General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

1. At a Glance

Revenue grew 17% to ₹190.6 Cr in FY26 against significant losses: net loss narrowed to ₹121.9 Cr from ₹140.4 Cr in FY25. The three-legged stool — Senior Living Residences, Assisted Care Services, and AGEasy — all expanded volume; none yet holds steady margins. Noida Phase 1 obtained a partial occupancy certificate in May 2026, unlocking ~₹150 Cr in receivables. Debt sits at ₹96.8 Cr on a ₹408 Cr net worth; cash position stands at ₹77.1 Cr, offering ~4–6 months of runway without fresh capital.

The tension: aggressive property launches without EBITDA cover, wage inflation squeezing care homes, and the need for a profitability inflection by mid-FY27 to avoid shareholder dilution.

Management signalled losses narrow further in FY27, with one or two verticals approaching breakeven “by later part” of the year — a softly-stated commitment.

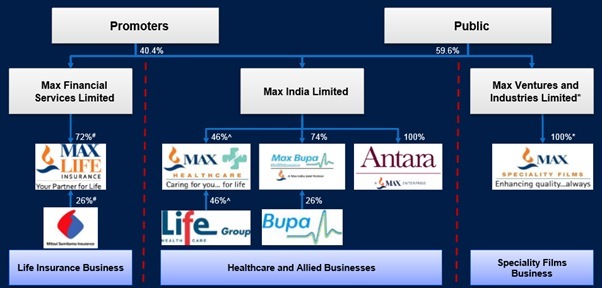

2. Introduction

Max India is a holding company anchored in the Antara senior care brand, owned by Max Group. The company operates across three domains: senior living residences in Gurgaon and Noida; assisted care services spanning care homes and at-home nursing; and AGEasy, a D2C and marketplace platform for senior wellness products.

Incorporated in 2019 and listed in 2022, Max India arrived during the pandemic boom in senior care. The thesis was simple: India’s demographic shift toward an aging population would create secular tailwinds across residential facilities, care services, and product distribution. For three-and-a-half years, the company has delivered on volume — units sold, beds opened, revenue more than doubled — but profitability remains absent.

The May 2026 earnings call contained no admission of error, only recalibration: cost overruns at Noida forced a write-up of project capex; wage inflation triggered by the Labour Code compliance dented margins across care homes; and the ambitious 1.5 million sq ft per annum development target landed at 1.1 million sq ft due to regulatory delays (Chandigarh lost height clearance after “Operations Sindoor,” a local property crackdown).

In June 2026, management granted 8.74 lakh ESOPs and allotted 60,000 shares — a signal that equity dilution lies ahead.

3. Business Model: WTF Do They Even Do?

Senior Living Residences: The Jewel and the Anchor.

Max Estates Gurgaum Limited (MEGL) and subsidiary Max Estates Gurgaum 2 Limited develop intergenerational senior living towers — apartment communities where both seniors and multi-generational families live. The Antara Senior Living brand manages operations, services, and resale. Revenue comes in two forms: upfront development fees (management fees earned during construction and sales) and post-occupancy annuities (community amenities, healthcare, housekeeping).

Estate 360 (Gurgaum, first phase): all 292 units sold; ITD (inception to date) sales collection ₹534 Cr at 87% efficiency. Antara has earned ₹45.6 Cr in management fees, of which ₹26 Cr accrued in FY26. At maturity, the community will generate ~₹10–12 Cr annual annuity.

Estate 361 (Gurgaum, Phase 2): launched Dec 2025 with 180 units; 127 sold, ₹69 Cr collected by Mar 2026. Management guidance: ~₹200 Cr lifetime management fee, price-dependent. Phase 2 launching “around the corner… in the next few days.”

Antara Noida (Phase 1): partial occupancy certificate received May 2026; 340 units ready for possession. ~₹150 Cr in receivables sit in the SPV pending collection. Phase 2, at 2–3x the original price points, holds ~220 units and 0.44 million sq ft of embedded upside. The path to Phase 2 approvals: complete possession obligations → seek authority “recertification of revised building plans” → reapproval. Management: “Hopefully, by the end of this year [FY27].”

Antara Dehradun: the only operational community (14 acres). Q4 operations revenue ₹6.7 Cr; FY26 full-year ₹24.2 Cr with ₹2.3 Cr profit. Fully occupied; growth “more linear.” Cash positive, profitable — a proof-of-concept that the model works at scale. Five resales in FY26 generated ₹1.71 Cr in marketing fees.

