Laxmi Dental Q4 FY26: The ₹10.1 Crore Reality Check for Premium Appraisals

Section 1 — At a Glance

Laxmi Dental Limited’s latest financial closure presents a stark contrast between accelerating operating execution and the unyielding expectations of a post-IPO market evaluation. Landing on the stock exchanges in January 2025 after a ₹698 crore capital raise, the company concluded its first full financial year with a Q4 FY26 revenue performance of ₹74.0 crore. This represented a 21.9% expansion over the matching three-month stretch from the prior year, signaling a visible operational rebound from a notably depressed third quarter. Net profit for the final quarter came in at ₹10.1 crore, outstripping the low-base ₹4.3 crore of the previous year’s matching period, but carrying a one-off tax normalization benefit linked to previous labor code provisions.

For the complete span of FY26, aggregate operational revenues climbed to ₹278.0 crore against ₹239.1 crore in FY25. This 16.2% top-line appreciation was driven primarily by international laboratory exports and the ongoing integration of digital hardware into domestic networks. However, full-year consolidated margins felt the weight of global supply dynamics. Profit after tax for FY26 closed at ₹28.9 crore, registering a decline from the ₹33.4 crore reported in FY25.

Investor attention remains intensely anchored to the structural transformation of the business model from a service-oriented dental laboratory into a medical technology and branded consumer healthcare enterprise. While the deployment of automated intraoral scanners acts as an essential catalyst for domestic laboratory market share capture, it simultaneously exerts downward pressure on consolidated gross margins. Furthermore, the company faces intensifying domestic price competition within its clear aligner division alongside structural shifts in working capital deployment. When a newly capitalized enterprise experiences capital inflation ahead of free cash flow generation, a divergence between nominal accounting growth and structural equity efficiency routinely emerges. The primary operational question is whether the current investment cycle will yield scalable economic leverage or simply increase asset density across an inherently fragmented healthcare landscape.

Section 2 — Introduction

Laxmi Dental Limited occupies a unique and highly specialized niche within the Indian healthcare manufacturing sector. Founded in 2004, the corporate journey began far more modestly in 1989 as a localized, manual dental laboratory. Over the subsequent decades, the company systematically consolidated its operational footprint to position itself as an integrated designer and fabricator of custom dental prosthetics, clear orthodontic aligners, and specialized pediatric dental crowns.

Following its public listing in early 2025, management has embarked on an aggressive capital deployment strategy focused on structural digitization and automated domestic laboratory expansion. The business operates an export-oriented infrastructure, sending custom crowns and material sheets to over 95 countries while maintaining a domestic service grid that connects with thousands of dental clinics. As the corporate identity transitions from a private manufacturing boutique to a highly visible public entity, the operational mandate has shifted from mere volume generation to the defense of capital allocation efficiency under the watch of an institutional shareholder base.

Section 3 — Business Model: WTF Do They Even Do?

