Asian Energy Services Ltd Mar 2026 : Revenue Scales 70% to ₹791 Crore on Global Resourcing & Energy Supercycle Inflection

Section 1 — At a Glance

Asian Energy Services Ltd (AESL) has orchestrated a significant operational scale-up in the fiscal year ended March 31, 2026, positioning itself at the intersection of India’s aggressive energy security mandates and global upstream capital expansion. Total revenue from operations surged by 70.1% to touch ₹791.05 crore, up from ₹465.04 crore in the previous fiscal year, driven by heavy execution momentum in the core oil and gas services domain and structural inorganic contributions. The company’s consolidated Operating Profit (EBITDA) tracked this topline expansion, climbing 36.6% to reach ₹98.89 crore against ₹72.41 crore in FY25. Consolidated profit after tax (PAT) followed a similar trajectory, expanding by 23.0% to settle at ₹51.91 crore. Reported net profit stood at ₹51.16 crore, translating to a basic EPS of ₹11.38 on an adjusted equity share base of 4.49 crore shares.

While headline revenue compounding remains strong, investor focus is closely split between structural margin deviations and asset-heavy integration parameters. The consolidated EBITDA margin experienced a compression of 310 basis points, declining from 15.6% in FY25 to 12.5% in FY26, largely reflecting project-specific cost variances, a one-time acquisition drag from the international Kuiper consolidation, and acute localized supply-chain logistics delays originating from conflicts in West Asia. Despite these short-term execution challenges, a high-conviction unexecuted order book of approximately ₹1,750 crore (excluding the international Kuiper portfolio) safeguards near-to-medium term top-line visibility. Management has underscored this structural turnaround by proposing a dividend of ₹1.25 per share. Corporate performance metrics indicate an improving fundamental landscape, but persistent working capital constraints—highlighted by elevated debtor cycles—underscore the reality that operational expansion must be carefully balanced with strict cash-flow management.

Section 2 — Introduction

Asian Energy Services Ltd has structurally pivoted from its historical position as a seasonal, domestic seismic data provider into an integrated, international energy infrastructure and operation services platform. Operating across multiple high-stakes vectors within the upstream hydrocarbon and mineral handling corridors, the company has positioned itself to capture the tailwinds of a major domestic upstream capital cycle. This analysis emerges at a vital corporate juncture: the organization is currently processing a comprehensive scheme of arrangement to merge its parent holding entity, Oilmax Energy Private Limited (OEPL), directly into its listed structure, an exercise expected to conclude by September or October 2026.

By incorporating Kuiper Group’s international energy resourcing networks alongside Oilmax’s producing fields, the post-merger entity is engineered to transition from a pure-play, bid-dependent services contractor into an asset-backed production platform. This structural evolution addresses the historical volatility embedded in project-based micro-cap energy cycles, creating a more predictable and diversified revenue stream.

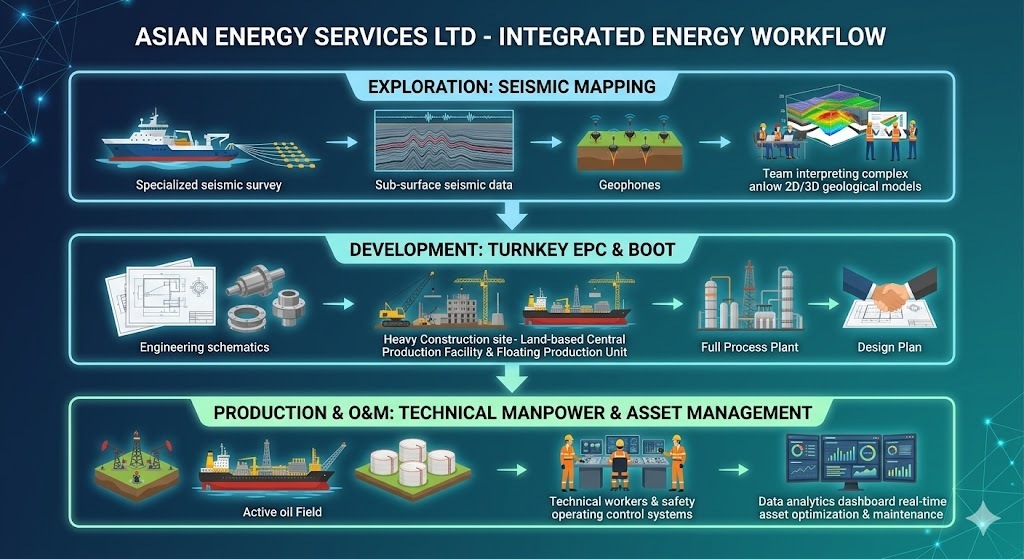

Section 3 — Business Model: WTF Do They Even Do?

To the smart but comfortably detached investor, Asian Energy operates as an industrial general contractor for heavy infrastructure and technical staffing across the oil, gas, and mineral exploration lifecycles. They do not simply dig holes; they map fields, build surface production structures, run the daily operations of mature oilfields, and engineer high-volume bulk material handling systems for coal miners.

The revenue framework is divided into two operational engines:

Integrated Oil & Gas Vertical (80% of Q1FY26 Revenue): Delivers land/transition-zone seismic data acquisition, turnkey engineering, procurement, and construction (EPC) solutions, and multi-year operations & maintenance (O&M) contracts for onshore and floating offshore infrastructure (FPSO/FPU).

Mineral and Infrastructure Vertical (20% of Q1FY26 Revenue): Executes fast-track bulk material logistics systems, continuous coal handling plants (CHP), and mining process-infrastructure engineering.

Through the newly integrated Kuiper Group, the business adds an asset-light international technical resourcing framework. This mechanism functions as a specialized, high-margin international deployment pipeline for energy majors across West Asia and Southeast Asia, decoupling a portion of corporate profitability from domestic infrastructure execution cycles.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly and Annual Performance Comparison

Metric

Latest Quarter (Mar 2026)

YoY change (%)

QoQ change (%)

Full Year FY26

Full Year FY25

YoY change (%)

Revenue

338.23

57.0%

43.6%

791.05

465.04

70.1%

EBITDA / Operating Profit

47.75

46.6%

42.7%

98.89

72.41

36.6%

PAT

31.96

44.8%

46.4%

51.91

42.12

23.0%

EPS (₹)

7.11

41.1%

43.6%

11.38

9.41

20.9%

Note: Minor discrepancies between sequential accounting alignments and absolute metrics in tables trace precisely to consolidated share allocations from joint-venture adjustments and specific asset tax provisions.

The fourth quarter showcased strong execution acceleration, with standalone and consolidated volumes expanding sharply. However, this surge arrived after minor supply-chain bottlenecks in preceding periods. Topline momentum was temporarily held back by an estimated ₹75 crore revenue deferral in the standalone domestic service segment, caused by regional maritime logjams in West Asia and client-side readiness constraints. These impacts are timing-related rather than structural cancellations, shifting the associated high-margin realizations directly into the FY27 opening quarters.

Earnings quality ultimately hinges on the speed of conversion from contract wins to cash