1. At a Glance – The Smallcap With Big Hammers

Market cap: ₹100 Cr.

Current price: ₹201.

3-month return: -27.7%.

P/E: 24.6.

ROCE: 11.9%.

ROE: 14.8%.

Debt: ₹89.4 Cr.

Sales (TTM): ₹204 Cr.

PAT (TTM): ₹4.08 Cr.

Welcome to Samrat Forgings Ltd, a ₹100 crore smallcap that forges steel for tractors, trucks, locomotives and earthmovers — and occasionally forges investor patience.

Q3 FY26 (Dec 2025 quarter) revenue came in at ₹49.78 Cr with PAT of ₹1.49 Cr. That’s a 28.4% jump in quarterly profit YoY. Sounds impressive, right? But zoom out — the stock is down 27.7% in three months and 34.3% over one year. The market clearly isn’t clapping.

The company is expanding forging capacity by 80% with a ₹45 Cr capex. It has a new 6,000-ton press line under commissioning. It has credit ratings of IVR BBB-/Stable and A3 for short term facilities. It also received GST notices of ₹8.14 Cr and ₹11.43 Cr earlier… and then got a ₹3.79 Cr demand dropped recently.

So is this a turnaround blacksmith story? Or a leverage-heavy, working-capital hungry metal bender?

Let’s put on our detective coat. Smallcap analysis mode activated.

2. Introduction – The Punjab Forging Factory With Ambition

Samrat Forgings was incorporated in 1991 (as per screener listing section). It manufactures closed-die steel forgings and machined components.

Closed-die forging, for those wondering, means you take red-hot steel, slam it inside shaped dies with hydraulic force, and out pops something that eventually becomes a crankshaft, gear, axle housing or locomotive component.

Basically, industrial protein.

They cater to:

- Swaraj Group

- Ashok Leyland

- Mahindra & Mahindra

- TATA Hitachi

- Diesel Locomotive Works

- Twin Disc, Belgium

Now here’s the interesting bit — top 5 customers contribute around 75% of total sales in FY25. That’s concentration risk. One OEM coughs, Samrat sneezes.

Revenue went from ₹162.34 Cr in FY24 to ₹191.14 Cr in FY25 (as per rating report). EBITDA margin improved from 8.21% to 9.15%. PAT margin? 2.66%. Not exactly luxury margins.

But they are expanding capacity aggressively. New 6,000-ton press. Solar plant. 66 KV substation.

Question for you: When a ₹100 Cr market cap company takes on ₹42+ Cr capex… is that ambition or adrenaline?

Let’s dig deeper.

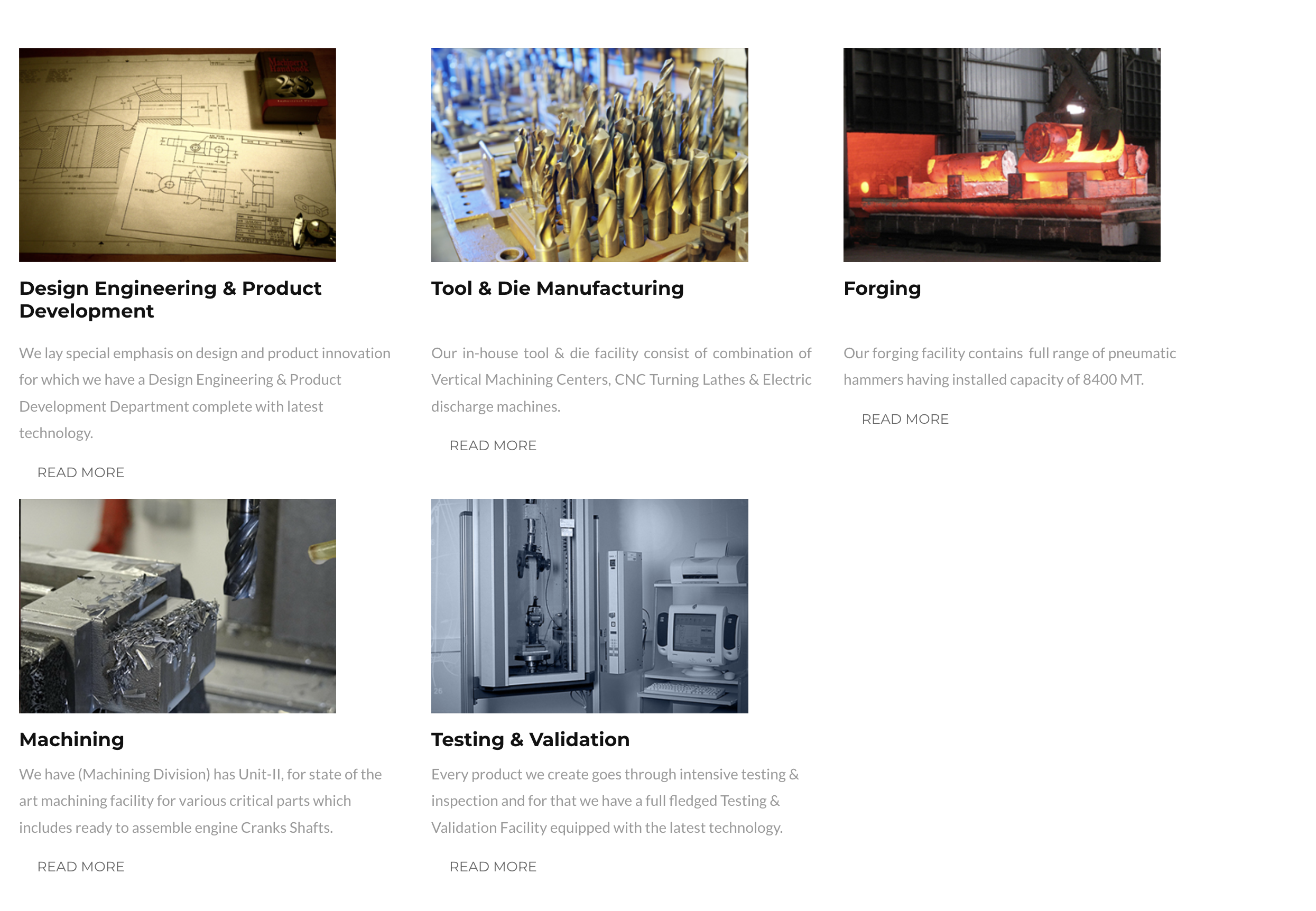

3. Business Model – WTF Do They Even Do?

Imagine this: A tractor company needs crankshafts. They don’t melt steel themselves. They outsource it.

Enter Samrat Forgings.

They:

- Procure steel billets

- Heat them

- Forge into shapes

- Machine components to precise tolerances

- Supply to OEMs

Segments include:

- Automotive: Arm knuckles, gears, axle housings

- Farm equipment: Crankshafts, camshafts

- Oil & energy: Drive shafts, drill bits

- Locomotive: Drive gears, hanging links

- Earthmoving equipment: Ring gears, trunnions

Capacity:

- Forging division: 15,000 MT per annum

- Machining division: 7,000 crankshafts per month

- 50,000 other parts per month

- 6,000-ton forging press under commissioning

This is a classic B2B capital goods supplier. No branding glamour. No retail story. Just metal and margins.

But here’s the