DEE Development FY26: Heavy Metal Engineering Meets Heavy Working Capital

1. At a Glance

High-pressure project execution and a massive structural order book defined the full-year trajectory for this specialized engineering player. The headline performance was driven by a powerful acceleration in the core piping division, which benefited from a cyclical upsurge in domestic thermal power ordering and international gas turbine capital expenditure cycles. Topline expansion comfortably outpaced historical averages, supported by the rapid commercial operationalization of scaled capacity additions.

However, beneath the sharp acceleration in net profitability lies a structural asset footprint that remains intensely working capital heavy. Extended milestone-based billing timelines and strategic raw material safety stocking ahead of fixed-price contract deliveries have kept inventory days highly elevated, leading to a prolonged cash conversion cycle. Operating cash flows diverged meaningfully from headline accounting profits as absolute working capital deployment absorbed incoming liquidity.

While a milestone tariff revision in the non-core biomass power segment provided immediate relief and mechanical write-backs, the investment thesis remains strictly bound to execution efficiency and raw material cost protection.

Financial Wisdom Drop: A roaring order book provides excellent multi-year revenue visibility, but unless execution milestones translate directly into predictable ledger collections, a business risks growing its way straight into a severe liquidity squeeze.

The core operational challenge going forward centers on ramping asset utilization across newly integrated processing mills while systematically working down the extended inventory cycle.

2. Introduction

DEE Development Engineers Ltd is not your neighborhood hardware shop. The company is a specialized engineering powerhouse operating at the hyper-critical intersection of high-pressure process piping, heavy metal fabrication, and modular skid assembly. If an oil refinery, nuclear facility, or thermal power giant needs to move volatile, high-temperature fluids without triggering an industrial catastrophe, they dial this company.

The corporate journey has transitioned from design-led component manufacturing toward heavily integrated engineering systems. With the recent completion of a major growth capital expenditure cycle, the company is attempting to transform itself from a pure-play project contractor into a structurally hedged engineering platform. Wry observers will note that while the corporate tagline promises to “make every customer a repeat customer,” the balance sheet is currently working overtime to ensure the lenders are equally attached.

3. Business Model: WTF Do They Even Do?

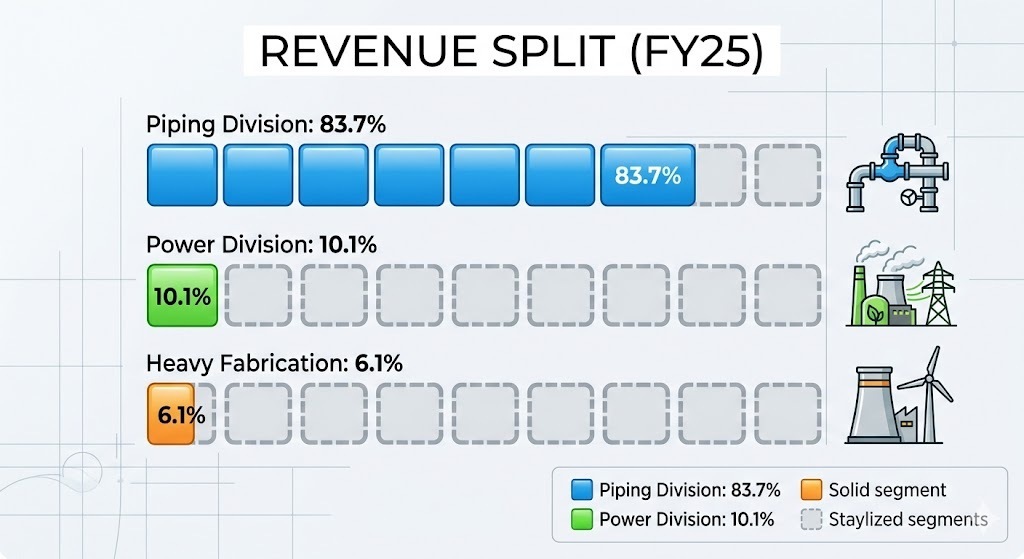

To put it bluntly, the company designs, bends, welds, and stress-tests gigantic metal tubes that can withstand pressures high enough to crush a tank. Their bread and butter is the Piping Division, which brought in a resounding 83.7% of total revenues in FY25, followed by the Power Division at 10.1%, and a small Heavy Fabrication slice at 6.1%.

They take massive steel cylinders, convert them into customized prefabricated “piping spools” or modular skids offsite, and ship them to global players like Reliance, Mitsubishi, and Toshiba. It is a high-barrier sandbox because qualifying as a vendor takes years of auditing.

Strangely, management also operates two biomass power plants in Punjab because nothing screams “process engineering excellence” quite like burning paddy straw to generate electricity under long-term state contracts. This non-core segment has historically acted as a margin sponge, absorbing cash generated from the core business to fund regional power-grid drama.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Headline Performance Table

Metric

Latest Quarter (Q4 FY26)

YoY (%)

QoQ (%)

Revenue

361.57

+26.3%

+26.1%

EBITDA / Operating Profit

63.64

+0.2%

+33.6%

PAT

28.01

-11.1%

+53.2%

EPS (Reported)

4.04

-11.0%

+53.0%

Did Management Walk the Talk?

Reviewing past execution signals reveals a management team that loves a good swaggering projection. During previous quarters, leadership repeatedly hammered home that their core business EBITDA was running ahead of the consolidated pack, and they have delivered on that absolute volume growth.

However, they also promised that the commissioning of the new Anjar facilities would instantly smoothen the working capital drag. Instead, the inventory lines continued to bloat, which management calmly brushed aside as “strategic stocking” to feed their massive execution pipeline. Wryly speaking, when management calls a multi-month buildup of steel inventory a “strategic advantage,” the cash flow statement usually begs to differ.

On the non-core front, they spent the last year complaining about a suppressed tariff at the Malwa Power plant. This quarter, they finally secured a tariff revision to ₹5.22/kWh, complete with a back-dated recovery of ₹5.14 crore. Management noted that this long-awaited regulatory