SMS Pharmaceuticals FY26: A ₹102 Crore Mirage or a Genuine Structural Metamorphosis?

Date of Publishing -

Spotted a factual error — a wrong number, date, or fact? Tell us and we will check the source.

1. At a Glance

A headline net profit of ₹102 crore for FY26 represents a 47% year-on-year surge that initially commands investor attention. This milestone crowns a multi-year recovery from a net loss in FY23, driven primarily by a 13% expansion in top-line revenue to ₹887 crore and a 155-basis-point expansion in EBITDA margins to 19%. However, beneath this polished exterior lies a far more intricate and delicate earnings structure.

A substantial portion of this bottom-line growth is driven by the sudden, dramatic financial turnaround of an associate entity, VKT Pharma. VKT contributed ₹13.99 crore to the consolidated net profit in FY26, up from just ₹1.74 crore in FY25. Excluding this associate boost, SMS Pharmaceuticals’ core business grew at a more modest 31% to ₹88 crore.

At the same time, operating cash flow conversion fell sharply from 73% in FY25 to 49% in FY26. This decline stems from an asset-heavy business model that locked up ₹351 crore in inventory and pushed the total operating cycle to an elongated 160 days.

With total debt climbing to ₹365 crore to fund an aggressive ₹280 crore capital expenditure program, the market finds itself weighing the near-term benefits of backward integration against structural cash conversion bottlenecks.

2. Introduction

SMS Pharmaceuticals Limited stands as an established name in the highly volatile Indian merchant Active Pharmaceutical Ingredient (API) sector. Having spent over three decades navigating price erosion and supply-chain whiplash, the company operates across two commercial manufacturing sites with a total reactor capacity of 3,120 KL.

Historically known as the world’s largest manufacturer of the anti-ulcer drug Ranitidine, management has spent the last five years attempting to de-risk its product portfolio. They have pivoted toward high-volume, vertically integrated generic drug categories while gradually building out secondary platforms in anti-diabetics and anti-retrovirals.

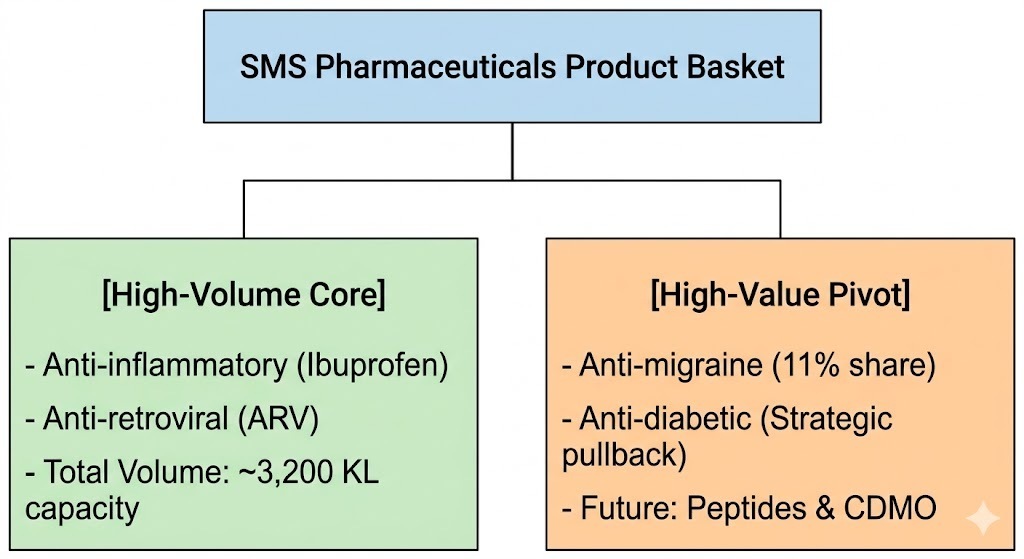

3. Business Model: WTF Do They Even Do?

At its core, SMS Pharmaceuticals is a contract manufacturer and bulk supplier of generic raw materials to global formulations giants like Cipla, Zydus, and Teva. The business model splits its portfolio between high-volume commodities and high-value molecules.

The underlying issue here is a heavy concentration of revenue, with the top 10 customers contributing 76% of sales, and a single, unnamed buyer holding a 28% share. Management insists this single-customer risk is safe because it is spread across multiple products, though investors might view it more like a giant single point of failure distributed across several baskets.

Furthermore, the company’s geographical mix has seen a major shift. Exports fell from 19% in FY22 to 13% in Q3 FY25, forcing SMS to lean heavily on the competitive domestic market for 87% of its sales.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Headline Results

Metric

Latest Quarter (Q4 FY26)

YoY

QoQ

Revenue

238.00

-4.13%

13.09%

EBITDA

40.00

-2.44%

-8.36%

PAT

32.71

60.97%

39.37%

EPS

3.49

52.40%

39.04%

Did Management Walk the Talk?

In May 2025, management laid out an ambitious roadmap for FY26, targeting 20% top-line growth and a 20% EBITDA margin, supported by cost savings from their backward integration projects. Looking at the final FY26 results, revenue fell short at 13% growth, while the full-year EBITDA margin landed just below the target at 19%.

During the May 2026 conference call, management explained that external factors disrupted their goals. Rising geopolitical conflicts in the Middle East created logistics and freight bottlenecks, while a sharp spike in solvent costs during March compressed late-quarter margins.

What is Management Promising in the Coming Quarters?

Looking ahead, management is sticking to a conservative 15% revenue growth guidance for FY27. They have also set an aspiration to push EBITDA margins toward an all-time high of 22%, banking on the full operational rollout of their backward integration infrastructure.

Crucially, the company has updated its product roadmap. Management has requested a two-quarter window before providing final details on its upcoming peptide and CDMO initiatives, with meaningful revenue contributions from these high-margin platforms pushed back to FY29.

Would you back a management team that continually asks the market to wait two more quarters for commercial clarity on its next leg of growth?

5. Valuation Discussion

To assess the valuation structure of SMS Pharmaceuticals, we analyze its trailing financials against historic peer bands. For FY26, the company recorded a reported full-year EPS of