Bajel Projects (FY26): The 74% PAT Jump Hides a 214-Day Debtor Problem

General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

1. At a Glance

Bajel Projects reported FY26 profit after tax up 74% to ₹27 crore on revenue of ₹2,792 crore (+7% YoY).

The headline sounds muscular—but dig into the balance sheet and a tension emerges. Debtors ballooned from ₹971 crore to ₹1,634 crore (a ₹663 crore swing in one year), pushing debtor days to 214. The company claims this spike is mostly timing and collection already happened post-March. Management also had to account for a one-time labor code provision that knocked PAT reported below ₹8 crore before exceptional items.

EBITDA did expand 38% to ₹125 crore and margins moved north to 4.4% from 3.4%, which is genuine. But ask this: does a working capital stretch that deep tell a story about execution rhythm, customer payment discipline, or just the cost of chasing scale in power EPC?

The order book sits at ₹3,442 crore—about 1.2x annual revenue and solid—with major wins from MSETCL, PGCIL, and a first ₹400+ crore MENA order post-March. Return on average capital employed rose to 15.8%. Debt ticked up to ₹367 crore (₹140 crore was bill discounting), but net cash borrowings fell to ₹31 crore.

The teaser: A company pivoting toward quality-led growth, doubling down on execution, but asking whether ₹3,000 crore in net cash minus ₹1,634 crore in receivables is a strength or a sign the working capital machine needs tuning.

2. Introduction

Bajel Projects Limited—carved out from Bajaj Electricals in September 2023 and listed separately in December 2023—is now the standalone power transmission & distribution EPC arm of the Bajaj Group. It’s a relatively young public entity, but the underlying business spans 25+ years of transmission line, substation, and monopole work.

