Rajshree Sugars FY26: A ₹31.64 Crore Sweetener to Clean Up a Sticky Balance Sheet

Section 1 — At a Glance

Rajshree Sugars & Chemicals Ltd wrapped up fiscal year 2026 by proving that in the sugar business, financial survival requires a healthy dose of cyclical drama. The top-line numbers revealed an accelerating contraction, with annual revenue shrinking 15.14% year-on-year to ₹544.68 crore, down from ₹641.82 crore in the prior year. Yet, beneath this thinning top-line crust lay a massive quarterly surprise. The company recorded a net profit of ₹31.64 crore for the final quarter alone, engineering a dramatic swing against its previous nine-month trajectory. This eleventh-hour push allowed full-year net profit to scrape into positive territory at ₹1.14 crore.

While the bottom-line numbers flash green, deep balance sheet strains continue to demand strict investor vigilance. Promoters have pledged a staggering 100% of their equity shares, leaving the operational steering wheel vulnerable to external market shifts. Concurrently, long-term capital efficiency remains deeply depressed, with a Return on Capital Employed (ROCE) of just 3.18%. In cyclical commodities, a sudden spike in quarterly profits can mask structural inefficiencies if the underlying capital engine fails to generate real economic value. This analysis evaluates whether the recent quarterly surge signifies an operational pivot or simply a temporary cyclical high.

Section 2 — Introduction

Rajshree Sugars & Chemicals Ltd, incorporated in 1985 and headquartered in Coimbatore, is an integrated sugar manufacturer operating across Tamil Nadu. Over the decades, it has evolved from a simple sugarcane crushing unit into an integrated enterprise managing sugar refining, biomass-based power generation, and industrial alcohol distillation.

The company’s primary processing footprints are distributed across three production facilities located in Theni, Villupuram, and Gingee. These plants operate in a highly synchronized loop, converting sugarcane waste (bagasse) into electricity and molasses into alcohol. This structural integration is meant to buffer the company against volatile sugar pricing. However, legacy debt burdens, severe regulatory constraints, and periodic raw material shortages in its regional crop belts have historically limited its ability to build sustainable financial momentum.

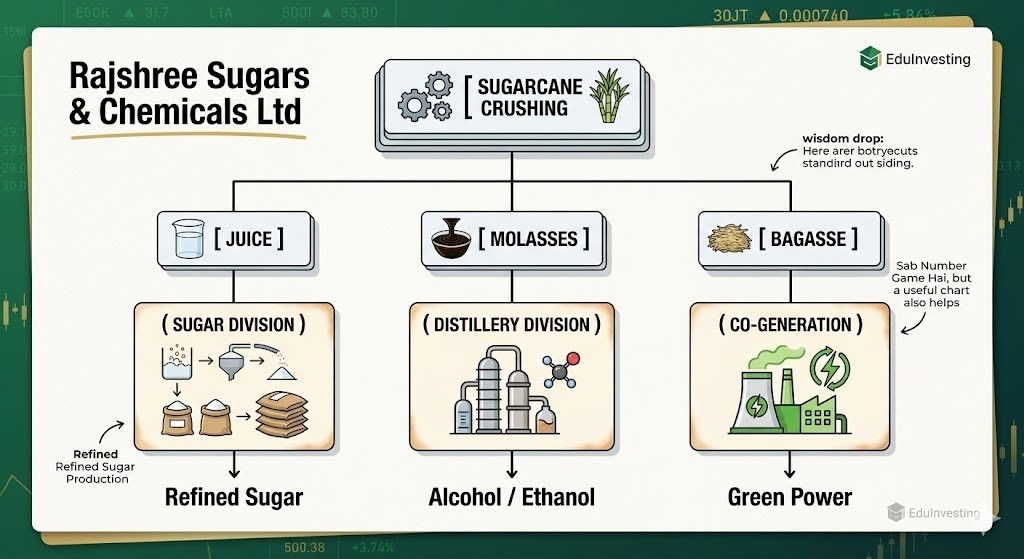

Section 3 — Business Model: WTF Do They Even Do?

The company relies on an integrated circular production model designed to extract commercial value from every stage of sugarcane processing.

Sugar Division: This is the core volume driver, accounting for roughly 73% of overall segment revenues under normalized conditions. The company commands an aggregate crushing capacity of 11,500 tons of cane per day (TCD).

Co-Generation of Power: The fibrous leftover residue from sugarcane crushing, bagasse, is fed into boilers to generate electricity. It features an aggregate power capacity of 54.5 megawatts across its facilities, supplying internal operations and exporting excess units to the state grid.

Distillery & Alcohol: This business processes molasses, a heavy byproduct of sugar production, into industrial alcohol and fuel-grade ethanol. It runs a combined processing footprint of 125 kilo liters per day (KLPD).

Bio Products: A small secondary division utilizing filter press mud and organic processing waste to formulate biocomposts and agricultural inputs.

Section 4 — Financials Overview

Figures are standalone, in ₹ crore.

Headline Performance Metrics

Metric

Latest Quarter (Mar 26)

YoY (%)

QoQ (%)

Revenue

₹188.93

+8.24%

+92.81%

EBITDA / Operating Profit

₹51.87

+83.42%

Positive Turn

PAT

₹31.64

+100.25%

Positive Turn

EPS

₹9.55

+166.76%

Positive Turn

Did Management Walk the Talk?

Reviewing the company’s long-term financial disclosures highlights a protracted battle with legacy financial defaults. Management spent nearly a decade in default on loans extended by the government’s Sugar Development Fund (SDF). After a series of restructuring updates failed to take hold due to asset coverage shortages, management took decisive steps over the last year.

They pursued a comprehensive One Time Settlement (OTS) scheme with the SDF, culminating in a final execution in March 2025. Operational data indicates that management delivered on its pledge to clear institutional encumbrances. They completely eliminated their term loan obligations with ICICI Bank through non-core asset sales and core operating cash flows. This aggressive debt clearance paved the way for an long-awaited