Refex Renewables FY26: The Gravity-Defying Solar Play with a ₹42 Crore Negative Net Worth Trap

Section 1 — At a Glance

Refex Renewables & Infrastructure Limited presents a stark juxtaposition of massive stock price appreciation against severely deteriorating financial fundamentals. Over the last five years, the stock has delivered a compounded price CAGR of 35%, yet its operational core has hollowed out entirely, culminating in a devastating consolidated net loss of ₹42.02 crore for FY26. The top-line remains completely stagnant, with FY26 revenue printing at ₹66.47 crore, down from ₹67.02 crore in the previous fiscal, representing a structural inability to scale its solar engineering, procurement, and construction (EPC) business.

Investor intrigue is heavily driven by the promoter group’s aggressive expansion rhetoric, including entries into Compressed Biogas (CBG) and wind energy joint ventures. However, the reality under the hood is a minefield of structural risk signals. The group’s consolidated net worth has been entirely obliterated, closing FY26 at a negative ₹81.52 crore. The balance sheet is heavily overloaded with borrowings of ₹486.80 crore, leading to an acute interest coverage ratio of just 0.28, meaning its operating profits cannot cover a third of its debt service obligations. Furthermore, statutory auditors have issued a severely qualified opinion on the consolidated books, citing a total lack of audit evidence for key liabilities, long-term borrowings, and fixed deposits. Equity value is entirely an illusion when a business operates structurally on life support from promoters. The upcoming chapters will reveal whether this solar vehicle can actually generate cash, or if it is simply a corporate restructuring shell designed to burn capital.

Section 2 — Introduction

Welcome to Refex Renewables & Infrastructure Limited (formerly known as SunEdison Infrastructure, because nothing says fresh start like changing your name after the previous avatar left a trail of structural chaos). Part of the Chennai-based Refex Group, this is an entity that builds rooftop and ground-mounted solar power installations, sets up solar water pumps for farmers, and acts as an Independent Power Producer (IPP).

Historically, this stock traded at a humble ₹5.55 back in 2018. Somewhere along the line, the market looked past its structurally damaged income statement and pushed the share price all the way to a peak of ₹1,183, before a reality check dragged it back down to the current market price of ₹311.85. If you ever wanted to study an enterprise where the stock price behaves like a high-flying tech darling while the underlying balance sheet reads like a distress-assets catalogue, you’ve arrived at your destination. Grab your sunscreen; it gets blindingly bright inside.

Section 3 — Business Model: WTF Do They Even Do?

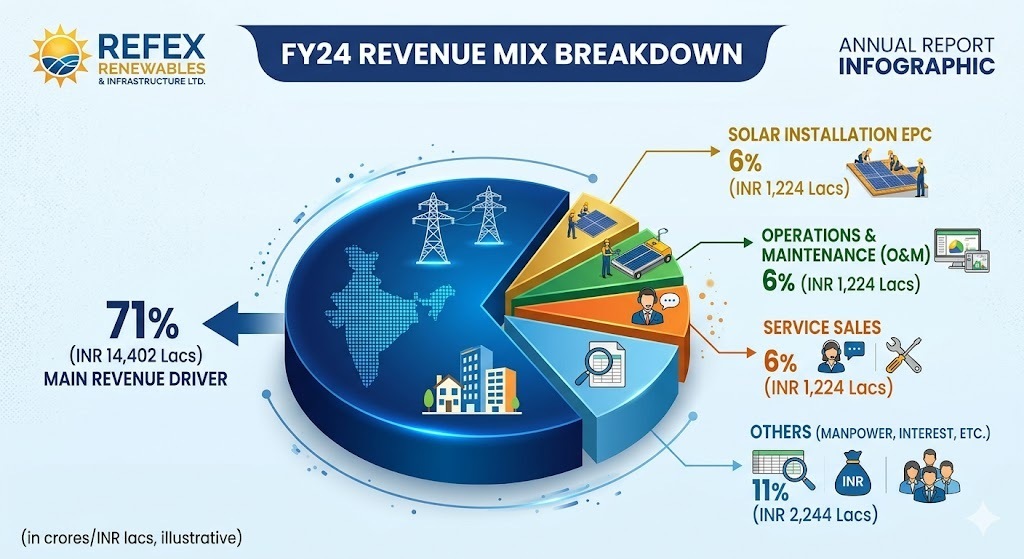

Refex Renewables divides its corporate existence into two main buckets: Commercial & Industrial (C&I) solar power setups—which brings in roughly 87% of segment revenues—and a Rural segment that sets up solar water pumps and home lighting. In FY24, selling actual electricity made up 71% of their top line, while the actual engineering and installation of new solar systems accounted for a minuscule 6%.

In short, they aren’t actively filling an order book with massive new solar projects; they are primarily acting as a landlord for existing panels, collecting power bills. But because keeping things simple doesn’t sound exciting in investor presentations, management has gone on an diversification spree. They’ve signed a Joint Venture to become an Original Equipment Manufacturer (OEM) for wind turbines and are setting up a Compressed Biogas (CBG) plant. Why excel at one capital-intensive, low-margin business when you can simultaneously explore three?

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Mar ’26)

YoY

QoQ

Revenue

₹19.35

-3.59%

+20.19%

EBITDA / Operating Profit

₹8.62

+28.66%

+39.48%

PAT

₹-9.96

-23.57%

+6.13%

Reported EPS

₹-22.14

-23.34%

+6.15%

The top line for the March 2026 quarter came in at ₹19.35 crore, down from ₹20.07 crore in the same period last year. While Operating Profit managed to look lively at ₹8.62 crore due to a reduction in raw material consumption, the bottom