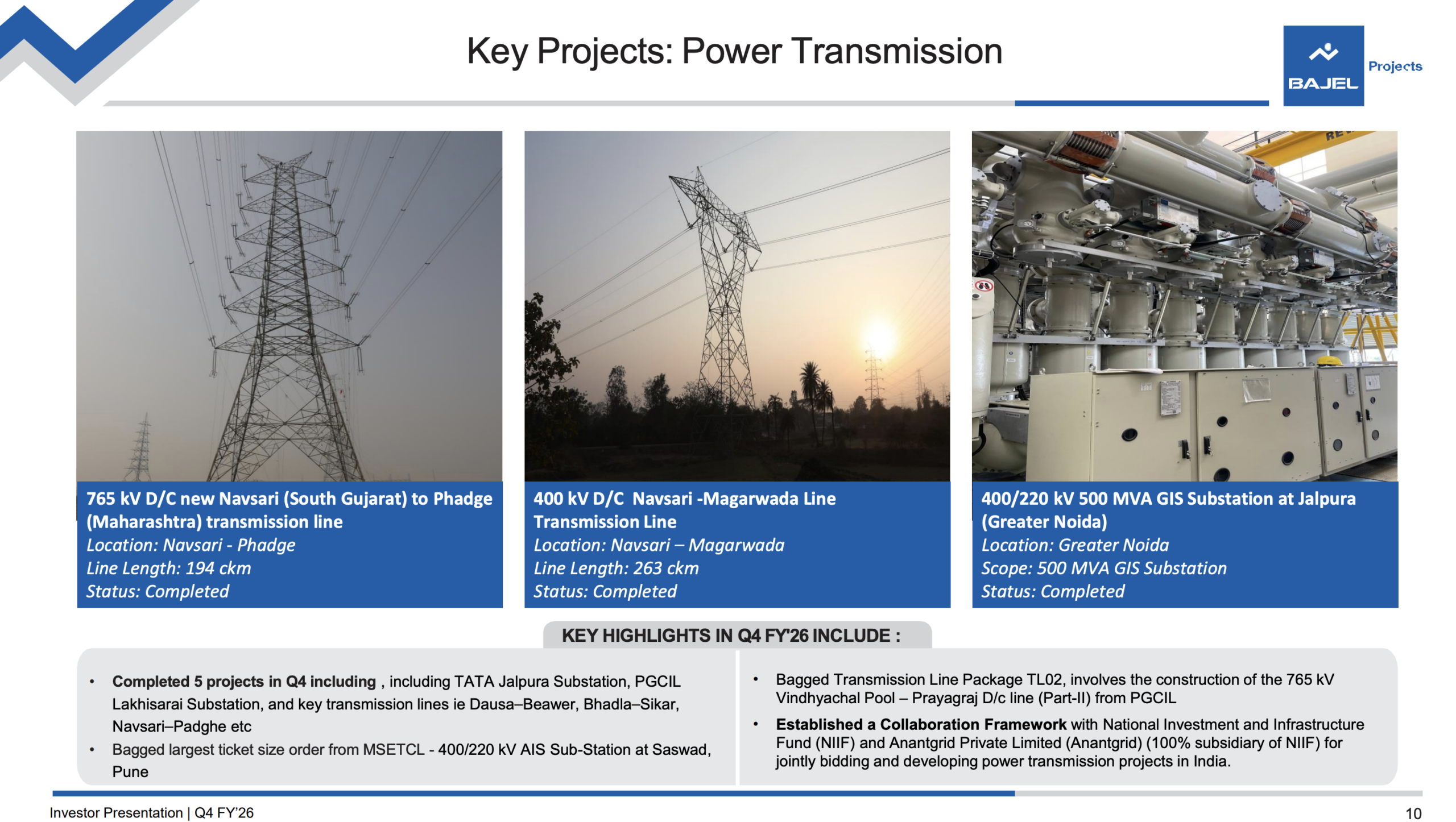

The company operates in an industry riding structural tailwinds. India’s power transmission roadmap targets ₹9 lakh crore of capex through 2032, with renewable integration and inter-state transfer corridors driving demand. Bajel claims it executed ~10% of India’s total transmission line capacity addition in FY26 (1,168 ckm out of 12,139 ckm nationally).

FY26 marked a post-demerger inflection point. Management articulated a deliberate shift from “scale-led growth to quality-led growth”—tighter project selection, disciplined bidding, stronger contractual terms. They launched RAASTA 2030, a six-year roadmap aiming for double-digit revenue growth, high single-digit EBITDA margins, and 15%+ return on capital employed by FY28–30.

The last 12 months saw major order wins (MSETCL ₹700+ crore, Vindhyachal PGCIL, Mandsaur PGCIL), a 50:50 joint venture in Saudi Arabia with Al Sharif, a collaboration framework with NIIF and AnantGrid for project co-development, and announcement of a ₹170 crore capex to expand manufacturing capacity at Ranjangaon from 45k MTPA to 110–120k MTPA.

3. Business Model: WTF Do They Even Do?

Bajel does four things: transmission EPC, distribution EPC, international EPC, and manufacturing.

Power Transmission (93% of order book). The company executes turnkey projects—design, engineering, procurement, manufacturing, installation, commissioning—for 132 kV, 220 kV, 400 kV, and 765 kV transmission lines in single-circuit, double-circuit, and multi-circuit configurations. It also designs and builds EHV AIS/GIS substations. In FY26, it completed 17 projects, commissioned 1,168 ckm across lines and substations, and has standing qualifications for 765 kV work.

The moat, if it exists, is narrow. Competition is intense (low entry barriers, says the credit rating agency), but Bajel’s advantage is execution track record and customer relationships with Power Grid Corporation (the dominant buyer, 40%+ of order book), state distribution utilities, and renewable developers building evacuation corridors.

Power Distribution (7% of order book). This is retrofits: upgrading the last mile. Construction of 33/11 kV substations, 11 kV and 33 kV overhead lines, underground cabling, compact substations, service connections. The company claims 50,000+ villages electrified (mostly under government schemes like Saubhagya) and 26 lakh+ connection points. This is a lower-margin, longer-execution business; it’s where government schemes live and where Bajel has fewer counterparty risks but tighter pricing.

