GAIL (India) FY26: A Story of High Tariffs, Deep Gas Losses, and Chokepoint Drama

1. At a Glance

The financial year 2026 was a masterclass in macroeconomic irony for GAIL (India) Limited. On one hand, the state-owned gas giant was handed a structural lifeline by the Petroleum and Natural Gas Regulatory Board (PNGRB) via an interim tariff hike for its integrated pipeline network, boosting the base rate from ₹58.61 to ₹65.69/MMBTU. On the other hand, global geopolitical disruptions severely tested the company’s operating resilience.

The outbreak of conflict in West Asia on February 28, 2026, and the subsequent blockade of the Strait of Hormuz completely upended the global supply chain for liquefied natural gas (LNG). With Qatar and the UAE traditionally supplying nearly 60% of India’s LNG imports, the invocation of force majeure by Petronet LNG Limited (PLL) on Qatari supplies left GAIL navigating restricted availability and severely pinched transmission and marketing volumes.

Financially, the pressures became starkly apparent in the tail end of the year. Consolidated revenue for FY26 stood flat at ₹1,41,597.72 crore compared to ₹1,41,903.49 crore in FY25. However, consolidated net profit slid significantly by 39.1% to ₹7,582.47 crore down from the previous year’s ₹12,449.80 crore. This compression was driven by a painful spike in input gas costs, a weakening rupee, and a massive non-operating hit captured under other expenses.

While the core pipeline business remains fundamentally protected by regulated returns, GAIL’s downstream petrochemical operations have transformed into a severe margin drag. The market is now looking past the near-term volume bottlenecks to see if the massive capital expenditure program can successfully pivot the company toward diversified international sourcing and a broader clean energy footprint.

2. Introduction

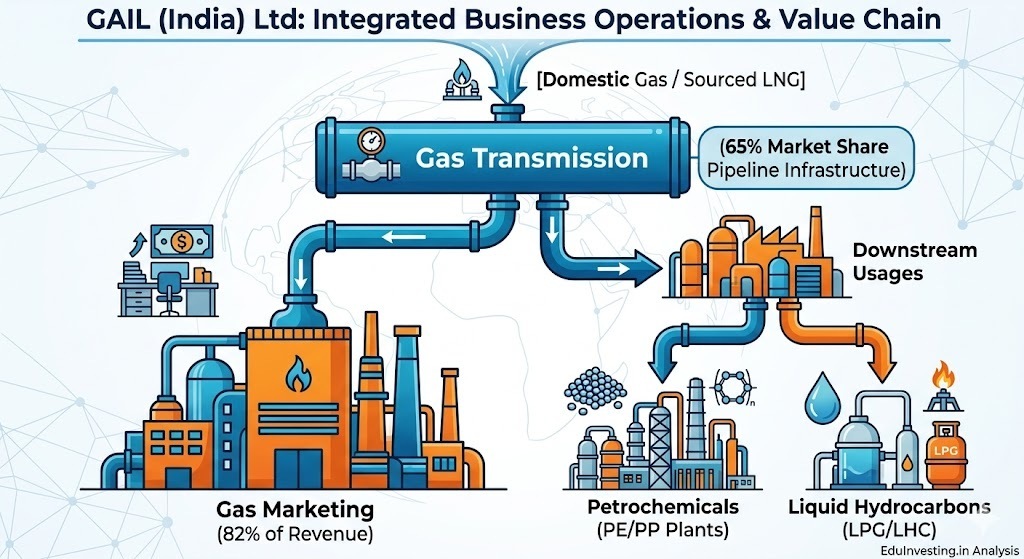

GAIL (India) Limited occupies a uniquely monopolistic, yet structurally complex, position within India’s energy architecture. Originally incorporated in 1984 as a state-owned pipeline utility, the maharatna PSU has expanded vertically across the entire natural gas value chain. Today, it functions as an integrated energy conglomerate, running a network of over 11,500 km of natural gas trunk lines, 2,300 km of LPG pipelines, six gas processing facilities, and a major downstream petrochemical complex.

The corporate architecture is heavily tethered to public service mandates, acting as the primary execution arm for the government’s “One Nation-One Grid” pipeline connectivity master plan. However, operating a strategic utility comes with structural volatility, as GAIL must constantly balance domestic regulatory tariff constraints with wild fluctuations in international energy benchmarks like Henry Hub and Brent crude. The current fiscal year represents a major strategic juncture, as a comprehensive leadership change—marked by Deepak Gupta taking over the reins as Chairman and Managing Director on March 1, 2026—coincides with the company’s heaviest commissioning slate for petrochemical expansions and renewable energy joint ventures.

3. Business Model: WTF Do They Even Do?

GAIL’s business model is essentially an exercise in corporate split personalities. To help unpack how this asset-heavy infrastructure giant actually functions, it helps to look at how its processing networks physically link production to consumption.

The company is structured around four primary moving parts, each with completely different margin profiles and risk drivers:

Natural Gas Transmission: This is the crown jewel. GAIL owns and runs approximately 65% of India’s natural gas pipeline infrastructure. It charges a regulated tariff to move gas from ports and domestic fields to industrial consumers. It is a classic toll-booth model where profit is purely a function of volume throughput and regulatory approvals.

Natural Gas Marketing: While transmission provides the steady cash, marketing drives the top-line scale, accounting for a massive 82% of gross revenue. GAIL buys LNG globally via long-term contracts or spot markets and sells it to domestic fertilizer plants, power stations, and city gas networks. When global supply gluts occur, this segment thrives on trading margins; when geopolitical chokepoints close, it triggers expensive sourcing substitutions.

Petrochemicals: GAIL processes natural gas into polyethylene (PE) and polypropylene (PP) at its Pata plant and via its subsidiary, Brahmaputra Cracker and Polymer Limited (BCPL). This segment exists to add value to raw gas, but it is highly cyclical and vulnerable to international plastic pricing drops.

LPG and Liquid Hydrocarbons (LHC): The company extracts LPG, propane, and pentane from raw gas streams across four processing units. It also runs a high-utilization pipeline network dedicated purely to transporting LPG for oil marketing companies.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Headline Results

Metric

Latest Quarter (Mar 2026)

YoY (%)

QoQ (%)

Revenue

35,576.55

2.37%

1.15%

EBITDA / Operating Profit

1,453.39

-59.64%

-50.35%

PAT

1,484.72

-40.40%

-15.46%

Reported EPS (₹)

2.26

-39.73%

-15.36%

The trailing quarter tells a very clear story of operating margin compression. While revenue remained stable, hovering around the ₹35,500 crore mark due to fixed transmission contractual volumes,