Bosch Ltd FY26: The ₹1,410 Crore Smoke Signal and the 45x P/E Conundrum

Section 1 — At a Glance

Bosch Ltd closed the financial year 2026 with a headline revenue from operations of ₹20,034.7 crore, marking a 10.8% expansion over the previous fiscal. While top-line momentum reflects resilient underlying volume pull across domestic automotive segments, investor focus remains intensely concentrated on the structural quality of earnings. Reported profit after tax climbed to ₹2,773.2 crore, appearing at first glance as a spectacular 37.6% surge. However, a forensic unbundling of the profit and loss statement reveals that this bottom-line expansion was heavily subsidised by an exceptional non-operating driver—specifically, the strategic divestment of the Video Solutions, Access, and Intrusion Communication lines under the Building Technologies umbrella.

Excluding this transactional windfall, organic operating profit expansion moved at a far more measured pace. Operating profit margins compressed relative to the historical high-water marks of the prior decade, pinned down by elevated raw material consumption costs that absorbed ₹12,887.2 crore, or roughly 64.3% of top-line revenue. Concurrently, the stock continues to command an aggressive premium, trading at a price-to-earnings multiple of 45.0x against a backdrop of single-digit multi-year volume trends in traditional core segments. While an immaculate, virtually debt-free balance sheet and a formidable domestic market share provide immense structural comfort, the divergence between headline accounting growth and core manufacturing yields remains a critical point of long-term evaluation.

Operational leverage is a double-edged sword that cuts deepest when commodity inflation forces a business to run faster just to stand still.

With structural regulatory transitions looming across the domestic landscape, the market is aggressively pricing in future content-per-vehicle step-ups. The narrative for the upcoming year is no longer about steady replacement demand, but about how quickly advanced electronic architectures can scale.

Section 2 — Introduction

Bosch Ltd represents the undisputed blue-chip anchor of Indian automotive component engineering, operating as a 70.54% owned subsidiary of the global Robert Bosch enterprise. The corporate architecture spans mobility solutions, industrial technology, consumer goods, and energy building portfolios. For decades, the entity has functioned as an effective tax on Indian vehicle production; if a wheel turns on an Indian highway, chances are high that a Bosch-engineered fuel injection pump, electronic control unit, or exhaust sensor is dictating its rhythm.

Yet, the modern automotive landscape is undergoing an existential transformation. The company finds itself navigating a delicate straddle: defending its highly lucrative, deeply entrenched internal combustion engine (ICE) business while simultaneously deploying capital to secure incumbency in the emerging electric vehicle (EV) ecosystem. Management’s operational posture has shifted toward a framework of “cautious optimism”. This restraint is well-founded, given that the business is structurally exposed to volatile global logistics channels, sensitive currency fluctuations, and localized commodity cycles that refuse to cooperate with quarterly corporate budgeting schedules.

Section 3 — Business Model: WTF Do They Even Do?

To the casual observer, Bosch is the company that makes the power drill sitting in their garage or the spark plug inside their car. To the institutional analyst, Bosch is a sprawling industrial tollbooth that monetizes regulatory mandates.

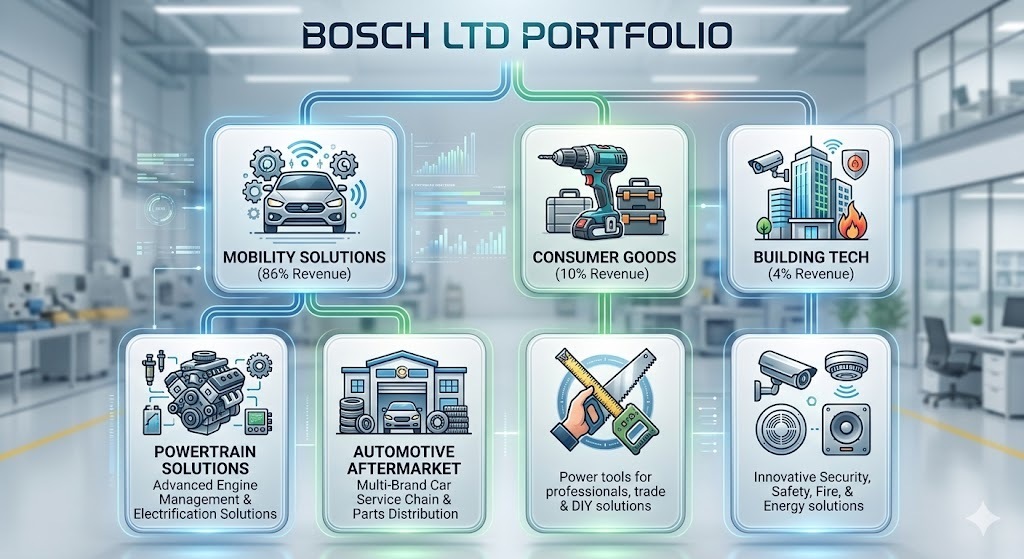

The business model derives 86% of its top-line juice from the Mobility segment. Within this block, Powertrain Solutions manufactures complex engine management systems for diesel, gasoline, and alternate fuel vehicles. When the Government of India decides to tighten emission norms, Bosch does not sweat; it simply recalibrates its product line, inserts more sensors per engine tailpipe, and bills the original equipment manufacturers (OEMs) for the privilege.

The remaining revenue is split between Consumer Goods at 10%—mostly power tools looking for a home in professional industrial clusters—and Building Technologies at a tiny 4%. Structurally, the company is moving away from being a pure manufacturing engine to a wholesale trading and technical services provider. Today, pure manufacturing accounts for 44% of revenue, while wholesale and retail trading combine for a massive 53%. In short, a significant portion of the business involves importing the sophisticated global IP of its German parent and selling it to Indian manufacturers who cannot build it themselves.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Latest Quarter (Mar ’26)

YoY (%)

QoQ (%)

Revenue

5,565.7

31.5%

13.9%

EBITDA / Operating Profit

781.6

40.3%

27.6%

PAT

570.0

1.1%

7.0%

EPS (₹)

193.26

1.1%

7.0%

The final quarter of the financial year delivered an impressive ₹5,565.7 crore top-line performance, expanding by 31.5% over the matching prior period. Operating profit followed suit, surging 40.3% to ₹781.6 crore as fixed costs found