Indian Oil Corporation Ltd FY26: The ₹42,096 Crore Maharatna Engine Fires on All Cylinders

Section 1 — At a Glance

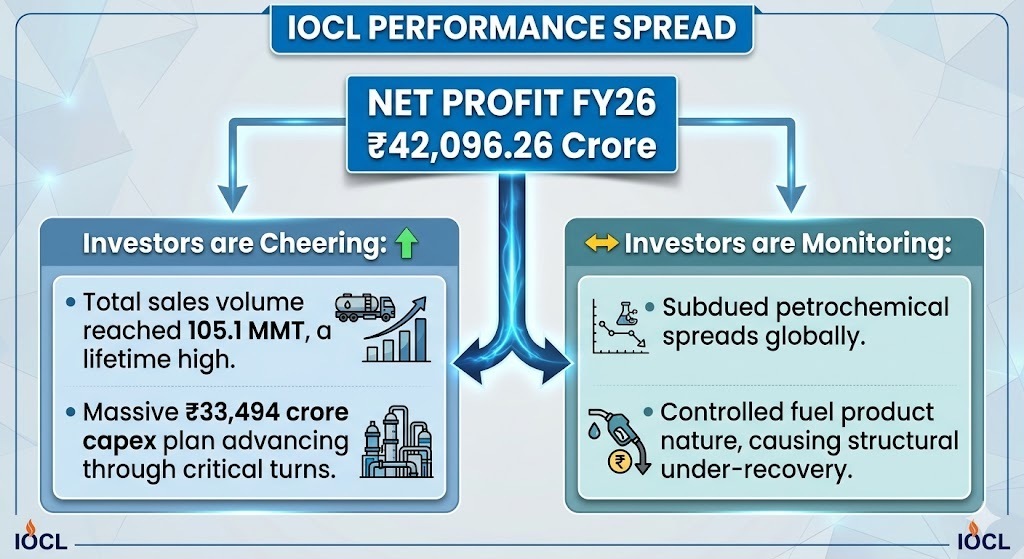

Indian Oil Corporation Ltd (IOCL) locked in a powerful fiscal performance for the year ended March 31, 2026, delivering an annual Net Profit of ₹42,096.26 crore. This structural resurgence stands out as a sharp contrast to the volatile trailing twelve months, driven by robust domestic consumption and high-visibility capacity utilization across its core infrastructure assets.

The frontline narrative reveals an operational apparatus running at absolute limits. The market is carefully weighing IOCL’s massive multi-location brownfield expansion track against structurally capped marketing margins on sensitive domestic fuel products. Earnings visibility remains structurally superior when compared to past multi-quarter cyclical troughs. Real capital efficiency is achieved when massive scale absorbs volatile macro inputs without burning through institutional equity. A look ahead suggests that the immediate trajectory hinges on whether regional product crack spreads can comfortably absorb the impending execution of its ambitious brownfield supply additions.

Section 2 — Introduction

Indian Oil Corporation Ltd commands a dominant, government-controlled Maharatna position across India’s hydrocarbon value chain. Straddling everything from crude exploration and cross-country pipeline networks to refining and deep-retail marketing, the company operates as the foundational energy baseline for the domestic economy.

The primary reason for evaluating the firm at this juncture is its aggressive brownfield transition strategy. IOCL is currently processing a multi-billion dollar capital expenditure pipeline focused on expanding refining limits, upgrading downstream petrochemical footprint, and scaling green hydrogen infrastructure to capture shifting consumer preferences.

Section 3 — Business Model: WTF Do They Even Do?

IOCL turns crude oil into consumer fuels, industrial polymers, and commercial gases via an integrated value chain. The business operates through three clearly divided segments:

Petroleum Products: This is the absolute powerhouse, accounting for roughly 94% of top-line revenue. The firm acts as the primary distributor of high-speed diesel, motor spirit, and liquefied petroleum gas across India via a retail infrastructure footprint that controls 42% of all domestic fuel outlets.

Petrochemicals: Contributing roughly 3% of revenue, this segment produces polymers and chemical intermediates under specialized brands like PROPEL and CYCLOPLAST.

Other Businesses: A mix of natural gas marketing, upstream oil exploration assets, and a bulk explosives manufacturing unit that services core heavy industry.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Headline Performance

Metric

Latest Quarter (Mar 2026)

YoY

QoQ

Revenue

2,08,289.26

6.67%

1.53%

Operating Profit

24,803.80

65.04%

9.05%

PAT

14,458.08

78.00%

11.16%

EPS (₹)

10.24

78.09%

11.18%

(Note: YoY and QoQ changes computed directly from consolidated quarterly disclosures.)

The financial records highlight a profound bottom-line expansion during the final quarter of the fiscal year. Sequential growth points to stabilized domestic inventory valuations and favorable real-world logistics pricing optimization. Quarterly trends reflect accurate underlying corporate performance only when operational