The model is fee-heavy and illiquid: cash emerges slowly from construction-linked collections and then from operations annuities; total invested capital in residences ~₹490 Cr against ₹45 Cr surplus.

Assisted Care Services: The Ramp, The Headwind.

Antara operates 485 beds across 8 care homes in NCR, Bengaluru, and Chennai — memory care, assisted living, and transitional services. The services vertical also includes care-at-home (nursing, physiotherapy, at-home clinical support), now being integrated into care homes to extract cost synergies.

FY26 revenue ₹38.8 Cr (up 60% YoY); Q4 net revenue ₹11.4 Cr. Patients served since inception: ~50,000; in Q4 alone, ~3,400. Occupancy: 27% average (bed-days basis), with wide variance by facility — Sector 41 Gurgaum at 34%, Noida at 38%, Bannerghatta Bengaluru at 37%.

The ramp is real: like-for-like occupancy (excluding new beds) rose 10% QoQ at mature sites. Unit economics are inflecting: contribution margin (revenue less variable cost) turned positive at several sites in Q4.

The headwind: most beds were added in the last quarter of FY26, depressing average occupancy. Labour Code compliance — gratuity provisioning and wage escalation — will add ₹3–4 Cr to the cost base in FY27. Management targets consolidated care homes EBITDA breakeven “in H1 of FY28,” assuming most beds have aged 8–10 quarters by then and reached 65–70% occupancy.

Invested capital ~₹484 Cr; the business has never posted a positive operating profit in full year.

AGEasy: The Dark Horse.

AGEasy is a D2C and marketplace platform for senior wellness products — commode frames, walking aids, fall-prevention gear, gut health supplements, lung health products — 91 live products across 159 SKUs. Distribution: Amazon, Flipkart, Swiggy, and the AGEasy.com D2C site.

FY26 revenue ₹76.8 Cr (up 100% YoY); Q4 ₹23 Cr. Lives touched: 7+ lakhs; repeat customers 78,000+; NPS 45. Return on Ad Spend (RoAS) improved from 1.2 to 1.8 overall in FY26, with D2C RoAS exiting at 1.7–1.8 and marketplaces at 2.2. Gross margins jumped to 40% in Q4 from 28% in Q1 — a 40% improvement.

Management’s April 2026 exit metrics: RoAS 2.9, gross margin 47%. Profitability track: EBITDA breakeven guided for Q4 FY27.

The moat, per management: 3 patents granted, 3 filed. Differentiation claims focus on senior-specific design, efficacy data, and community features. Sourcing: 70% domestic, 30% imports (mostly China), exposed to geopolitical logistics risk but mitigated via forward-buying and alternative vendors.

4. Financials Overview

Figures are consolidated, in ₹ crore, quarterly results basis.

Metric

FY26 Q4

FY26 Q3

QoQ Change

FY26 Full Year

FY25 Full Year

YoY Change

Revenue

72.0

49.8

+45%

213.4

164.2

+30%

EBITDA

(6.8)

(27.8)

+1.6x

(83.1)

(99.5)

+16%

PAT

(19.3)

(42.9)

+55%

(121.9)

(140.4)

+13%

EPS (₹)

(3.68)

(8.17)

+55%

(23.2)

(26.7)

+13%

Revenue acceleration is real: Q4 jumped 45% sequentially and 58% year-over-year. Residences (senior living project collections + Dehradun ops) contributed ₹37.9 Cr in Q4 (up 1.9x QoQ). Assisted Care Services ₹32.7 Cr (technically consolidated, but net revenue reported as ₹11.4 Cr after eliminations). AGEasy ₹23 Cr (up 1.4x YoY).

EBITDA loss narrowed significantly: Q4 loss of ₹6.8 Cr versus ₹27.8 Cr in Q3 — a 75% improvement. For the full year, operating losses fell ₹16 Cr (16% improvement). Management cited cost optimization and “efficient treasury management.”

Net profit loss improved 13% YoY due to smaller depreciation and net of tax benefits. EPS, already deeply negative, improved from ₹(26.7) to ₹(23.2), but this reflects share count fluctuations (equity issuance deferred pending sentiment improvement; warrant allotment in Sept 2025 at ₹222 per share raised ₹80.35 Cr).

Concall Color:

Management stated: “We expect these numbers to further improve in the coming financial year.” No guidance on breakeven timing or EBITDA positivity for