BLS International Q4 FY26 : Visa Monopolist Crosses ₹2,900 Crore Operating Baseline on 40% Structural Margins

Section 1 — At a Glance

BLS International Services Ltd delivered a record-shattering operational performance for the fiscal year ended March 31, 2026, driven by an aggressive structural migration toward self-managed visa execution centers and high-velocity digital onboarding platforms. Full-year consolidated revenue scaled 36.7% to touch ₹2,998.22 crore, compared to ₹2,193.30 crore in FY25. This geometric top-line growth triggered substantial operating leverage within its core Visa & Consular franchise, propelling consolidated earnings before interest, taxes, depreciation, and amortization (EBITDA) by 30.1% to ₹818.90 crore, achieving an elite structural EBITDA margin of 27.3%. Net Profit After Tax (PAT) expanded 34.1% year-on-year to hit ₹723.80 crore.

The primary catalyst attracting immediate public market focus is the company’s dramatic transition away from localized partner-run processing layouts toward 100% self-managed execution facilities, which pushed segment-level visa margins to a peak of 40.1%. Concurrently, inorganic rollups—specifically the integration of Turkey-based iDATA and Dubai’s Citizenship Invest—have rapidly expanded the group’s cross-border jurisdiction.

However, corporate governance watchdogs and institutional allocators remain hyper-focused on lingering regulatory and balance-sheet friction points. The business correspondent and digital services pipeline experienced significant margin dilution, with divisional metrics sliding to 7.0% due to thin direct-selling-agent pass-through fees stemming from the newly consolidated Aadifidelis loan-distribution vertical. Furthermore, the asset layout now carries an elevated intangible footprint, harboring ₹1,212.80 crore in goodwill alongside a sharp expansion in gross borrowings to ₹430.58 crore.

In asset-light outsourcing monopolies, real financial scale occurs when the incremental cost of processing a transaction drops asymptotically toward zero while upfront processing collections systematically starve the working capital cycle.

The subsequent analytical segments dissect whether these structural tailwinds can successfully outrun intensifying margin degradation inside the domestic digital matrix.

Section 2 — Introduction

BLS International has established a dominant global duopoly alongside competitor VFS Global in the highly sensitive niche of sovereign Government-to-Citizen (G2C) identity and visa processing infrastructure. Operating as an exclusive administrative intermediary for 46 client governments across 80+ sovereign territories, the corporate architecture is meticulously organized to absorb non-discretionary visa workflows, document authentication, biometric capture, and premium value-added ancillary services.

The publication of this comprehensive analysis coincides with an extraordinary structural turning point for the enterprise. In late 2025, the company navigated severe regulatory volatility when a sudden two-year debarment order issued by the Indian Ministry of External Affairs (MEA) was forcefully quashed and set aside by the Hon’ble High Court of Delhi. This full judicial clearance cleared the operational runway for the group to deploy a series of mega-concessions won in early 2026, most notably a landmark domestic UIDAI Aadhaar deployment contract valued up to ₹2,553.35 crore over a six-year horizon.

By analyzing the audited financial reports for the period ending March 31, 2026, this report strips away the promotional presentation layer to evaluate the underlying unit economics of cross-border human mobility.

Section 3 — Business Model: WTF Do They Even Do?

To the uninitiated retail investor, BLS International looks like a glorified travel agency. In reality, it acts as a tollbooth on the borders of sovereign nations. The company’s business model is divided into two distinct, non-overlapping operational engines:

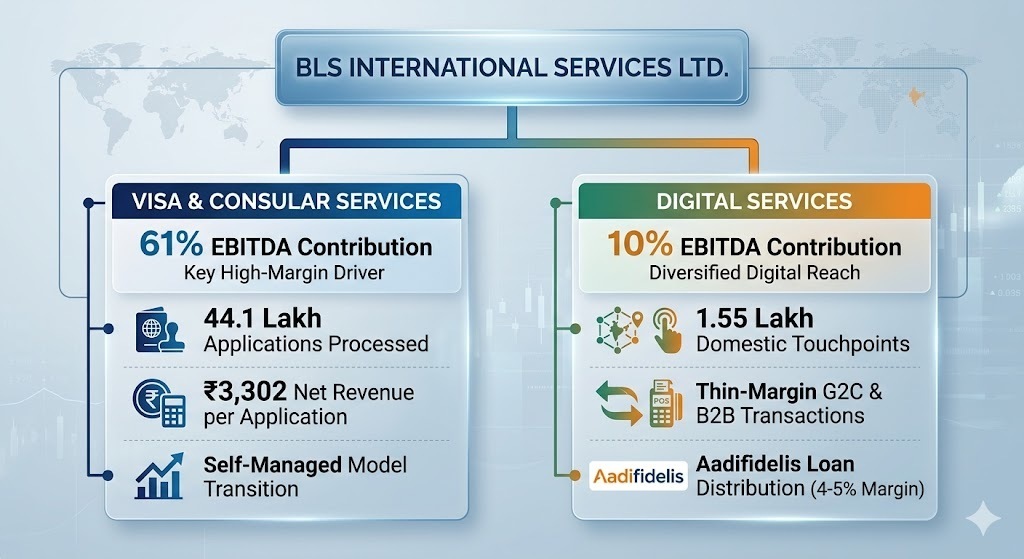

1. Visa and Consular Services (61.3% of Segmental EBITDA Group Mix)

BLS handles everything except the actual “Yes/No” decision on a visa application. They lease real estate, build secure information networks, capture facial recognition and liveness metrics, and upsell premium services (lounge access, SMS tracking, insurance). Economics are entirely transaction-driven. In FY26, the company scaled its annual volumes to 44.1 lakh applications processed, while net revenue per application surged 13.7% to reach ₹3,302, reinforcing their extreme pricing power via value-added upsells.

2. Digital Services (Housed under listed subsidiary BLS E-Services)

This segment is a high-volume, hyper-localized domestic infrastructure play utilizing 155,000+ brick-and-mortar citizen touchpoints across rural and semi-urban India. Acting as principal Business Correspondents for major financial institutions (SBI, PNB, HDFC), they process micro-deposits, distribute basic e-governance paperwork, and manage Aadhaar identity enrollment centers. While gross transaction value (GTV) rocketed past ₹1.1 lakh crore, the business functions on razor-thin fee splits, rendering it a massive cash-throughput engine with minimal structural margin contribution.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Performance Trend Analysis

Metric

Latest Quarter (Q4 FY26)

YoY (%)

QoQ (%)

Full Year FY26

Full Year FY25

YoY Annual (%)

Revenue

814.56

17.58%

10.60%

2,998.22

2,193.30

36.70%

EBITDA

203.91

17.12%

3.00%

818.90

629.30

30.13%

PAT

177.80

120.16%

9.30%

723.80

539.60

34.14%

Reported EPS (₹)

4.32

120.41%

9.37%

16.68

12.34

35.17%

The top-line velocity observed across the historical table signals strong structural health, but the real magic is occurring behind the scenes in the cost accounting layout. In Q4 FY26, total consolidated revenue came in at ₹814.56 crore, supported by an accelerating application count of 10.8 lakh inside the visa division.

Annual reported profit after tax reached ₹723.80 crore. A core operational divergence must be highlighted: raw visa volumes grew by roughly 10% during the quarter, while