Scoda Tubes Mar 2026: A 217-Day Inventory Pile-Up Disguised as a Growth Story

Date of Publishing -

Spotted a factual error — a wrong number, date, or fact? Tell us and we will check the source.

1. At a Glance

Scoda Tubes presents a financial profile characterized by top-line stagnation masking significant underlying balance sheet stress. For the full year FY26, the company posted consolidated revenue of ₹518.65 Cr and a Net Profit of ₹38.84 Cr, translating to an annual EPS of ₹6.48. However, a deeper look into the components driving these figures reveals substantial operational bottlenecks.

The most alarming signal lies in the working capital cycle. Inventory days have ballooned to 217 days, effectively meaning the company is holding over seven months of stock. Consequently, the operating cash flow for FY26 collapsed to a negative ₹13.79 Cr, marking a stark divergence from the reported PAT. Growth on the income statement means nothing until it arrives on the cash flow statement.

On the capital allocation front, the company deployed ₹149.93 Cr in investing activities, funded heavily by ₹152.73 Cr from financing, riding on the back of a recent ₹220 Cr IPO. With a cancelled European acquisition and management citing gas supply disruptions for a weak Q4, the core narrative hinges entirely on their upcoming welded tube capacity expansion. Can a heavy CAPEX cycle bail out a broken cash conversion cycle?

2. Introduction

Established in 2008 and operating out of Mehsana, Gujarat, Scoda Tubes Limited essentially takes stainless steel and turns it into seamless and welded pipes. They recently hit the primary markets in June 2025, raising ₹220 Cr to fund capacity expansions and feed their growing working capital hunger.

The timing of the IPO is fascinating, arriving just before the company posted a quarter characterized by severe supply chain snarls and negative operating cash flows. The Patel family holds a tight 66.43% grip on the equity, steering a ship that exports roughly 30% of its output to places like Italy and Germany while relying heavily on domestic power and infrastructure tenders.

