Arvind Ltd FY26: A Silk-Smooth Topline Meets an Advanced Material Twist

Section 1 — At a Glance

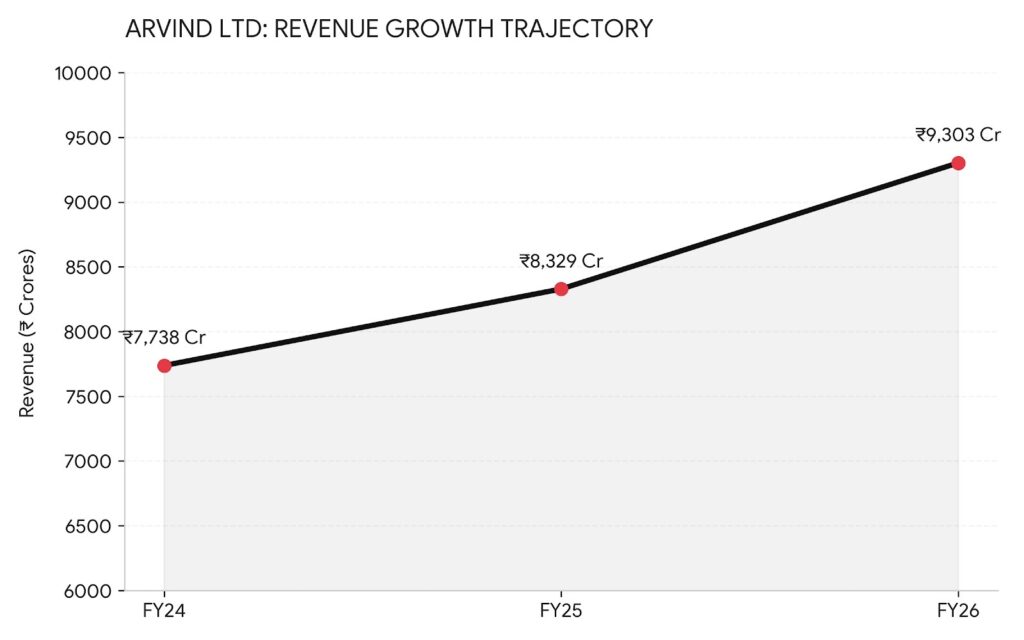

Arvind Ltd has completed its fiscal year 2026 with an all-time high consolidated revenue from operations of ₹9,303 crore, matching a strong 12% top-line expansion against the prior fiscal year. While the traditional denim, wovens, and garmenting legacy continues to form the spine of the company’s manufacturing footprint, the investor spotlight has decisively swerved toward the high-margin, high-growth Advanced Materials Division (AMD). AMD rebounded with an impressive 19% yearly growth, pocketing ₹1,839 crore in operations.

What is keeping the bulls charged is a consistent margin expansion and deleveraging discipline. Consolidated EBITDA for the full year jumped 15% to ₹1,061 crore, pushing operational margins up by 37 basis points to 11.4%. Profit after tax (before exceptional items) scaled to ₹444 crore, marking a solid 21% jump. Simultaneously, better free cash flow generation allowed the company to trim its domestic net debt by ₹112 crore, leaving closing net debt at ₹1,172 crore as of March 31, 2026.

However, beneath the smooth fabric of these headline numbers lie structural friction points that keeping analysts watchful. Operating cash flows, while healthy at ₹867 crore, are increasingly being drawn down by capital expenditure requirements. Margin expansion faced tariff headwinds, and a one-time provision of ₹23.5 crore (net of tax) was absorbed due to the implementation of the new Labour Code. Furthermore, a mega-acquisition in the United States closed in May 2026 is set to completely alter the leverage profile, spiking consolidated debt back up to the ₹3,000 crore mark.

Operational efficiency acts as a reliable shield during cyclical downturns, but aggressive cross-border capital allocation tests a balance sheet’s true endurance.

Can Arvind leverage its global technical textile play without loosening its hard-won operational discipline? Let us dissect the threads.

Section 2 — Introduction

Arvind Ltd is an institutional titan of the Indian textile landscape with an operational history spanning nearly eight decades. Famously recognized as one of the largest vertically integrated denim and woven fabric manufacturers on the planet, the company has transformed itself from a traditional textile mill into a sophisticated manufacturing conglomerate. Its processing capabilities stretch from cotton yarn up to fully structured retail garments, providing a massive cushion of structural flexibility.

The rationale for tracking Arvind right now goes far beyond standard apparel cycles. In May 2026, the company made a definitive geopolitical move by executing a majority stake acquisition in US-based Dalco-GFT LLC via its wholly-owned subsidiary, Arvind Advanced Materials Limited (AAML). This provides the company with immediate, deep-moat entry into the highly lucrative US technical textiles and automotive supply chain. With new leadership taking the reins of the core textile division, Arvind is aggressively attempting to shed its slow-growth commodity tag for a high-value technical avatar.

Section 3 — Business Model: WTF Do They Even Do?

To the uninitiated, Arvind just makes your favorite pair of blue jeans. In reality, the company operates a multi-layered manufacturing engine bifurcated into two distinct universes: traditional Textiles and Advanced Materials (AMD).

The Textiles segment is the old-school breadwinner, driving 84% of total group revenues. It processes cotton and synthetic inputs into Denims, Wovens, and fully processed Garments. Woven fabrics hold the lion’s share at 46% of the fabric mix, followed by Garments at 27% and core Denim at 18.5%. It is a high-volume game, pushing out 135.8 million meters of woven fabrics and 51.6 million meters of denim annually.

The real margin engine, however, is the Advanced Materials Division (AMD), making up 12% of sales. This segment produces highly engineered technical textiles used in extreme environments: fire-retardant corporate workwear, heavy-duty industrial filtration systems, automotive composites, and structural reinforcement fabrics. Over half of AMD’s sales come from human protection gear, providing a high-barrier business model where buyers “spec-in” products directly into long-term programs.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Results Comparison

Metric

Latest Quarter (Mar 2026)

YoY (Mar 2025)

QoQ (Dec 2025)

Revenue

2,553.09

2,220.69

2,372.64

EBITDA / Operating Profit

306.21

244.57

272.58

PAT

159.71

151.04

97.59

EPS

6.09

5.77

3.72

The quarterly trajectory illustrates an absolute powerhouse finish to the year. Q4 revenue jumped 15% year-on-year, driven by a blistering performance in the Advanced Materials segment, which posted its best-ever quarterly revenue of ₹546 crore. Margins in the AMD segment crossed a striking 17.3% during the quarter, aided by a reversal of earlier expense provisions and strong defense order executions. On the traditional side, the garmenting division recorded its third consecutive quarter of shipping over 10 million pieces, showcasing robust global volume stickiness.

Short-term earnings acceleration often reflects seasonal or non-recurring tailwinds; look for multi-quarter consistency before treating a margin spike as structural reality.

Did Management Walk the Talk?

Reviewing guidance from previous cycles shows that management has successfully hit its operational targets for FY26. The team had consistently promised a recovery in the AMD business to an 18–20% growth band following historical slowdowns, and they delivered right