HPL Electric & Power FY26: Two Engines, One Bet That Markets Have Forgotten

Section 1: At a Glance

HPL Electric just delivered ₹1,811 Cr of revenue — a 6.5% climb to all-time highs — and the stock markets yawned. Down 37% over 12 months. But the narrative beneath the headlines is sharper: a company that has quietly shifted from one growth engine (smart meters) to two, and from a 9.92% ROE to the verge of something better.

Two signals clash. One whispers. One shouts.

The whisper: Cash profit grew 13.4% to ₹155.51 Cr, outpacing reported earnings. Order book sits at ₹3,200+ Cr — nearly double annual revenue. Smart meter execution rebounded hard after an industry-wide slowdown in Q1. CRISIL just upgraded to A+/Stable. Credit protection metrics are tightening. Wires & Cables just logged a 85% three-year revenue step-up.

The shout: P/E of 25.2x at a 9.92% ROE screams “overpaid smallcap.” Working capital days still stretch to 221. Depreciation spiked 49% post-capex, crushing reported PAT. The “second growth engine” (Consumer & Industrial) is 43% of revenue — meaningful, but still dependent on commodity prices and margin discipline that hasn’t fully proved itself.

So which is it? A hidden gem riding two structural tailwinds, or a leveraged smallcap betting everything on government’s smart meter push and cable pricing power?

What makes HPL worth the 15 minutes: It’s not the numbers everyone sees. It’s the two you have to find.

