’s usually a red flag for “we do many things, master of none.”

The core business revolves around custom synthesis and manufacturing for pharma and chemical clients. Orders are typically B2B, formulation-driven, and compliance-heavy. The WHO-GMP certification allows them to supply regulated markets, which theoretically should mean better pricing and stickier customers.

The plant at Vadivarhe, Nashik, has an installed capacity of about 150 MTPA. That’s not massive, but it’s respectable for a SME chemical player. Recently, management announced the commencement of commercial production of over 10 APIs, targeting global formulation manufacturers. Sounds exciting, right?

But here’s the catch. Capacity doesn’t pay EMIs. Utilisation does. And margins do. VSCL’s problem is not lack