Banswara Syntex Mar 2026 : A ₹475 Crore Debt Load and a 12.2% Margin Turnaround

Section 1 — At a Glance

Banswara Syntex Limited exited the financial year ending March 31, 2026, on a structurally transformed note, navigating complex domestic and global structural imbalances. Headline revenue from operations touched ₹1,356.28 crore for FY26, showing a moderate growth curve compared to ₹1,292.53 crore in FY25. The real operating push was visible in the company’s EBITDA, which climbed to ₹143.60 crore in FY26 from ₹117.20 crore in the preceding year, driving EBITDA margins up to 10.5%. Net profit for the full year reached ₹31.20 crore, rebounding from a suppressed base of ₹22.16 crore in FY25, despite absorbing a ₹8.90 crore exceptional charge linked to evolving national labor welfare rules.

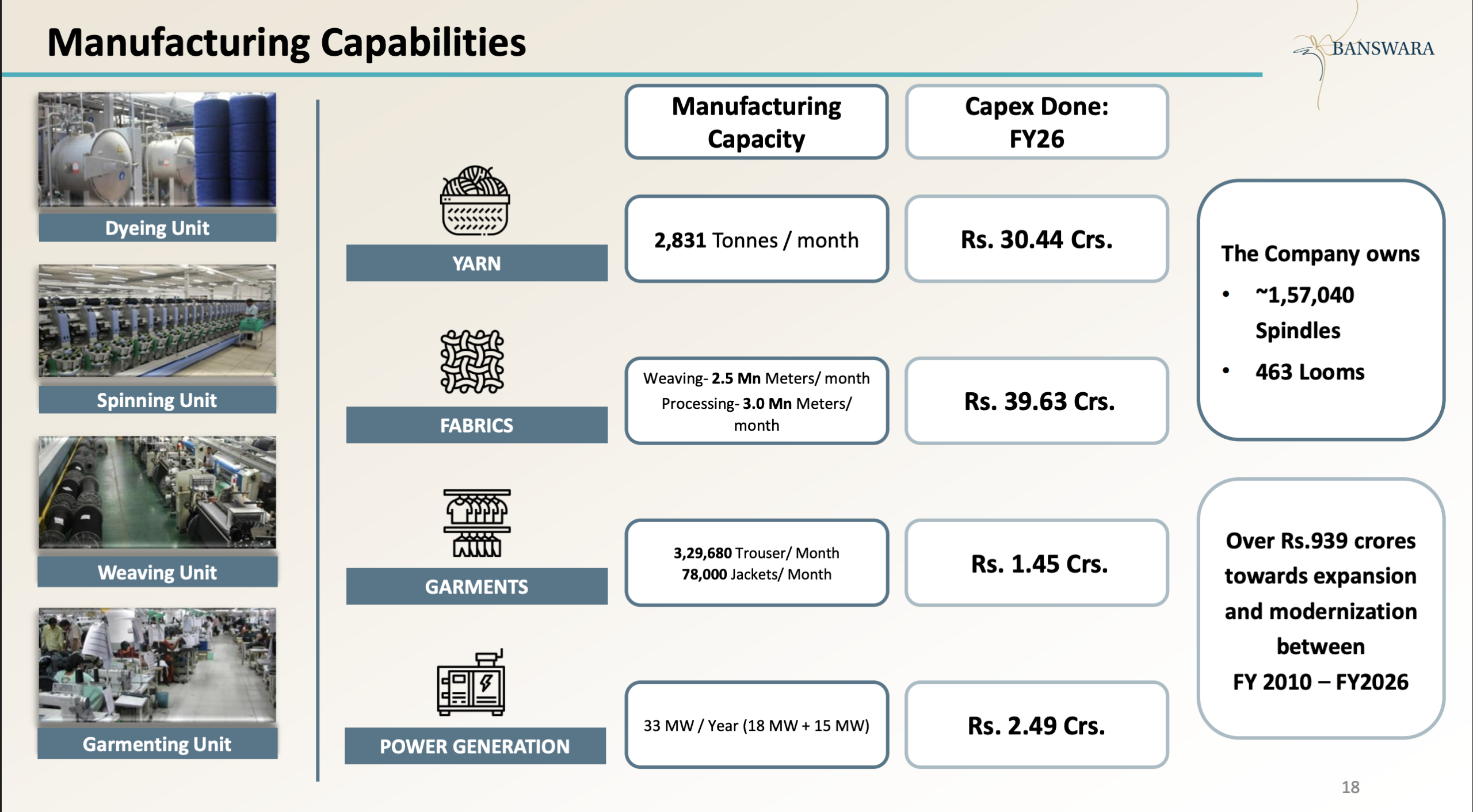

The structural transformation is led primarily by the garmenting vertical, where full-year capacity utilization expanded to 72% from a historic low of 46% in FY25. This operational momentum generated ₹324.00 crore in annual garment revenues, backed by a strong final quarter performance of ₹96.00 crore. However, the core yarn manufacturing division continues to act as a significant drag, hobbled by chronic regional labor availability deficits that dragged down yarn capacity utilization to 77% for the year.

What remains a key monitorable for the public markets is the capital structure. Total balance sheet borrowings stood at ₹474.99 crore by the close of March 2026, keeping the debt-to-equity ratio pinned at 0.81. Capital asset creation over cycles cannot be treated as isolated engineering achievements if the financing behind them continuously outpaces free cash generation. While the asset-heavy modernization capex cycle is approaching completion, capital allocation efficiency will now depend on management’s ability to extract premium pricing fields across the US and European export territories.

Section 2 — Introduction

Banswara Syntex Limited is an established, legacy synthetic textile manufacturer headquartered in Rajasthan. Over its decades-long corporate evolution, the enterprise has repositioned itself from a localized commodities producer into a highly coordinated, vertically integrated player spanning the fiber-to-clothing value chain. The company operates advanced spinning, weaving, chemical processing, and ready-made apparel lines across production blocks in Banswara, Surat, and Daman.

