Samvardhana Motherson International Ltd. Mar 2026: The ₹1,26,104 Crore Global Auto Giant Scaling New Peaks

Section 1 — At a Glance

Samvardhana Motherson International Ltd. (SAMIL) wrapped up an monumental fiscal year with its highest-ever annual revenue touching ₹1,26,103.67 crore. This performance reflects a steady 11% top-line expansion, driven primarily by resilient automotive demand in emerging markets and aggressive inorganic consolidations. While group revenues scaled unprecedented operational heights, the underlying margin profile was tested by severe external crosswinds. Sharp commodity inflation—with international copper spot prices jumping 16% sequentially—combined with volatile European logistical frameworks to keep full-year reported operating profit margins flat at 9.44%.

What is captivating long-term equity investors is the rapid scale-up of SAMIL’s structural business diversification. Its non-automotive segments, specifically aerospace engineering and consumer electronics manufacturing, are registering explosive growth metrics, with aerospace expanding 40% year-on-year. Furthermore, the company has reinforced its financial position, compressing its core leverage ratio down to 0.8x—the lowest net debt-to-EBITDA framework recorded in the firm’s history.

However, critical risks persist underneath the stellar headline numbers. While domestic demand structures remain exceptionally robust, industrial production frameworks across Western and Central Europe continue to display structural softness, necessitating expensive business transformation exercises. Rising systemic interest rates and raw material volatility also continue to penalize underlying return ratios, keeping the company’s return on equity compressed at 10.9%. True corporate scale is an incredible operational shock absorber, but unbridled inorganic diversification always tests long-term capital execution. Can this global tier-1 giant seamlessly transition its massive auto-component muscle into emerging electronics and aerospace domains without diluting its historical return baseline?

Section 2 — Introduction

Samvardhana Motherson International Ltd. has transformed itself from a domestic wire manufacturer into a specialized Design, Engineering, Manufacturing, Assembly, and Logistics (DEMAL) global powerhouse. The company commands an omnipresent structural footprint spanning 425 operational facilities across 47 individual nations. This massive industrial reach allows SAMIL to position itself adjacent to nearly every major global automotive original equipment manufacturer (OEM) assembly line, providing just-in-time logistical integration.

The publication of this analysis coincides with a defining structural juncture for the enterprise. Having spent the last two fiscal years executing a wave of high-profile global acquisitions—including Atsumitec, Yutaka Giken, and Nexans AutoElectric—the corporate emphasis is transitioning from raw deal assembly to rigorous operational optimization. With a massive total booked business pipeline standing at a colossal USD 96 billion, the investment community’s focus has fundamentally shifted to a critical metric: execution velocity. This deep-dive report is engineered to cut through the intricate labyrinth of cross-border corporate restructurings, multi-segment revenue streams, and localized manufacturing variables to evaluate whether SAMIL’s equity framework represents a structurally de-risked global engineering compounder or an overly extended, capital-intensive macro proxy.

Section 3 — Business Model: WTF Do They Even Do?

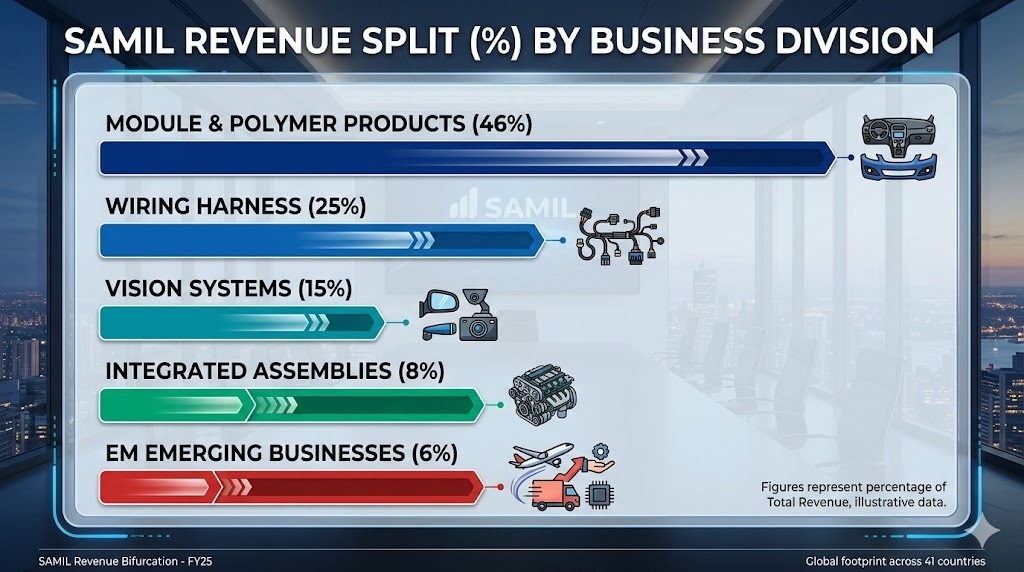

If you think SAMIL is just a humble factory making plastic dashboards, you are missing the entire multi-layered plot. The company operates as a global automotive component integrator. They manage complex supply chains, design high-spec systems, and assemble critical components. Their operational architecture is split across four core automotive pillars and a rapidly accelerating emerging business basket:

Modules & Polymer Products (46% of Revenue): The massive core of the ship, manufacturing massive, highly visible components from front bumpers and instrument panels to complete cockpit assemblies.

Wiring Harness (25% of Revenue): The intricate nervous system of vehicles, where they operate as an unshakeable market leader in India and a critical global supplier for commercial heavy vehicles.

Vision Systems (15% of Revenue): A domain where they hold a virtual global stranglehold, supplying high-tech exterior and interior rear-view mirrors and camera-detection rigs to almost everyone.

Integrated Assemblies (8% of Revenue): Operating as a sophisticated “tier 0.5” assembly partner, taking parts from dozens of client-specified vendors and delivering ready-to-mount modules directly to lines.

Emerging Businesses (6% of Revenue): The high-growth wild card, stretching their plastic molding and wiring capabilities into defense, aerospace, logistics, and high-volume consumer electronics.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Comparison Table

Metric

Latest Quarter (Mar 2026)

YoY (%)

QoQ (%)

Revenue

34,309.31

17.03%

9.23%

EBITDA

3,805.00

42.24%

25.04%

PAT

1,497.14

9.14%

46.25%

EPS

3.66

1.67%

0.00%

Financial Narrative & Performance Analysis

The final quarter of the fiscal year delivered an outstanding top-line surge, with quarterly revenue accelerating past the ₹34,300 crore mark, driven by robust performance across business divisions and the timely consolidation of the Atsumitec entity. EBITDA margins staged an impressive recovery to hit 11.1%, largely due to comprehensive cost-saving and operational transformation frameworks rolling out through their European polymer facilities. Diversification is the only real armor an industrial business has against macro volatility. While intense copper cost inflation penalized the wiring harness division, the polymer business optimization absorbed the blow. Reported net profit for the quarter landed at ₹1,497.14 crore, though this includes exceptional charges of ₹177 crore tied directly to the structural execution of Western European restructuring programs.

What is Management Promising in the Coming Quarters?