Ganesh Green Bharat H2 FY26: A 242% Sales Jump or Just High-Voltage Drama?

Section 1 — At a Glance

Ganesh Green Bharat Limited (GGBL) is displaying an extraordinary operational expansion that has rapidly caught the attention of the broader market. Headline numbers for the full financial year ending March 31, 2026, show a spectacular top-line surge, with revenue skyrocketing by 242% to reach ₹1,064.73 crore compared to ₹311.39 crore in the previous fiscal year. Net profit for the same period followed a similarly explosive trajectory, growing by 154% to touch ₹75.15 crore, up from ₹29.62 crore in FY25. This dramatic growth has driven the company’s annual basic earnings per share (EPS) to ₹30.31. This explosive expansion is primarily underpinned by the massive scaling up and commissioning of its solar photovoltaic (PV) module manufacturing capacity in Mehsana, Gujarat, which reached an operational milestone of 1.1 GW in late November 2025.

However, beneath this blinding operational glare, sophisticated market observers are tracking significant undercurrents of financial stress. While the top-line expanded exponentially, the company’s operating profit margin (OPM) compressed noticeably to 10.4% in FY26 from 14.0% in the previous year. This structural shift indicates a business model increasingly exposed to intense raw material cost pressures and highly aggressive competitive bidding conditions. Furthermore, working capital intensity is rising significantly. Inventories have ballooned over the last twelve months to ₹169.98 crore, locking up deep tranches of liquidity. Massive growth often acts as a temporary screen for operational inefficiency, hiding structural vulnerabilities until cash flow cycles begin to tighten. Whether GGBL can successfully translate these massive public contract orders into actual free cash flow—rather than letting it sit on the balance sheet as frozen inventory—remains the central question for long-term equity investors.

Section 2 — Introduction

Ganesh Green Bharat Limited, originally incorporated in 2016, has evolved from a small-scale electrical contracting outfit into a specialized renewable infrastructure player. The company operates a multi-pronged business model across four core verticals: solar PV module manufacturing, solar engineering, procurement, and construction (EPC) allied services, electrical grid contracting, and rural water supply scheme projects.

Management has recently executed an aggressive pivot away from purely service-led EPC contracts toward automated manufacturing. This transformation has been heavily funded through public equity markets, following the company’s listing on the NSE SME Emerge platform in July 2024, which infused ₹125 crore into its capital structure. While the company has historically managed low-overhead government contracting, it is now operating a capital-intensive manufacturing business. This strategic transition introduces entirely new balance sheet dynamics, including technology obsolescence risks, global supply chain bottlenecks, and direct structural vulnerability to international raw material pricing cycles.

Section 3 — Business Model: WTF Do They Even Do?

To understand Ganesh Green Bharat, you have to realize they are trying to be a renewable energy ecosystem, an electrical contractor, and a rural plumber all at the exact same time.

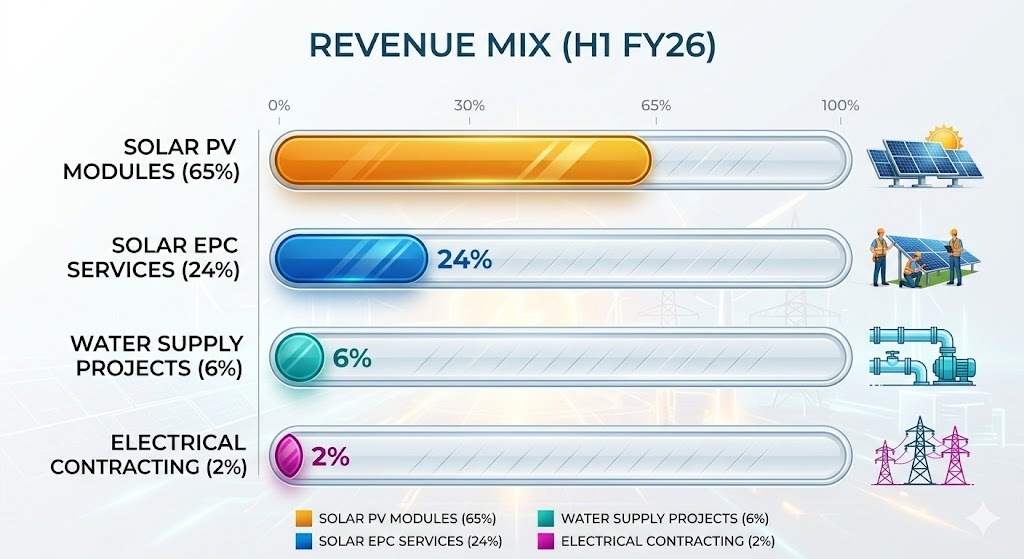

The revenue engine has fundamentally transformed over the past two fiscal years. In FY24, the business was reasonably diversified: solar PV modules brought in 53% of revenue, electrical contracting took up 30%, solar EPC services sat at 11%, and water supply schemes pulled up the rear at 6%. Fast forward to H1 FY26, and solar PV modules have completely devoured the mix, accounting for 65% of the total revenue. Solar EPC allied services (think solar water pumps and rooftop installations under government schemes like KUSUM) bring in another 24%, while water supply projects stand at 6%, and electrical contracting has dwindled down to a rounding error of 2%.

Geographically, the company is deeply infatuated with its home turf, drawing 47% of its historical revenue from Gujarat, with minor adventures into Punjab (16%), Chhattisgarh (13%), and Uttar Pradesh (7%). Their customer acquisition model relies on bidding directly for government contracts (28%), picking up crumbs via sub-contracts from larger infrastructure players (29%), and direct B2B module sales to commercial installers (44%). Essentially, they manufacture solar panels to feed their own internal EPC projects and sell the surplus to external buyers. It sounds beautifully integrated until you realize they are heavily dependent on government tender design and state utility budgets.