Siyaram Silk Mills Mar 2026: The ₹2,572 Crore Textile Giant Trying On Fast-Fashion Denim

Section 1 — At a Glance

Siyaram Silk Mills Limited delivered a steady financial performance for the fiscal year ended March 31, 2026, with revenue from operations reaching an all-time high of ₹2,572.50 crore, up 15.8% compared to ₹2,221.62 crore in the previous fiscal year. Operating profit (EBITDA) for the full year stood at ₹413.20 crore, registering a growth of 17.2% against ₹352.60 crore in FY25, while maintaining core consolidated operating margins stable at 16.1%. Full-year net profit (PAT) expanded by 17.1% to ₹230.90 crore, translating into a basic EPS of ₹50.89 on its equity capital base.

Investor enthusiasm is primarily anchored around the company’s aggressive retail transition into fast-fashion and ethnic wear via its newborn flagship formats, ZECODE and DEVO, alongside a robust asset-light outsourcing model where approximately 40% of fabric and 80% of garment volumes are outsourced to optimize capital efficiency. However, the structural divergence between rapid top-line growth and compressing cash flows is emerging as a critical point of friction. Operating cash flows dropped sharply from ₹255.02 crore to ₹93.18 crore year-on-year, driven by an extensive working capital build-up and a significant surge in marketing outlays, including the signing of high-profile brand ambassadors. True corporate agility is tested not when demand is booming, but when capital efficiency is maintained through aggressive retail expansions. As Siyaram targets an aggressive store rollout to counter cooling demand in its legacy wholesale segments, near-term profitability faces transitional friction from retail incubation losses.

Section 2 — Introduction

Siyaram Silk Mills Limited has long been a household brand across the semi-urban and rural landscape of multi-brand textile retail in India. Established over four decades ago, the corporate narrative has revolved around positioning high-quality menswear fabrics under legacy umbrellas such as Siyaram’s, J. Hampstead, Mistair, and Cadini Italy.

This comprehensive review explores Siyaram’s strategic crossroad in May 2026 as it formally reports its audited financial outcomes for the full fiscal year. The publication of these results coincides with an ambitious corporate pivot: the structural launch of company-owned, company-operated (COCO) retail engines tailored to capture the structural consumption shift in youth fashion. With a massive domestic distribution ecosystem under pressure from unorganized regional lookalikes and digital marketplace proliferation, this article untangles whether Siyaram’s capital allocation into standalone retail formats represents a genuine value-unlocking modern blueprint or a margin-diluting misadventure.

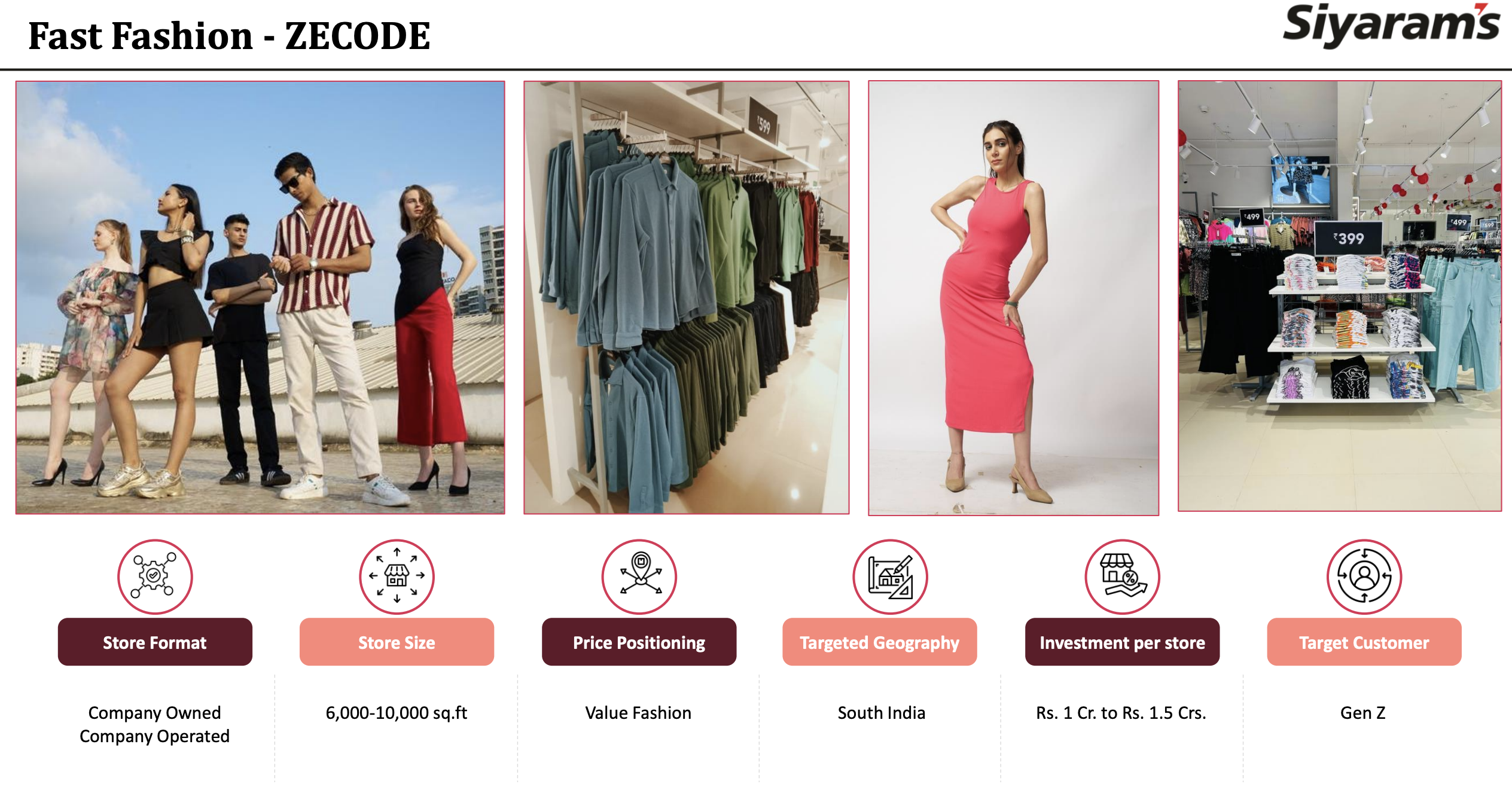

Section 3 — Business Model: WTF Do They Even Do?

At its core, Siyaram is a textile distribution engine masquerading as a manufacturing powerhouse. The revenue blueprint for FY25 shows a structural concentration in traditional textiles: Fabrics dictate a massive 81% of the top-line, followed by Readymade Garments at 13%, and peripheral sub-segments filling the remaining 6%. Geographically, the company is almost entirely insulated within boundaries, extracting 91% of its turnover from domestic markets and routing a modest 9% through international fabric converters.

The underlying mechanical framework utilizes a hybrid asset-light methodology. While Siyaram commands 11 manufacturing units across Tarapur, Daman, Amravati, and Silvassa, it deliberately outsources 50% of its fabric finishing and a staggering 80% of its garment assembly lines. This shields the balance sheet from brutal capacity underutilization penalties during demand downturns. The newer operational models, ZECODE (fast fashion capped at accessible pricing) and DEVO (premium traditional menswear), represent a hard strategic shift into direct retail ownership, aiming to replace wholesale intermediate friction with pure gross margin extraction.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly & Annual Trend Analysis

The financial trajectory highlights a back-ended growth surge in the final three months of the fiscal year, compensating for intermediate patches of soft retail activity.