International EPC (0.2% of order book, ~1–2 projects in flight). Kenya, Togo, Zambia (mostly supply). Post-March FY26, Bajel secured its first ₹400+ crore MENA order for a 500 kV overhead line. The Saudi JV (Al Sharif, 50:50) is the platform.

Manufacturing. The Ranjangaon plant (55 km from Pune) makes lattice towers, monopoles, high masts, lighting poles, and operates a galvanizing unit. Current capacity is ~45k MTPA, split across product lines. FY26 production hit 56.5k MTPA (exceeding nominal capacity—debottlenecking, management says). The capex to expand to 110–120k MTPA is underway; the galvanizing bath (the bottleneck) will be ready by August, but full monopole line capacity (6,000 MT/month vs current ~2,000 MT/month) won’t be online until end-FY27 or early-FY28.

What’s the competitive pressure? Commodity cost volatility (aluminum, zinc, steel). Execution labor shortages (skilled workers in foundation, erection, stringing). FX depreciation adding cost. And the inherent dynamics of EPC: low margins when bid competition rises, working capital intensity, and customer payment delays.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Q4 FY26

Q4 FY25

FY26

FY25

Revenue

1,008

801

2,792

2,598

EBITDA

38

27

125

90

EBITDA Margin %

3.7

3.4

4.4

3.4

PAT

14

5

27

15

EPS (₹)

1.22

0.42

2.33

1.34

Quarterly commentary. Q4 FY26 was the standout quarter—revenue crossed ₹1,000 crore for the first time. EBITDA of ₹38 crore (+39% YoY) and PAT of ₹14 crore (+193% over Q4 FY25’s ₹5 crore) arrived on the back of project completions (17 for the year) and higher billing. The fourth quarter accounted for 36% of annual revenue.

Annual performance. FY26 revenue of ₹2,792 crore grew 7% YoY (slower than prior-year 120% growth from FY24’s ₹1,194 crore, but management attributed the moderation to disciplined order selection and “capacity and bandwidth” constraints, not demand weakness). EBITDA grew 38% to ₹125 crore; the 100 bps margin improvement (3.4% to 4.4%) reflects operational leverage and better project mix. Exceptional items (₹8 crore, one-time labor code provision) reduced reported PAT to ₹27 crore, but pre-exceptional PBT was ₹42 crore (+73% YoY).

Working capital sting. Operating cash flow in FY26 was only ₹21 crore, down 70% from ₹69 crore in FY25. Free cash flow turned negative at -₹13 crore (vs +₹35 crore in FY25). The culprit: trade receivables surged ₹663 crore year-on-year to ₹1,634 crore. Management disclosed that a “marquee customer” held back ~₹225 crore in the last fortnight of March, and higher Q4 billing (~₹194 crore) was not cleared until early FY27. Retentions (contractual holdbacks as projects near completion) added ~₹100 crore. So the narrative is: timing + one large customer + retention increases due to project progress, not structural elongation. But the cash wasn’t there at March 31.

5. Valuation Discussion: Fair Value Range (Educational Only)

What follows is a walkthrough of how three valuation methods work, using this company’s numbers as the example — not a target, not a forecast, not advice.

Method 1: P/E Multiple. Annualized EPS for FY26 (full year) is ₹2.33 (before exceptional items, normalized). The peer band for heavy electrical equipment EPC players (Hitachi Energy, ABB, CG Power, BHEL, Siemens, GE Vernova, etc.) trades at P/E multiples ranging from 55x to 159x. Bajel itself, at CMP ₹201 (as of June 5, 2026), implies a P/E of 93.75x on FY26 EPS of ₹2.14 (inclusive of exceptional items). Using the peer band of 55–100x on FY26 normalized EPS of ₹2.33 produces a range of ₹128–233.

Method 2: EV/EBITDA Multiple. FY26 EBITDA was ₹125 crore; enterprise value at CMP ₹201 and net debt of ~₹184 crore (gross debt ₹367 cr minus cash ₹183 cr) is approximately ₹2,504 crore. Implied EV/EBITDA is 20x. The peer band