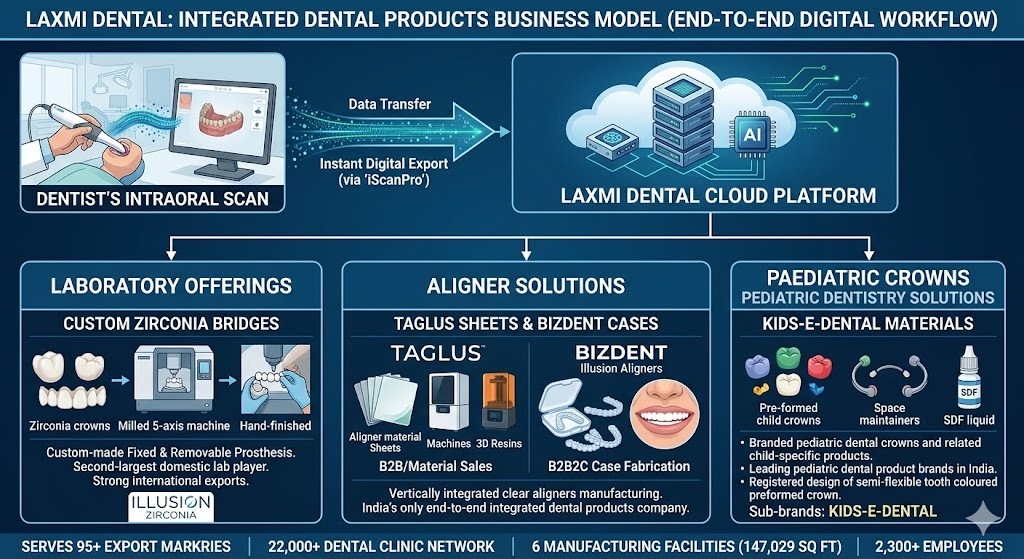

To the uninitiated, dental care looks like a straightforward relationship between a patient, a high-speed drill, and an expensive leather chair. In reality, your dentist is merely the retail storefront for an industrial assembly line. Laxmi Dental acts as the hidden engine behind that storefront, operating across three distinct segments that range from traditional manufacturing to high-tech software monetization.

First, they run a Laboratory Business. When a dentist takes an impression of your broken tooth, they send the digital file or physical mold to Laxmi. The company’s six manufacturing facilities then custom-mill structural crowns and bridges under brands like Illusion Zirconia.

Second, they operate the Aligner Solutions segment. This involves fabricating those invisible plastic trays that masquerade as braces (Bizdent), while simultaneously selling the underlying thermoforming plastic sheets and 3D resins (Taglus) to external competitors. It is a classic “selling shovels during a gold rush” strategy, ensuring they profit whether their own consumer aligner brand wins or loses.

Finally, they cater to Paediatric Dentistry via Kids-E-Dental, manufacturing pre-formed child crowns and silver diamine fluoride to arrest cavities before they become root canals. To accelerate this entire wheel, Laxmi deliberately dumps low-margin iScanPro intraoral scanners into dental clinics. The hardware itself barely makes a profit, but it effectively locks the doctor into Laxmi’s digital ecosystem, transforming an analog medical service into a highly sticky, recurring manufacturing pipeline.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Headline Performance Metrics

Metric

Latest Quarter (Q4 FY26)

YoY Change (%)

QoQ Change (%)

Revenue

₹74.0

+21.9%

+12.1%

EBITDA / Operating Profit

₹13.5

+41.8%

-3.6%

PAT

₹10.1

+134.9%

+1,022.2%

EPS (Reported)

₹1.83

+134.6%

+408.3%

The top-line progression to ₹74.0 crore for the quarter marks a steady operational recovery from the preceding quarter’s macroeconomic disruption. Operating profits grew to ₹13.5 crore, supported by an expanding share of high-margin, metal-free international laboratory volumes which grew 40.9% year-on-year in Q4.

The net profit line of ₹10.1 crore appears spectacularly inflated on a sequential basis, though a meaningful portion of this dramatic surge stems from a reversal of the previous quarter’s financial dynamics. In Q3 FY26, earnings were severely depressed by a one-time exceptional provision of ₹5.8 crore for gratuity liabilities under the new labor code, which was subsequently countered in Q4 by a ₹1.3 crore tax normalization benefit.

What is Management Promising in the Coming Quarters?

During the May 2026 conference call, executive management maintained a defensive yet optimistic stance regarding future margin evolution. Commenting on the competitive pricing pressure that has battered the domestic aligner segment, the CEO noted that pricing trends are “getting normalized in the running quarter” and that they took a deliberate, “balanced approach” to preserve gross margins rather than chasing unprofitable market share.

Furthermore, management highlighted the deployment of their newly launched iScope 360 remote monitoring platform, expecting it to drive higher compliance and pull-through volumes for their lab business. When pressed for hard numeric revenue and margin guidance for FY27, the CEO deflected structural commitments, stating, “I wish I could guide you,” but confirmed that internal automation investments will ensure that over the next two to three years, “people cost will be disproportional to the sales.”

Section 5 — Valuation Discussion: Fair Value Range Only

To evaluate Laxmi Dental’s current equity pricing without falling into the trap of post-IPO euphoria, we must anchor our assumptions to the actual normalized earnings power demonstrated in the trailing twelve months.

With 5.50 crore adjusted equity shares outstanding and a full-year FY26 net profit of ₹28.9 crore, the company’s full-year reported EPS stands at ₹5.25. At the closing market price of ₹233, the stock trades at an implied P/E multiple of 44.4x, slightly higher than the trailing Screener automated calculation of 38.2x which relies on unadjusted historical buckets.