Mufin Green Finance Q4 FY26: A ₹1,398 Crore Debt Engine Chasing Green Horizons

The market has a fascinating way of pricing the future when the present is still trying to balance its books. Mufin Green Finance Limited closed its fiscal year 2026 with a performance that managed to look simultaneously spectacular on the top line and exceptionally expensive on the valuation dial. With a market capitalization sitting at ₹2,191.20 crore and a closing price of ₹126.49, the company has transitioned from a sleepy investment shell into a hyperactive lending machine catering to green mobility, healthcare premiums, and corporate borrowers.

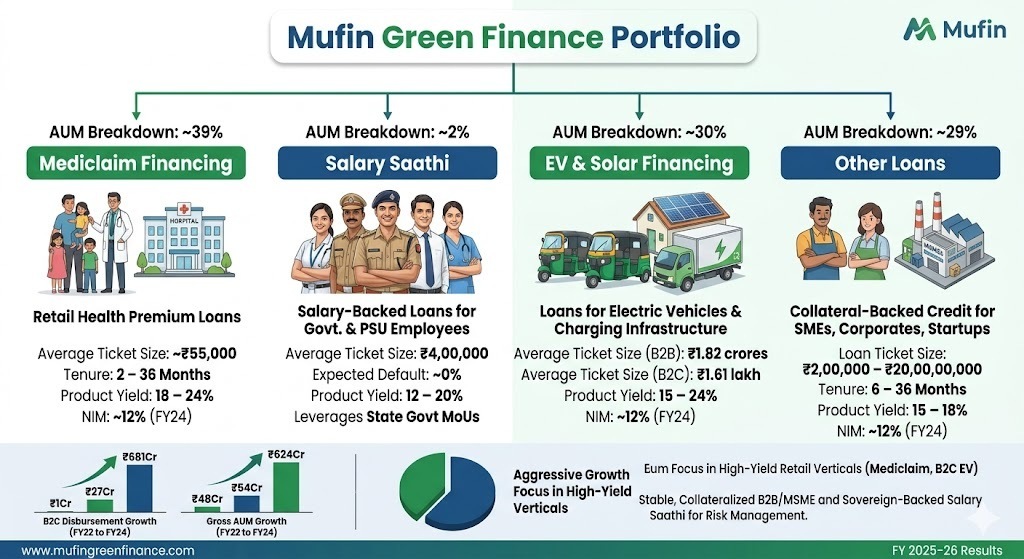

The structural evolution is hard to miss. Assets Under Management (AUM) surged to ₹1,541.17 crore, fueled by an aggressive push into Mediclaim financing, which now anchors 39% of the total portfolio. Yet, underneath the narrative of green transition and point-of-sale financial engineering lies a foundational reality: this is a business running on high-cost fuel. Total borrowings climbed to ₹1,397.60 crore , keeping the debt-to-equity ratio tightly coiled at 2.43x , while the interest coverage ratio remains a thin 1.32x. Investors are currently paying a premium that demands flawless execution, leaving little room for collection friction or macro speed bumps.

Financial leverage can look like genius during an expansionary phase, but it binds capital efficiency to strict operational discipline. Mufin’s Return on Equity (ROE) stands at a muted 6.69% , creating an obvious divergence against its premium multi-year price-to-earnings multiple. The coming quarters will determine whether the operational leverage gained by shrinking headcount can expand margins fast enough to justify the equity market’s enthusiasm.

Introduction

Mufin Green Finance Limited, originally incorporated as APM Finvest, has undergone a radical identity shift. Once a standard non-banking financial company focused on generic investments and loans, the entity was acquired by Hindon Mercantile Limited in March 2022. Since the acquisition, management has aggressively pivoted the balance sheet toward climate-sustainable products, electric vehicle ecosystems, and embedded retail health insurance financing.

Operating out of its headquarters in New Delhi, the company has expanded its geographical presence to cover multiple states with a rapidly growing active borrower base. The strategic pivot is clear: find niche, high-yield credit segments where mainstream commercial banks hesitate to underwrite risk, and embed financing directly into the transaction point. Over the last two fiscal years, this has manifested as a massive disbursement engine, though the rapid build-up of the book means that a significant portion of its loans has not yet been tested through a full credit cycle.

Business Model: WTF Do They Even Do?

If you listen to the investor presentations, Mufin Green Finance is an eco-warrior disguised as a financial institution. If you look at the ledger, it is an algorithmic pawnshop for high-yield niche credit. The company splits its operations across two distinct transactional architectures: B2B asset leasing and B2C retail financing.

Under the B2B umbrella, Mufin operates a fleet leasing model where it retains ownership of electric vehicles, charging infrastructure, and swappable batteries, leasing them directly to commercial operators. On the B2C side, it works through original equipment manufacturers (OEMs) and dealership networks to provide point-of-sale retail retail EV loans.

To prevent the EV book from becoming a singular risk vector, management introduced “Mediclaim Financing” in early 2025. This product splits large, annual health insurance premiums into predictable monthly EMIs at the point of sale, capturing yields between 18% and 24%. While it sounds sophisticated, it is fundamentally a high-yield retail play designed to balance out the slower-moving asset-backed green portfolio. The newest experiment, “Salary Saathi,” targets government and PSU employees by deducting loan repayments directly at the payroll source, attempting to extract high single-digit yields with theoretically low default parameters.

Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4 FY26)

YoY (%)

QoQ (%)

Revenue

64.66

100.74%

22.11%

EBITDA / Operating Profit

52.96

131.37%

28.51%

PAT

11.09

173.83%

58.20%

EPS (₹)

0.64

156.00%

60.00%

The top-line momentum continued its upward trajectory in Q4 FY26, with quarterly revenue reaching ₹64.66 crore compared to ₹32.21 crore in the corresponding quarter of the previous fiscal year. Operating profits kept pace, jumping to ₹52.96 crore as digital onboarding paths for the health insurance segment limited structural expense growth. Net profit for the final quarter landed at ₹11.09 crore, an acceleration reflecting the higher yields derived from the point-of-sale retail book.

Financial Wisdom Drop: Headline earnings growth in an early-stage financial firm tells you how fast they are writing checks,