United Polyfab Gujarat Ltd Mar 2026: Fire, Tax Raids, and a 37% Profit Surge

Section 1 — At a Glance

United Polyfab Gujarat Ltd posted an annual revenue from operations of ₹682.03 crore for the fiscal year ended March 31, 2026, marking a 13.23% growth compared to ₹602.22 crore in the previous fiscal year. Net profit for the full year surged 37.25% to ₹24.29 crore, up from ₹17.69 crore in FY25, driven by structural shifts in product mix and a notable reduction in manufacturing power costs. Annualized Earnings Per Share (EPS) for the fiscal year reached ₹1.06 based on the 22.95 crore adjusted equity shares outstanding.

The primary catalysts drawing investor interest are the expanding operating margins and the commissioning of captive renewable energy plants. The company operationalized 1 MW of solar power and 2.7 MW of wind power during FY25, yielding a direct power cost savings of ₹2.90 crore. An additional 5.384 MW solar capacity was slated for commissioning in early 2026, positioned to fulfill nearly 70% of total manufacturing power requirements by FY27.

However, severe concerns balance this optimism. A major fire broke out at the company’s factory premises on February 19, 2026, prompting Infomerics Valuation and Rating to place its bank facilities on ‘Rating Watch with Developing Implications’ due to potential near-term operational disruptions. Furthermore, corporate governance scrutiny intensified after an Income Tax Department search conducted under Section 132 on December 9, 2025, resulted in the seizure of unexplained cash. Margins are structurally exposed to highly volatile raw cotton prices, and a massive capital allocation block remains tied up in non-moving inventories, which expanded significantly over the year. Capital efficiency gains can easily be wiped out when external operational and regulatory friction begins to outpace core production advantages. The contrast between stellar reported profitability and deteriorating operational risk forms the core analytical tension for the company heading into the new fiscal year.

Section 2 — Introduction

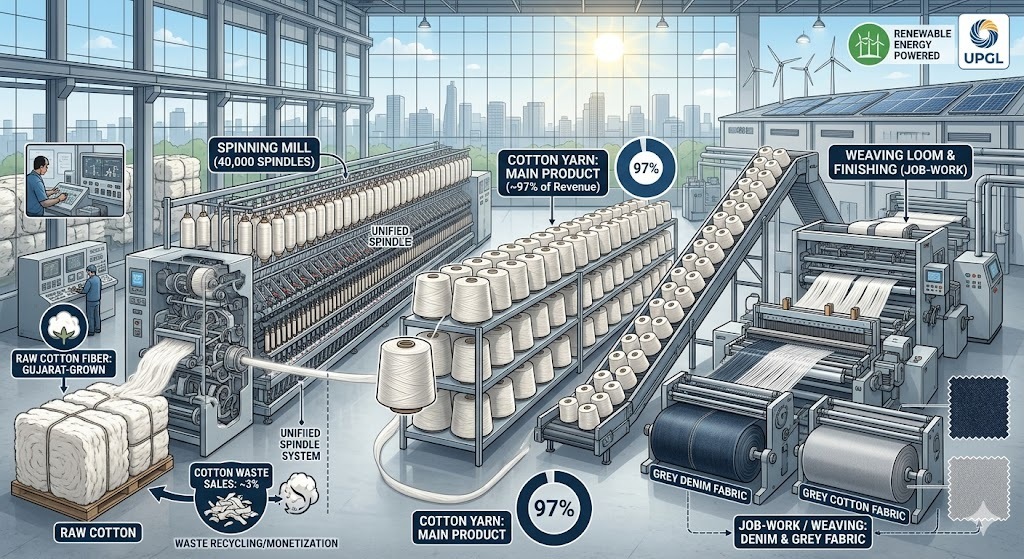

United Polyfab Gujarat Ltd (UPGL), incorporated in 2010 and headquartered in Ahmedabad, operates at the foundational end of the textile value chain. The company has transitioned from a small-scale textile player into an integrated spinning and weaving unit utilizing an installed base of 40,000 spindles.

This analysis is prompted by the release of the audited financial results for the quarter and full year ended March 31, 2026. The recent corporate timeline has been extraordinarily volatile, featuring a promoter-backed financial restructuring plan via equity warrants alongside unpredictable real-world setbacks like plant fires and tax raids. We explore the company’s structural unit economics, verify whether its balance sheet can withstand external disruptions, and assess if the current market valuation aligns with its underlying operational cash flows.

Section 3 — Business Model: WTF Do They Even Do?

At its core, United Polyfab converts raw cotton into yarn and woven fabrics. The business model is segmented into four primary product streams: cotton yarn (predominantly fine counts), dyed fabrics, grey fabrics, and denim fabrics. Operationally, the company functions both as a direct product manufacturer and as a job-work service provider for regional denim and cotton fabric brands, serving large industry clients such as Jindal, Welspun, and Aarvee Denims.

Financially, yarn is the absolute anchor of the top-line, accounting for approximately 97% of total sales, with the remaining 3% derived from cotton waste monetization. Geographically, the business model exhibits extreme concentration, as the company derives 100% of its operational sales from the state of Gujarat. While this localization saves significantly on logistics costs and places production directly inside India’s cotton-growing belt, it leaves the company entirely exposed to regional power tariffs, local labor shocks, and state-level policy shifts.