Section 2: Introduction

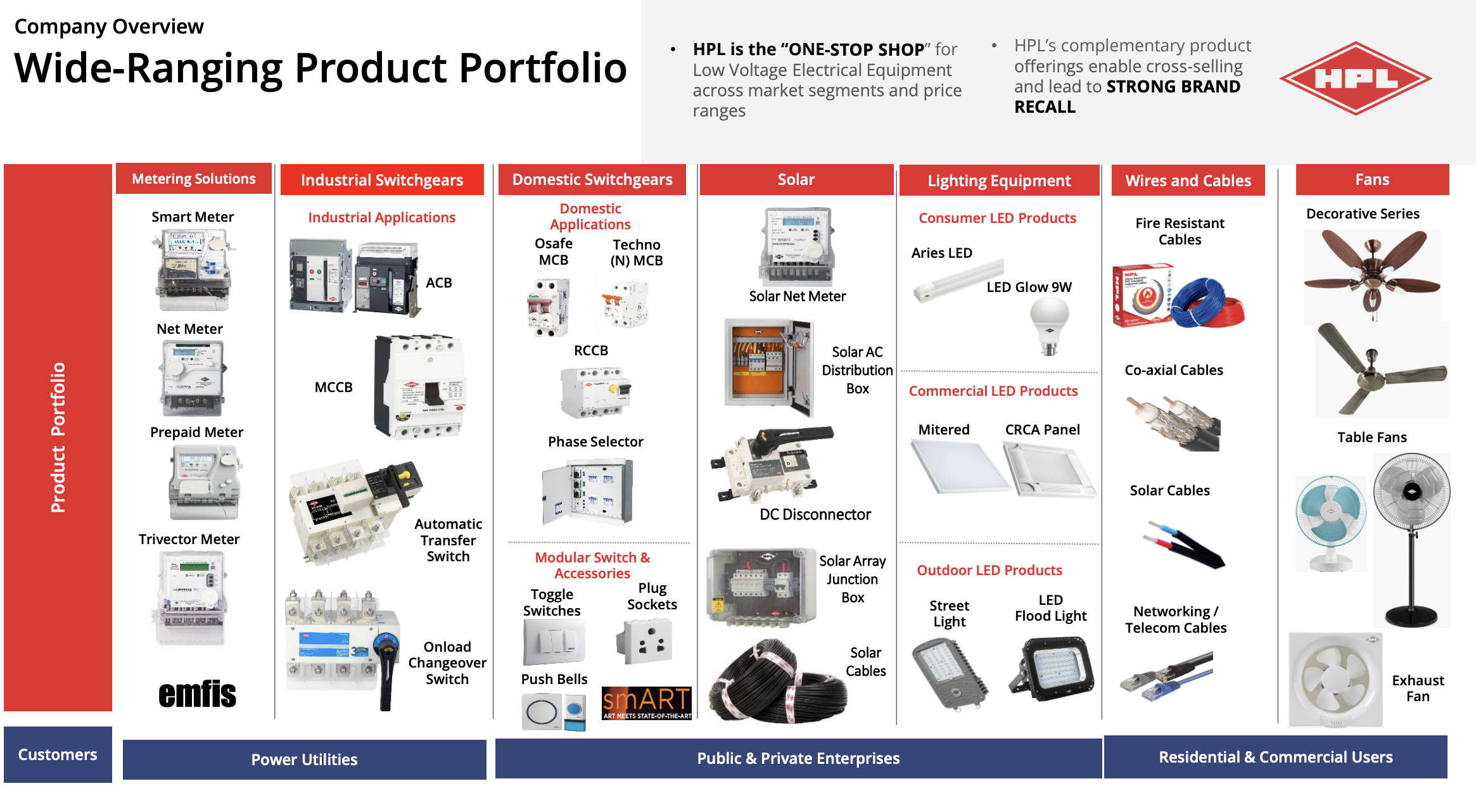

HPL Electric & Power Limited was incorporated in 1992 — two years before India’s telecom privatization kick-off, 12 years after Rajiv Gandhi’s computer imports. The company sells electrical equipment: meters, switches, cables, lighting, fans. Boring category, unglamorous products. For 40 years, it has quietly done what boring businesses do — grow in the shadows of sexier narratives.

But boring can be profitable if the tailwind is structural.

The story starts with Lalit Seth. In 1956 — before India’s independence was a generation old — he began importing meters from Europe. In 1998, HPL commissioned its first dedicated meter manufacturing plant. By FY26, it commands 20% of India’s domestic electric meter market and holds 50% of the on-load change-over switch market. The company exports to 42 countries. It owns 7 manufacturing facilities across Haryana and Himachal Pradesh, with 900+ authorized dealers and 85,000+ retailers — a distribution network that spans from Srinagar to Kanyakumari.

The shift:

For decades, HPL was a metering specialist. Smart meters — government-mandated, tender-driven, high-margin — became the growth pillar after 2018. By FY22, metering was 60% of revenue. But metering is tender-intensive, government-dependent, and lumpy.

Then something cracked. Between FY22 and FY26, Consumer & Industrial (wires, cables, switchgear, lighting) went from 40% to 43% of revenue. Not huge, but directional. Wires & Cables alone grew 85% in three years. Switchgear grew 33% in a single quarter (Q4). Lighting returned to growth after 18 months of price erosion.

The macro context:

India’s smart meter push remains real — ₹3.03 trillion allocated. But the deployment bottleneck shifted from policy to execution: AMISP (Advanced Metering Infrastructure Service Providers) on-ground capacity, last-mile connectivity, skilled manpower. Q1 FY26 saw an industry-wide slowdown. Q2–Q4 recovered. HPL’s metering revenue fell 4.6% YoY, but sequential recovery was +49.9% across the year — a rebound, not a collapse.

Meanwhile, Consumer & Industrial rode infrastructure capex: 5G rollouts, solar projects, data centers, real estate. The cable business — historically commodity-like — started acting like it had pricing power.

The valuation question:

At ₹357, HPL trades at 25.2x reported EPS. On a 9.92% ROE and 13.5% ROCE, that’s not cheap. But cash profit is growing faster than reported profit, and the company just raised debt capacity post-CRISIL upgrade. Order book of ₹3,200+ Cr (1.8x annual revenue) offers visibility. The question isn’t whether HPL is profitable — it clearly is. It’s whether two-engine growth, disciplined execution, and structural tailwinds justify the premium.

Section 3: Business Model: WTF Do They Even Do?

HPL sells five things:

1. Metering, Systems & Services (57% of FY26 revenue, ₹1,026 Cr)

Smart meters, conventional meters, prepaid meters, net meters — all sold under the brand Emfis. Government-mandated smart meter rollouts across India’s distribution companies (discoms) are the core. The government allocated ₹3.03 trillion for installation of 25 crore smart meters over the next decade. HPL has a ₹3,200+ Cr order book, 95% of which is smart meter orders.

