Lakshmi Mills Mar 2026: Hidden Textile Landlord Boasts a ₹755 Crore Liquid Safety Net

Section 1 — At a Glance

Lakshmi Mills Company Ltd (LMC) reported a consolidated revenue from operations of ₹242 crore for the full fiscal year ended March 31, 2026, marking a top-line decline of 8.11% compared to ₹263 crore in the previous fiscal year. Despite the contraction in core textile sales, the company pulled off an operating profit (EBITDA) of ₹28 crore, reflecting a notable margin expansion to 11.32% from 8% in the preceding period. However, heavy historical capital costs and underlying operational volatility resulted in a reported annual net loss of ₹16 crore, following a ₹5 crore loss in the prior year.

The stock is currently generating strong investor attention primarily because of its deep asset backing and real estate transformation, trading at a meaningful discount to its book value of ₹10,240. The company’s prime real estate in the heart of Coimbatore has been converted into a lucrative multi-outlet rental hub hosting premier retail brands, which brought in a steady stream of lease rental income alongside its core spinning business. Yet, structural worries persist, driven by low interest coverage, historical return on equity remaining in negative territory, and cyclical demand shocks in the textile sector that triggered a 25% production cutback during the broader cycle.

Evaluating asset-rich legacy businesses requires shifting the analytical gaze away from the temporary distortions of the income statement to the replacement cost of the underlying balance sheet. This piece explores whether LMC is a classic value trap or a deeply mispriced real estate fortress.

Section 2 — Introduction

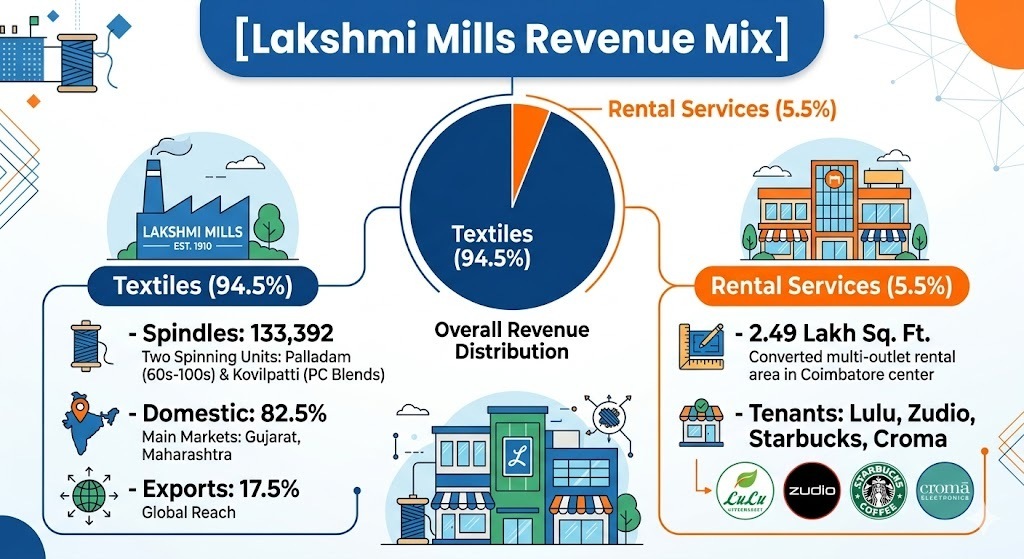

Established in 1910, Lakshmi Mills Company Ltd is one of South India’s oldest legacy textile players. For over a century, the company built its reputation around spinning premium cotton and polyester-blended yarns across its Palladam and Kovilpatti manufacturing facilities in Tamil Nadu. But as global textile supply chains shifted and raw material volatility eroded manufacturing spreads, the company quietly initiated a structural pivot: turning its idled factory lands into high-yielding commercial real estate.

The publication of the audited financial results for the period ended March 31, 2026, brings this duality into sharp relief. While the spinning mills are grappling with an industry-wide slowdown, the rental division is scaling up, bolstered by a fresh ₹91 crore commercial expansion project and a strategic asset liquidation program that cleaned up the balance sheet. This analysis untangles the operational metrics of its manufacturing units from the massive hidden value of its corporate investment portfolio and urban land bank.

Section 3 — Business Model: WTF Do They Even Do?

To the untrained eye, Lakshmi Mills is an old-school textile mill churning out cotton yarn, polyester-cotton blends, slub yarns, and industrial fabrics ranging from school uniforms to specialised hospital aprons. It runs 133,392 spindles across two main locations, managing a delicate balancing act against the volatile prices of raw cotton and petrochemical derivatives. Textiles still generate the lion’s share of the top line, accounting for 94.5% of total revenue.