Va Tech Wabag Ltd FY26: The ₹1,080 Crore Cash Flush—How an Asset-Light Pure-Play Solved the EPC Working Capital Curse

Section 1 — At a Glance

Va Tech Wabag Ltd closed FY26 with a robust performance, demonstrating the execution capabilities of a pure-play water technology leader operating an asset-light model. Total consolidated revenue for the financial year reached ₹3,944.2 crore, marking a 19.7% year-on-year expansion that fits within management’s structural medium-term guidance of 15–20% compounded annual growth. This top-line expansion was matched by a 21.8% year-on-year increase in consolidated EBITDA, which reached ₹524.1 crore, while Profit After Tax (PAT) climbed 25.5% year-on-year to ₹370.5 crore.

Financially, the company achieved an unencumbered gross cash milestone of ₹1,080 crore, leading to a net cash position of ₹950 crore (excluding transient engineering development SPV debt). This marks the sixth consecutive year of positive net cash accumulation, structurally shifting the net finance cost line into net positive treasury income. Backlog velocity remained high, with the closing consolidated order book expanding 26% year-on-year to a record ₹17,235 crore. This provides a clear visibility runway of over 4.3 times historical revenue.

Investor attention is drawn to the expanding share of long-term Operations & Maintenance (O&M) and framework contracts, which now constitute 38% of the closing backlog at ₹63,462 million. This shift provides predictable annuity income streams that buffer the lumpier Engineering, Procurement, and Construction (EPC) execution cycles. However, worry signals persist within the balance sheet architecture. The company operates with an inherently elongated working capital cycle, driven by municipal billing milestones and unbilled revenue mechanics, leaving debtor days extended at 234 days.

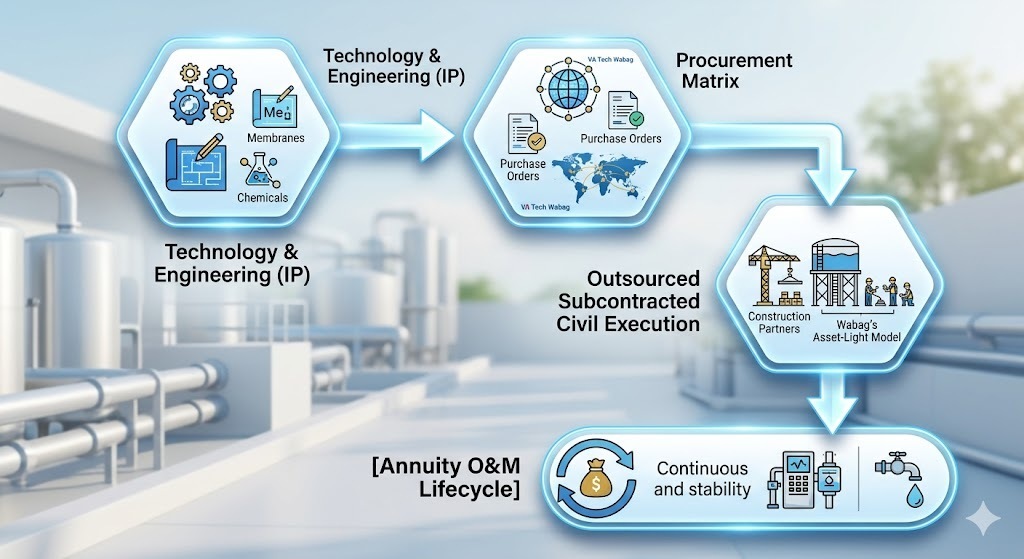

Real structural asset-efficiency is not achieved by scaling heavy industrial hardware, but by leveraging intellectual property to control the monetization cycle while outsourcing capital-intensive execution.

The forward-looking operational framework remains contingent on the administrative completion of the municipal public-private partnership platform with Norfund to formally deconsolidate legacy capital commitments.

Section 2 — Introduction

Va Tech Wabag Ltd has evolved from a traditional municipal engineering contractor into a global, technology-led pure-play water solutions multinational. Headquartered in Chennai, India, with localized operational hubs stretching from Bucharest to Riyadh, the corporate entity controls a century of specialized processing lineage. The company’s capabilities cover the entire lifecycle of industrial and civil water processing, specializing in advanced sewage treatment, high-purity industrial process recycling, zero-liquid-discharge systems, and mega-scale reverse osmosis sea desalination.

Strategically, management has implemented an explicit operational pivot designed to insulate the corporate balance sheet from the traditional vulnerabilities of the civil infrastructure sector. By divesting legacy international assets—including the step-down European operations of Wabag Water Services S.R.L. Romania in August 2024 for EUR 1.20 million—the organization has concentrated its business capital on high-margin, payment-secured contracts in India and the Middle East and Africa (MEA) clusters. This restructuring aligns with a corporate design focused on technology delivery and operational management, while shifting capital-heavy asset ownership to institutional infrastructure financiers and private development funds.

Section 3 — Business Model: WTF Do They Even Do?

To the casual observer, Va Tech Wabag builds very large, deeply unglamorous concrete tanks that prevent municipal wastewater from turned adjacent ecosystems into a crisis zone. To the institutional market, it operates as a specialized intellectual property wrapper that brokers engineering solutions across a global multi-billion-dollar addressable market. The company does not operate heavy machinery, pour commodity concrete, or maintain an expensive fleet of earthmovers. Its gross carrying value of physical property, plant, and equipment is a minimal ₹66 crore, allowing it to generate nearly ₹4,000 crore in revenue on a virtual balance sheet footprint.

The enterprise monetizes its business through two operational frameworks:

Engineering Procurement (EP) / EPC (83% of FY26 Revenue): The company engineers the fluid dynamics, specifies the membrane chemistries, designs the automated controls, buys the high-tech pumps, and leaves the low-margin work of laying pipelines to local subcontractors.

Operations & Maintenance (O&M) Annuity (17% of FY26 Revenue): Once built, municipal bodies realize they cannot run advanced automated facilities. Wabag steps back in under 15-to-25-year contracts to operate the assets, capturing predictable, high-margin cash flows that fund corporate distributions.

The structural revenue mix is systematically shifting toward international geographic corridors (52% of revenues) and municipal municipal counterparties (80% of execution). Through its pioneering “One City One Operator” (OCOO) blueprint, the corporate entity now manages entire urban sewage ecosystems, such as Agra (180 MLD) and Ghaziabad (462 MLD), establishing a long-term annuity model that transforms municipal chaos into recurring corporate revenue.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Headline Execution Performance

Metric

Latest Quarter (Q4 FY26)

YoY (%)

QoQ (%)

Revenue

1,414.40

22.33%

47.18%

EBITDA / Operating Profit

156.00

10.79%

-14.29%

PAT

128.00

28.64%

14.29%

Reported EPS (₹)

20.59

28.69%

39.88%

Financial Commentary & Performance Evaluation

The final quarter of the financial year delivered a massive operational acceleration, with revenue for Q4 FY26 expanding 22.33% year-on-year to ₹1,414.40 crore. This outpaced historical sequential trend lines as marquee industrial packages and large-scale domestic engineering works hit peak billing velocity. Operating profit for the quarter came in at ₹156.00 crore. While gross EBITDA absolute numbers advanced, the unadjusted OPM compressed slightly to 11.0% due to transient project mix shifts and late-stage cost recognition adjustments across international jobs.

Net Profit for the single quarter surged 28.64% year-on-year to ₹128.00 crore, supported by a significant reversal in the finance cost architecture.