The fundamental rationale for assessing the enterprise at this juncture centers on its major multi-year modernization and debottlenecking capex cycle. Between FY10 and December 2025, the company deployed over ₹917.00 crore into internal upgrades. This asset creation process has left a heavy mark on the corporate balance sheet, elevating overall liabilities and drawing closer inspection from credit rating agencies due to structural leverage parameters. With international sourcing dynamics shifting through structural adjustments like the India-UK Free Trade Agreement and global procurement diversification, the company’s ability to convert raw gross block expansion into real corporate cash flows is a critical trendline.

Section 3 — Business Model: WTF Do They Even Do?

To the smart but lazy observer, Banswara Syntex is a factory ecosystem that takes synthetic and blended fibers at one end and spits out formal suits for premium global high-street brands at the other. It acts as a full-service, vertically integrated industrial package. The core operations are split across three key production layers:

Yarn Processing: Producing polyester, viscose, acrylic, and premium wool-blended specialty counts across 151,360 spindles.

Ready-Made Apparel: Turning internal fabrics into formal trousers and structured jackets, commanding a dominant 70% domestic market share in highly specialized corporate formal suit contracts inside India.

The underlying economic thesis relies on capturing margin chunks at every stage of production. By consuming its own internal yarn within its fabric mills, and feeding internal fabrics straight into its apparel plants, Banswara attempts to bypass open-market margin leakage. To keep this massive industrial machine from stalling, the company also runs a 33-megawatt captive thermal power setup to satisfy its intensive multi-location base energy requirements.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Mar 2026

YoY (%)

QoQ (%)

Revenue

365.65

7.52%

7.56%

EBITDA / Operating Profit

43.06

98.71%

13.92%

PAT

11.49

35.49%

-17.93%

EPS (₹)

3.36

35.48%

-17.85%

Did Management Walk the Talk?

During previous analytical cycles, management emphasized that the second half of the fiscal year would demonstrate structural margin improvements as value-added