Reliance Power Ltd FY26: A ₹1,662 Crore Guarantee Ghost and the Renewables Pivot

At a Glance

A stark divergence defines the financial landscape of Reliance Power Limited. On one hand, the company features a legacy thermal portfolio operating at high utilization rates; on the other, it faces acute liquidity distress driven by deep-seated subsidiary defaults and intensive regulatory scrutiny. For the financial year ended March 31, 2026, the company reported a consolidated net loss of ₹336.89 crore, a severe reversal from the net profit of ₹2,947.83 crore recorded in FY25. The prior year’s profitability was heavily inflated by an exceptional other income of ₹3,871.07 crore, which vanished in FY26 into a negative ₹12.93 crore. Consolidated revenue from operations stood flat at ₹7,619.71 crore against ₹7,582.89 crore in FY25, highlighting a stagnant top-line growth trajectory.

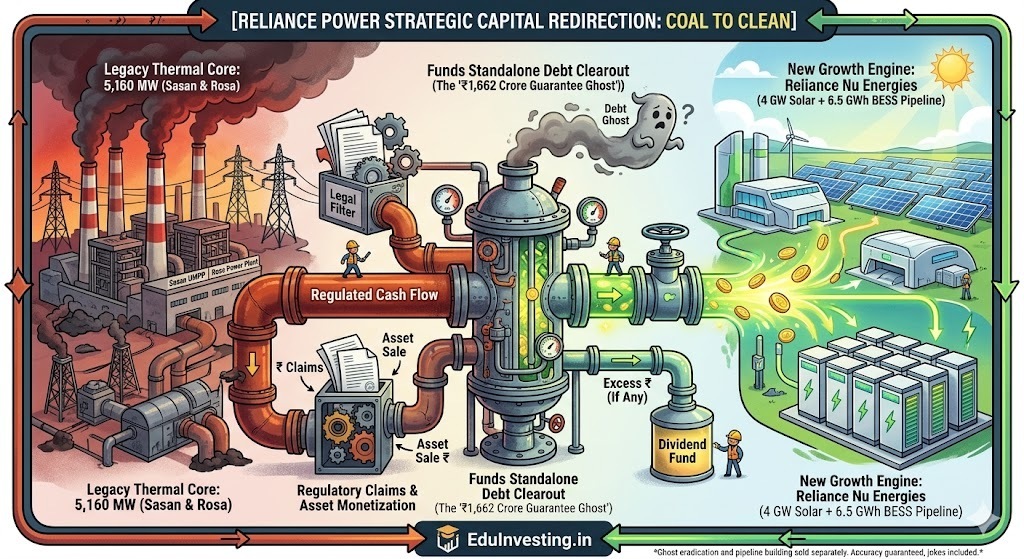

The primary operational anchor remains the 3,960 MW Sasan Ultra Mega Power Project and the 1,200 MW Rosa power plant. However, the consolidated balance sheet remains constrained by total borrowings of ₹14,812.03 crore. While management highlights that standalone operations are bank-debt-free, credit rating agency ICRA has reaffirmed a ‘[ICRA]D’ rating, denoting a state of default. This default is driven by an invoked corporate guarantee of ₹1,641.67 crore (with current legal demands hitting ₹1,662.52 crore) on behalf of its non-operational subsidiary, Samalkot Power Limited.

Compounding the financial friction, the Enforcement Directorate confirmed the provisional attachment of assets worth ₹407.60 crore in May 2026 under anti-money laundering probes related to bank-guarantee frauds. Simultaneously, SEBI initiated a forensic audit of the company on January 14, 2026, over alleged securities violations. Amidst this distress, the company is attempting a structural pivot via its new subsidiary, Reliance Nu Energies, claiming a locked pipeline of 4.0 GW solar and 6.5 GWh Battery Energy Storage Systems (BESS). However, actualizing this pipeline exposes the company to severe capital expenditure execution risks. Financial survival depends on high-risk capital raises, with the board seeking authorizations to raise up to ₹6,000 crore in equity and ₹3,000 crore via debentures. Earnings quality deteriorates when survival relies on asset monetization and equity dilution rather than core operational cash generation.

Introduction

Reliance Power Limited, a prominent entity of the Anil Ambani segment of the Reliance Group, functions as a developer and operator of large-scale power generation projects across India. Historically built on a massive footprint of conventional thermal assets, the company’s capital allocation choices over the last decade have led to a heavily leveraged structure, multiple project delays, and subsequent loan defaults. The legacy portfolio is dominated by coal-fired generation plants tied to long-term Power Purchase Agreements (PPAs) with state-owned power distribution companies (Discoms).

In recent periods, the company has embarked on a corporate transformation agenda, branding itself as a transitioning platform “From Coal to Clean”. This strategy is primarily routed through newly incorporated vehicles like Reliance Nu Energies Private Limited, targeting aggressive bid wins in integrated solar power and utility-scale Battery Energy Storage Systems. Structurally, the promoter holding has settled at 24.98%, with the remaining equity widely distributed among institutional and public shareholders. This analytical breakdown evaluates whether the operational performance of its core thermal cash cows can support its clean energy ambitions while under legal and financial duress.

Business Model: WTF Do They Even Do?

At its core, Reliance Power operates a two-speed business model: generation from legacy thermal units and a conceptualized pipeline of renewable energy platforms. The legacy operational segment consists of 5,305 MW of total capacity, of which 5,160 MW is thermal and a tiny 145 MW is renewable. The heavy lifting is done by the 3,960 MW Sasan Ultra Mega Power Project (UMPP) in Madhya Pradesh, powered by its own captive coal mines, and the 1,200 MW Rosa coal plant in Uttar Pradesh. These plants operate on long-term PPAs, theoretically backed by multi-tier payment security mechanisms like letters of credit and escrows to bypass the chronic cash delays of state Discoms.

The “New Growth Engine” model relies on Reliance Nu Energies. Instead of bidding for generic, ultra-competitive plain vanilla solar projects, the company is targeting integrated premium solutions: Solar + BESS hybrids and Firm and Round-the-Clock (RTC) clean power tenders. The business model intends to monetize dispatchability, where storage capacity commands a premium over regular solar generation.

While the company outlines a locked pipeline including a 930 MW Solar/1,860 MWh BESS project with SECI and cross-border collaborations in Bhutan, these projects currently exist purely on paper and are exposed to intense execution, land acquisition, and financial closure risks.

Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Mar 2026

Dec 2025

Sep 2025

Jun 2025

Mar 2025

Revenue

1,887.26

1,872.84

1,974.03

1,885.58

1,978.01

Operating Profit (EBITDA)

576.29

604.32

617.67

565.04

589.84

Net Profit (PAT)

-494.00

25.11

87.32

44.68

125.57

Reported EPS (₹)

-1.19

0.06

0.21

0.11

0.31

The quarterly trajectory shows structural margin pressure. While revenue has hovered consistently between ₹1,850 crore and ₹1,980 crore, the final quarter of FY26 encountered an absolute breakdown, printing a net loss of ₹494.00 crore. This bottom-line collapse in March 2026 was accelerated by a negative other income line of ₹322.67 crore and elevated interest expenses of ₹474.06 crore. Operating profits have remained bounded around ₹560–₹610 crore per quarter, indicating that while the power plants are running and collecting tariff revenues, the capital structure outside the plants is draining the cash.