RateGain Travel FY26: A ₹1,824 Crore Tech Flywheel Powered by a Massive $250 Million Bet

Section 1 — At a Glance

RateGain Travel Technologies delivered a massive headline performance in FY26, scaling its annual consolidated revenue to ₹1,823.55 crore—a staggering 69.41% jump over the previous fiscal year. This explosive topline surge was powered by the strategic integration of US-based Sojern Inc., a landmark $250 million acquisition completed in November 2025 that fundamentally altered the company’s financial and operational architecture. Yet, underneath this breathtaking expansion lies a distinct web of financial adjustments and structural transitions that investors are parsing with intense scrutiny.

While reported net profit dipped slightly by 6.96% to ₹194.39 crore due to high transaction-related exceptional costs and integration expenses, management’s adjusted profit after tax—which normalized for the deferred deal consideration of the Sojern buyout—reached a far healthier ₹249.90 crore. This structural inflection point marks a clear transformation from a pure-play connectivity vendor into a heavyweight AI-driven operating system for the global travel and hospitality value chain.

However, the balance sheet has absorbed significant dramatic shifts to support this leap. Total borrowings surged from just ₹16.05 crore to a formidable ₹948.70 crore, heavily altering the risk profile of a previously asset-light software enterprise. Additionally, cash equivalents fell from ₹349.63 crore to ₹173.13 crore as internal cash was aggressively deployed. True corporate maturity is measured by how effectively scale dilutes fixed structural friction into pure earnings. The critical narrative here is no longer about maintaining lean insulation, but rather whether RateGain can extract high-margin synergies from its massive new platform before financing and amortization lines drag down its returns.

Section 2 — Introduction

RateGain Travel Technologies Ltd has firmly positioned itself as the largest Software as a Service (SaaS) provider in the travel and hospitality industry in India, operating an interconnected global network that spans across vital booking channels]. Over the years, the company has transitioned from a localized tech utility into a mission-critical infrastructure provider connecting global travel intermediaries, airlines, car rental agencies, and cruise lines[8]].

The modern travel landscape requires real-time agility, and RateGain acts as the digital nervous system that processes competitive pricing, automates inventory updates, and orchestrates performance marketing campaigns at scale][2]. Rather than resting on its legacy laurels, the organization spent the latter half of the fiscal year absorbing international assets and retiring legacy frameworks, explicitly pursuing global enterprise clients and expanding its geographical footprint across North America and Europe.

Section 3 — Business Model: WTF Do They Even Do?

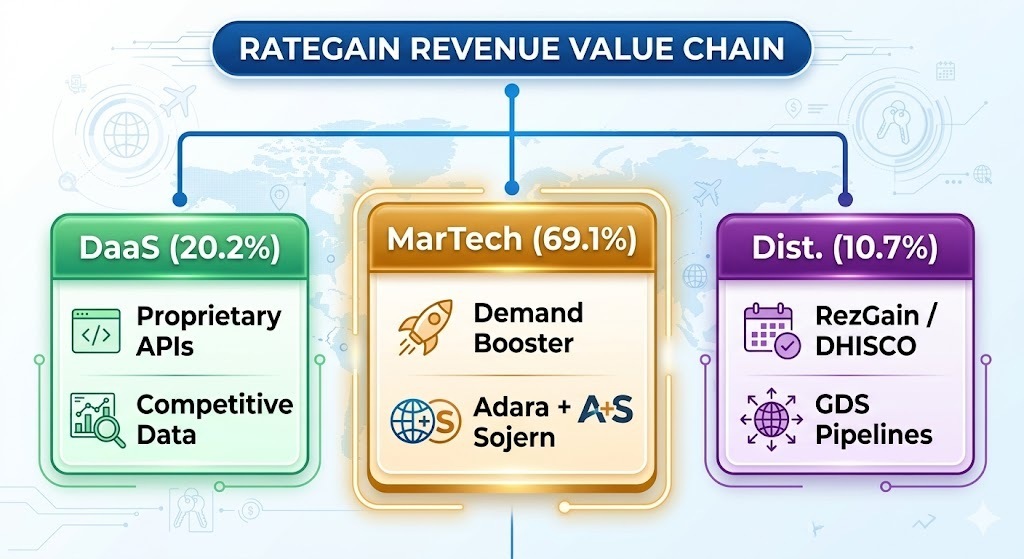

If you think RateGain simply writes software for travel agents, you are missing the entire multi-layered plot. They run a three-headed B2B travel engine designed to capture money no matter how or where you book a trip.

First up is Data as a Service (DaaS), accounting for 20.2% of the mix. This is their legal corporate espionage wing. It uses proprietary technology and API connections to constantly scrape hotel rooms, car rentals, and airline tickets globally, giving clients real-time competitive pricing data so they do not accidentally undercharge for a suite during peak tourist season].

Second is Distribution, making up 10.7%. Think of this as the digital plumbing of the travel industry. Through core products like RezGain and DHISCO, it links roughly 1,91,000 properties to over 400 global demand channels, seamlessly transmitting room availability, inventory rates, and confirmations back and forth It has two products in this space -RezGain & DHISCO. [3]]. It is a transaction and subscription heavy plumbing business where they charge for every reservation moving down the pipes.

Finally, the monster of the house: Marketing Technology (MarTech), commanding a massive 69.1% of the pie following the Sojern acquisition. MarTech provides digital marketing suites and performance advertising tools that use deep travel-intent data to target high-value travelers before they click book on a competitor’s app, Performance marketing operation leveraging the travel -intent data].

Section 4 — Financials Overview

Basis of Presentation: Figures are consolidated, expressed in ₹ crore unless explicitly designated otherwise.

RateGain’s latest financial performance reflects the heavy, non-linear impact of consolidating an international heavyweight into its regular financial reporting lines.

Headline Financial Performance

Metric

Latest Quarter (Q4 FY26)

YoY Change (%)

QoQ Change (%)

Revenue

₹715.55

+174.48%

+32.50%

EBITDA (Reported)

₹147.04

+142.64%

+68.83%

Net Profit (PAT)

₹69.99

+27.70%

+164.61%

Reported EPS (₹)

₹5.92

+39.62%

+164.29%

The business recorded its highest-ever quarterly sales of ₹715.55 crore, expanding by a breathtaking 174.48% compared to Q4 FY25. This dramatic leap represents the structural inclusion of a full quarter of Sojern’s operations, transforming the baseline characteristics of the corporate income statement. Meanwhile, legacy organic revenue stood resiliently at ₹311.00 crore, growing at a comfortable 19.30% clip as it reclaimed double-digit momentum.

EBITDA margins for the quarter settled at 20.55%, though management was quick to highlight an adjusted EBITDA margin of 23.50% once the ₹20.90 crore quarterly drag from earnout-related deferred considerations was backed out.