ICRA Ltd FY26: A 20% Topline Flex Encounters the Amortisation Reality Show

Section 1 — At a Glance

A business that explicitly prices the risk of others should theoretically have its own house in absolute, predictable order. In FY26, credit rating major ICRA Ltd delivered a heavy operational headline: revenue from operations surged by 20.43% year-on-year to hit ₹599.51 crore, up from ₹498.02 crore in the previous fiscal year. This top-line acceleration outpaced its multi-year compounded growth averages by a wide margin. However, the quality of this expansion tells a more nuanced story. Profit before tax (PBT) grew at a far more modest clip of 7.04%, reaching ₹250.45 crore. This creates a sharp operational divergence where incremental revenue is not translating into proportional bottom-line gains.

The divergence is primarily a symptom of strategic structural realignment. While the core Ratings franchise expanded efficiently on the back of resilient domestic bank credit, the company deployed ₹253.25 crore in cash to acquire RegTech firm Fintellix India. This asset purchase has introduced non-cash multi-year accelerated depreciation and transaction-linked amortisation cycles that will structurally suppress reported earnings per share (EPS) over the near term, even as cash operating metrics remain robust. Furthermore, a significant spike in “Other Expenses” to ₹74.35 crore during the year indicates that administrative adjustments and legacy liabilities are actively competing for operating cash.

Earnings quality is never defined by a single top-line burst; it is defined by the structural friction required to defend it. For a premium service business trading at a substantial valuation multiple, investors are currently forced to balance structural rating dominance against near-term non-cash margin dilution.

Section 2 — Introduction

ICRA Ltd occupies an enviable corporate position in the Indian financial architecture. Established in 1991 and backed indirectly by global rating titan Moody’s Corporation—which holds a controlling 51.86% stake—ICRA is one of the gatekeepers of the domestic debt market. It spends its days evaluating the structural strength of manufacturing entities, banks, non-banking finance companies (NBFCs), and massive infrastructure projects.

However, over-reliance on a single macro-driven cyclical pipeline is a precarious long-term strategy. To insulate itself from volatile domestic bond issuance cycles, management has spent the last few years aggressively engineering a corporate pivot toward non-ratings businesses. This manifests via two core operating divisions: Ratings and Research & Analytics (R&A). The latest chapter of this diversification strategy involves significant capital deployment into regulatory technology, moving the company squarely into the high-stakes, multi-geography compliance software arena.

Section 3 — Business Model: WTF Do They Even Do?

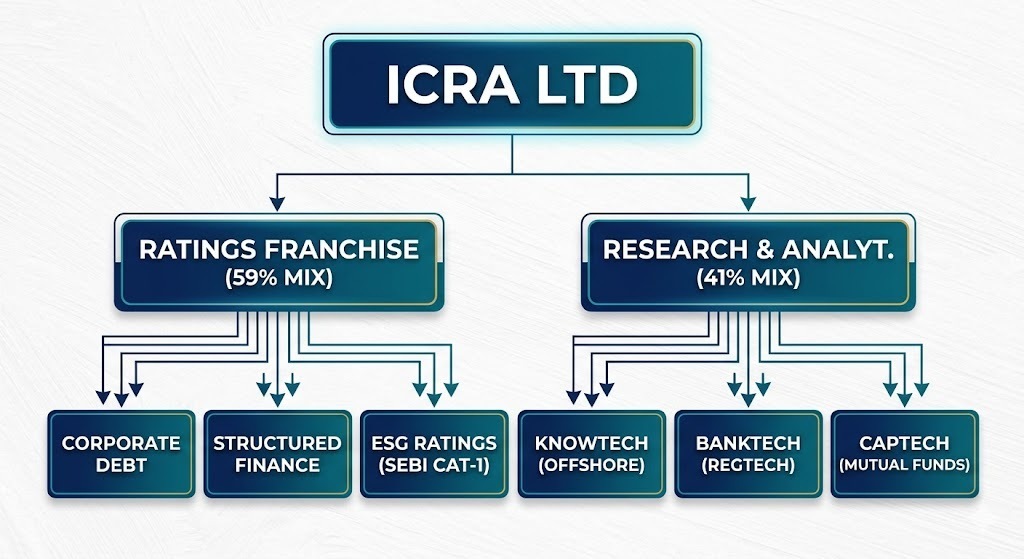

At its core, ICRA is a tollbooth on the highway of capital allocation. If a corporate entity wants to raise money via commercial paper, non-convertible debentures, or bank loans, they must pay ICRA to assess how likely they are to default. This Ratings division commands 59% of the corporate revenue mix. It is a beautiful, highly sticky model: you perform analytical work once, and then you collect recurring monitoring fees annually for as long as that debt is live in the system.

The other 41% of the house belongs to Research & Analytics (R&A). This segment is further split into KnowTech (offshore tech-enabled data management primarily serving Moody’s ecosystem), BankTech (risk management products for financial institutions), and CapTech (market data and valuation tools for mutual funds).

Through the Fintellix acquisition, ICRA is attempting to combine its credit risk domain expertise with automated compliance software, expanding its addressable wallet across Middle Eastern and US banking networks. It is an ambitious attempt to transform from an Indian analytical service house into a global subscription product provider.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Performance Trend

Metric

Latest Quarter (Mar 2026)

YoY

QoQ

Revenue

₹174.85

41.05%

6.88%

Operating Profit

₹69.56

39.56%

21.61%

PAT

₹52.45

11.91%

35.11%

EPS (Reported)

₹54.35

11.92%

35.13%

Note: Growth calculations are derived directly from the consolidated quarterly data sheet.

Did Management Walk the Talk?

During previous interactions, management committed to two major operational themes: structurally expanding the non-ratings revenue mix to diversify away from Moody’s-linked Knowledge Services and utilizing process reengineering to defend margins.

The numbers show that execution is a game of two halves. The Ratings business successfully extracted internal efficiencies, with margins expanding over the last eight quarters due to analytical automation. However, the R&A business grew at a modest 1.8% in H1FY26, severely weighed down by the complete runoff of its legacy ESG project pipeline and internal automation inside the Moody’s ecosystem.