CWD Ltd FY26: Revenue Explodes 346% While Capacity Triples

General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

1. At a Glance

The numbers are violent. CWD’s FY26 revenue reached ₹147 crore—a 346% jump from ₹33 crore in FY25. PAT hit ₹11 crore, up 343% YoY. Operating profit swelled to ₹27 crore from ₹7 crore. The market pays 62.4x earnings on a stock that trades near ₹310, versus a peer median of 38.5x.

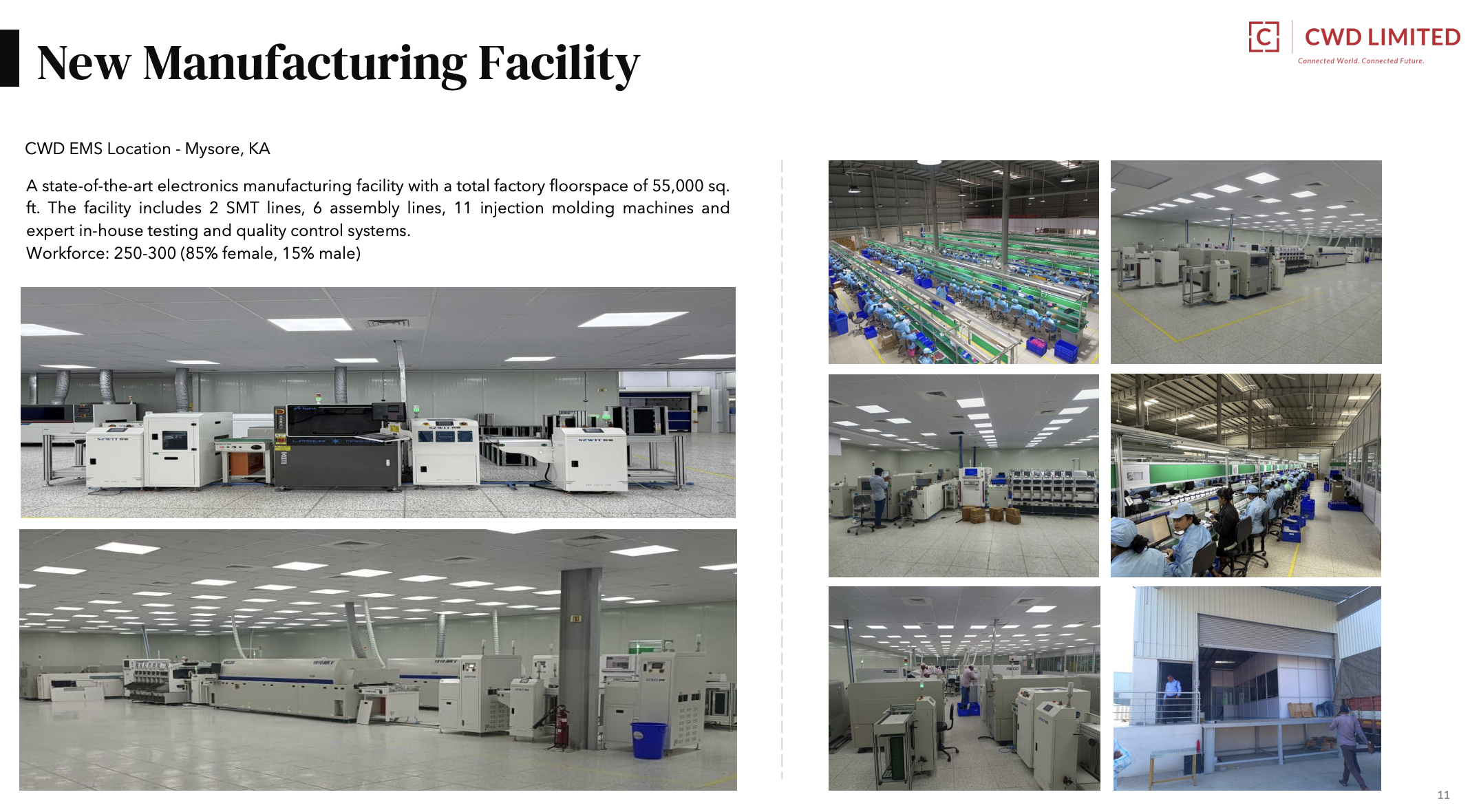

What’s paying for the rally: The company is running off an executable order book of ₹172 crore and expanded manufacturing footprint from 15,000 sq. ft. to 55,000 sq. ft.—a 3.7x jump. Soundbox daily production capacity climbed from 5,000 to 15,000 units.

But here’s the tension. Margins compressed: Operating profit margin dropped to 18.2% from 21.7% in FY25. Net margin stayed thin at 7.6%. Cash generation turned negative—the company burned ₹48 crore from operating activity in FY26 versus a ₹3 crore inflow in FY25. Working capital is the villain: inventory days jumped to 189 from 566 (improvement masked by raw absolute growth in stock), but receivables days compressed to 88 from 190.