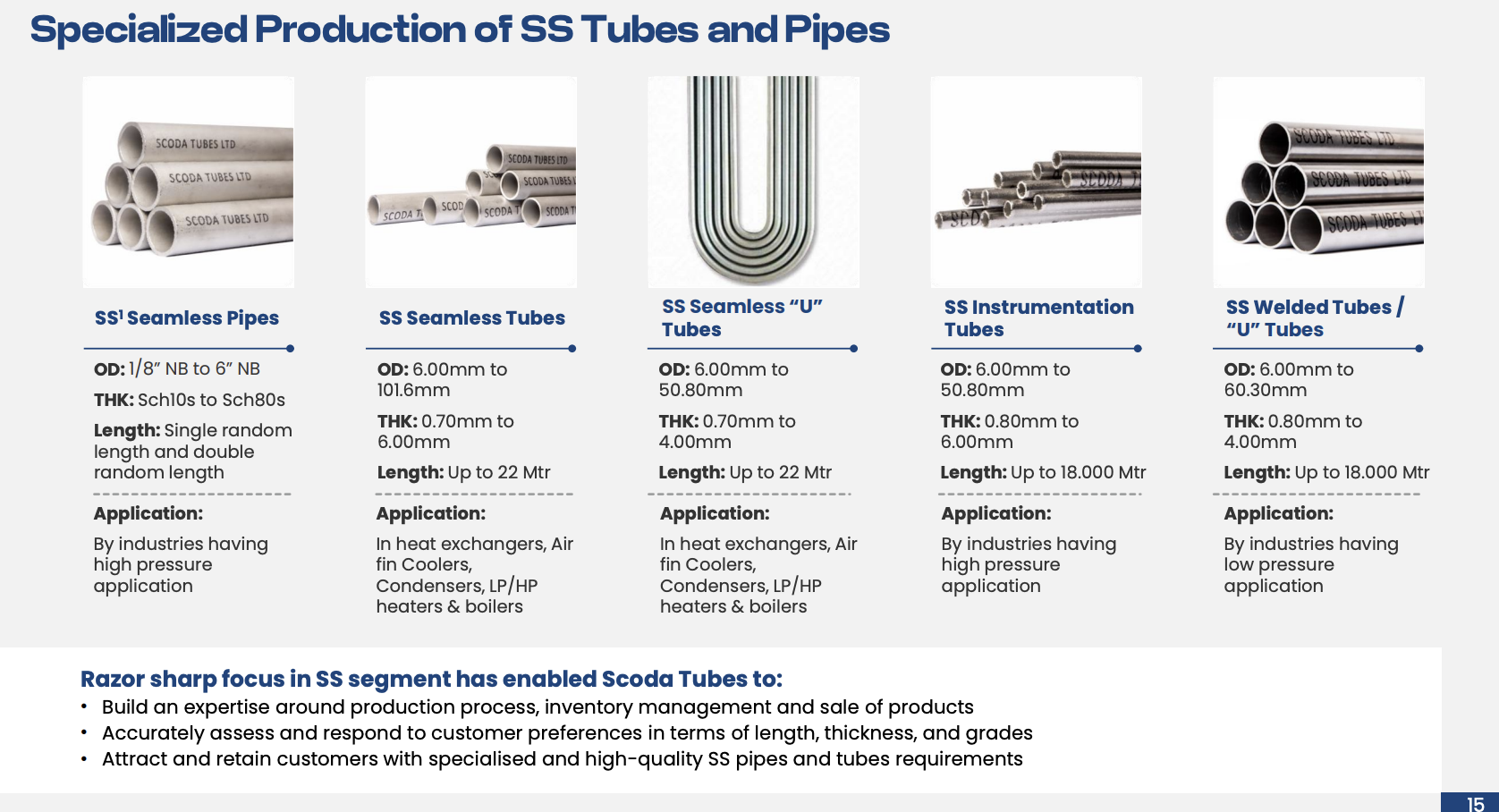

3. Business Model: WTF Do They Even Do?

Scoda Tubes operates in the glamorous world of high-pressure stainless steel tubes. They segment their portfolio broadly into two buckets: seamless tubes (which are exactly what they sound like—extruded metal with no joints, built for high pressure) and welded tubes (the cheaper, lower-pressure cousins).

Currently, their manufacturing facility cranks out 20,068 MTPA of seamless tubes, backed by a 20,000 MTPA “mother hollow” backward integration plant. But the strategic pivot is happening in the welded segment, where they are aggressively expanding capacity from a mere 1,020 MTPA to 13,150 MTPA.

Their client base reads like a carbon footprint index: Oil & Gas, Chemicals, Power, and Automotive. Despite exporting to 32 countries, Italy and Germany make up the bulk of their international shipments. Essentially, they are a proxy for global capex cycles, highly dependent on scrap steel availability, and terrifyingly leveraged to industrial energy costs.

Why does a company with 20,000 MTPA of seamless capacity need an explosive expansion in welded tubes right now? The capex tells a story the income statement hasn’t registered yet.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Mar 2026)

YoY (Mar 2025)

QoQ (Dec 2025)

Revenue

123.57

123.72

152.40

Operating Profit

16.71

17.43

23.01

PAT

6.32

6.83

11.47

EPS

1.05

1.18

1.91

The Q4 numbers are practically flatlined on a YoY basis, and distinctly depressed sequentially. When external shocks hit, commodity converters become price takers, not price makers.

Management was quick to point the finger at a geopolitical disruption in PNG gas supply. According to the CFO, the “plant was completely on the shutdown… for almost 15 to 17 days,” knocking out 40% of their March production volume. Management noted that in the absence of this disruption, revenue “could have been approximately ₹140 crores.”

Furthermore, the operating margin compression (down to 13.5% for the quarter) was directly attributed to commissioning drags. The CFO explicitly stated, “EBITDA declined due to under-absorbed fixed cost from lower utilization of new capacity.” They are building heavy machinery that isn’t running at full tilt yet, effectively paying the mortgage on a house they haven’t fully moved into.

5. Valuation Discussion: Fair Value Range

This fair value range is for educational purposes only and is not investment advice.

With a Current Market Price (CMP) of ₹121.55 and an annualised FY26 EPS of ₹6.48, Scoda Tubes currently trades at a P/E of 18.7x.