The magic: HPL embeds Wirepas RF mesh technology (RF = radio frequency; mesh = self-healing network) into meters for real-time data transmission. No manual meter reading. No billing delays. Better revenue realization for utilities.

The catch: Utilities don’t buy directly anymore. They use AMISPs — private contractors who bundle hardware, software, deployment, and training. AMISPs order from HPL in 1–3 lakh meter lots, not 10–15 lakh “big bang” awards. This shifted the deal cadence from lumpy tenders to recurring purchase orders. Good for revenue visibility, bad for headline order wins.

2. Wires & Cables (19% of revenue, ₹341 Cr)

Fire-resistant cables, co-axial cables, solar cables — sold to real estate, OEMs, telecom (Jio, Vodafone), data centers, and solar companies. The three-year CAGR is 36%. Q4 alone logged +82% YoY growth. The business has moved from commodity pricing to something more structural: infrastructure capex (5G, solar, data centers) is durable.

Copper price volatility creates 2–3 week margin lag, but HPL has passed price increases 6–7 times in 9M. Margin pressure acknowledged, but pricing power is real.

3. Switchgear & Industrial Products (14% of revenue)

ACBs, MCBs, DC disconnectors, automatic transfer switches — industrial and domestic. Q4 grew +33% YoY to ₹68 Cr. Market share is 5% in low-voltage switchgear. Product mix is improving (new ATS lines, AFDDs, mini MCBs). Switchgear also faces copper/silver cost inflation, but newer product introductions are helping.

4. Lighting & Electronics (7% of revenue)

LEDs, street lights, panel lights, downlighters. This segment faced 18 months of price erosion due to industry-wide oversupply. Q1 FY26 marked stabilization. Q4 showed +20% YoY growth — a real inflection, not a blip. Management is betting on premium segments: outdoor LED (data centers, highways, 5G infrastructure).

900+ authorized dealers and 85,000+ retailers is the hidden advantage. HPL recently shrank from 30 warehouses to 6 master warehouses (cost discipline), but dealer relationships remain sticky. Channel activation via digital loyalty apps, QR codes, and electrician tie-ups is now in play. This reaches every retailer-electrician network in small towns.

Geography: 97% domestic, 3% export. Export ambitions exist (UK, Europe FTA tailwinds), but domestic saturation is not near.

Section 4: Financials Overview

Figures are consolidated, in ₹ crore.

Metric

FY26

FY25

YoY

Q4 FY26

Q4 FY25

YoY

Revenue

1,811

1,700

+6.5%

520

493

+5.5%

EBITDA

281

255

+10.5%

86

82

+4.3%

PAT

91

94

-2.9%

31

37

-17.1%

EPS

14.15

14.58

-2.9%

4.80

5.78

-17.0%

The apparent miss: Revenue grew 6.5%, EBITDA grew 10.5%, but PAT fell 2.9%. How?

Depreciation spiked 49.6% to ₹63.2 Cr — a post-capex effect from manufacturing facility automation and new production lines. This is temporary drag, not structural weakness. Strip it out: Cash Profit grew 13.4% to ₹155.5 Cr. This is the true operational picture.

Margin story:

EBITDA margin improved 56 bps to 15.54%. Gross margin expanded 97 bps to 36.01%. This happened despite Wires & Cables facing copper inflation and Smart Metering facing execution friction. Why? Metering segment margins improved 51 bps (17.52% in FY26 vs 17.01% in FY25) despite lower volume — pricing discipline. Consumer & Industrial margins compressed 124 bps (10.21% vs 11.45%) due to input cost pass-through lags, but this is cyclical, not permanent.

What management promised (concall, Feb 2026):

Management said “20–25% topline growth is achievable” for FY27. This rests on: (a) metering policy clarity holding, (b) AMISP execution improving, (c) Consumer & Industrial channel scale-up. Not guidance. An expectation.

Smart Metering subsection:

Q1 FY26 saw an industry-wide deployment slowdown (weather, last-mile execution, utility coordination). But Q2 rebounded +14% QoQ, Q3 +26% QoQ, and Q4 +6% QoQ, reaching ₹305.7 Cr — the strongest FY26 quarter. This is sequential recovery, not