The company targets ₹380–400 crore in FY27 revenue. Does capacity and order flow actually deliver that, or is this another subcontinental hardware startup betting on manufacturing excellence in a land where supply chains still surprise you?

2. Introduction

CWD stands for Connected Wireless Devices. Incorporated in 2016, the company designs, develops, manufactures, and sells integrated solutions combining software and electronics. All products center on wireless technologies: short-range (NFC, Bluetooth BLE, WiFi, Zigbee), mid-range (LoRa), and long-range (5G LTE, NB-IoT, LTE Cat-M1).

The company operates two main segments: Consumer Electronics (smart, connected devices) and Technology Solutions (customized wireless communication platforms for enterprise). Its manufacturing facility sits in Mysore, Karnataka. A subsidiary, CWD Innovation HK Limited, is 100% owned and located in Hong Kong.

Recent moves: In January 2026, the company issued a 4:1 bonus (four new shares for every one existing share), expanding equity share count. In May 2026, the board approved FY26 audited results and allotted 38,513 shares from warrant conversion plus 154,052 bonus shares. This increased paid-up capital from ₹22.21 crore to ₹22.40 crore at par value of ₹10.

The executive duo—Tejas Kothari (Joint MD, CFO) and Siddhartha Xavier (Joint MD)—co-founded the company and hold board seats. Kothari has 25+ years in finance and management; Xavier was the former Head of Technology at Reliance Communications’ Device Group.

3. Business Model: WTF Do They Even Do?

Three revenue buckets dominate the narrative.

Fintech (Sound Boxes & Ad Platform): CWD is the chosen design manufacturer for PhonePe’s sound boxes. It also supplies to Sriram Finance, PayNearBy, AirPay, and Bajaj Finance. The product is a UPI-enabled sound box that announces transaction confirmations via audio, reducing manual reconciliation and merchant error. The company launched an industry-first ad platform layered on top, shifting toward a recurring SaaS revenue model. AI modules are in development for merchant churn management, device stability, and anomaly detection.

FY26 soundbox capacity expanded to 15,000 units/day from 5,000. The company targets 2.5 lakh units/month by end of FY27. An ₹76 crore order from a fintech firm (announced Aug 2025) and a ₹45 crore order (announced Mar 2025) anchor visibility.

Smart Metering (NIC—Network Interface Card): CWD is the chosen design manufacturer for CyanConnode, India’s leading Smart Meter Communication Systems provider. Smart meter installations in India reached ~35 million by FY25 against a rollout target of 250 million. The government’s push via the Revamped Distribution Sector Scheme (RDSS) and private utility deployments are driving demand. An ₹53 crore order from CyanConnode (announced Jul 2025) adds 6+ months of visibility.

The smart metering market is forecast at USD 308 billion by 2032E (CAGR 21% from 2024E).

Bespoke IoT & Agri-Tech: The company supplies livestock health monitoring (farm cattle tracking, rumination alerts), agri-tech soil sensors with cloud-based dashboards, and industrial IoT solutions. A 25,000-unit Wireless Mesh Sensor (WMS) order with commitment for 15,000 additional units strengthens the agri-tech foothold.

The global IoT device count is forecast to triple from 9.7 billion (2020) to 29 billion (2030). Consumer IoT is expected to drive ~60% of that demand.

The Cost Structure & Roast. CWD manufactures in-house at Mysore—15,200 sq. ft. expanded to 55,000 sq. ft. (2 SMT lines, 6 assembly lines, 11 injection molding machines, 250–300 staff expected to grow to 500). Raw material cost consumed 81.6% of revenue in FY26 (₹120 cr of ₹147 cr sales). Employee cost sat at ₹3.26 crore (2.2% of revenue), a micro figure for a ₹147 crore company. The company is pursuing direct OEM sourcing to reduce material costs—i.e., it’s buying cheaper semiconductors, not renegotiating supplier terms.

Operating profit margin fell from 21.7% (FY25) to 18.2% (FY26) despite a 346% revenue jump. That’s the inflation tax on growth: the business is drowning in raw material cost, not staffing inefficiency.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Metric

FY26

FY25

YoY Change

Revenue

147

33

346%

EBITDA

28

7

251%

PAT

11

3

343%

EPS (₹)

5.01

1.32

280%

Revenue growth was driven by soundbox orders (PhonePe scaling, others), smart metering (CyanConnode ramp), and IoT (WMS and agri-tech pilots). EBITDA margin was 19.3% in FY26 vs. 20.7% in FY25—tiny compression, but the business isn’t expanding profit pool as fast as top-line. PAT margin held at 7.6% (FY26) vs. 7.6% (FY25)—flat, which is unusual given the operating leverage should kick in.