Zydus Lifesciences Q4 FY26: The $166 Million Pivot from Cheap Generics to Expensive Platforms

Section 1 — At a Glance

Zydus Lifesciences finished its fiscal year 2026 on an aggressive note, with annual consolidated revenue from operations tracking at ₹27,148.4 crore and final net profit landing at ₹5,040.0 crore. The headliner for investor chatter is a sharp expansion in operating margins, which closed at an all-time high of 31.2% for the full year, driven by a high-value mix shift in the domestic branded formulation business and timely foreign exchange tailwinds. Yet, while headline profitability looks bulletproof, structural cash dynamics reveal a more complex operational undercurrent.

Annual operating cash flow decelerated sharply to ₹2,116.6 crore from ₹6,776.7 crore in the preceding fiscal period. This compression points squarely to working capital adjustments and intense capital deployment into international specialty pipelines. Concurrently, gross borrowings ballooned from ₹3,213.2 crore to ₹12,496.0 crore, reflecting an aggressive, debt-financed inorganic strategy to break out of low-margin generic spaces. True capital compounding requires turning operating accounting profits into real, unencumbered liquid surpluses. Investors are closely monitoring whether this massive capital outlay will yield structural competitive advantages or merely create a collection of underperforming assets. The immediate road ahead tests whether management can defend its >24% operating margin threshold amidst intensifying regulatory friction and core product competition.

Section 2 — Introduction

Zydus Lifesciences has travelled a long road from its humble restructuring setup in 1995 when it operated with a turnover of just ₹250 crore. Today, the consolidated entity has firmly positioned itself as India’s 5th largest generic player in the US and a dominant power player in chronic therapies at home.

The rationale for looking at Zydus right now is its aggressive, multi-million-dollar structural transformation. The company is actively attempting to shed its old identity as a traditional generic copier to become a specialty, asset-heavy innovator. With a flurry of overseas acquisitions—spanning from direct-to-consumer digital wellness footprints in the UK to biologics infrastructure in the US—the company’s balance sheet has fundamentally pivoted. This report breaks down the financial machinery behind this transition, dissecting whether the core business can successfully fund management’s global specialty ambitions.

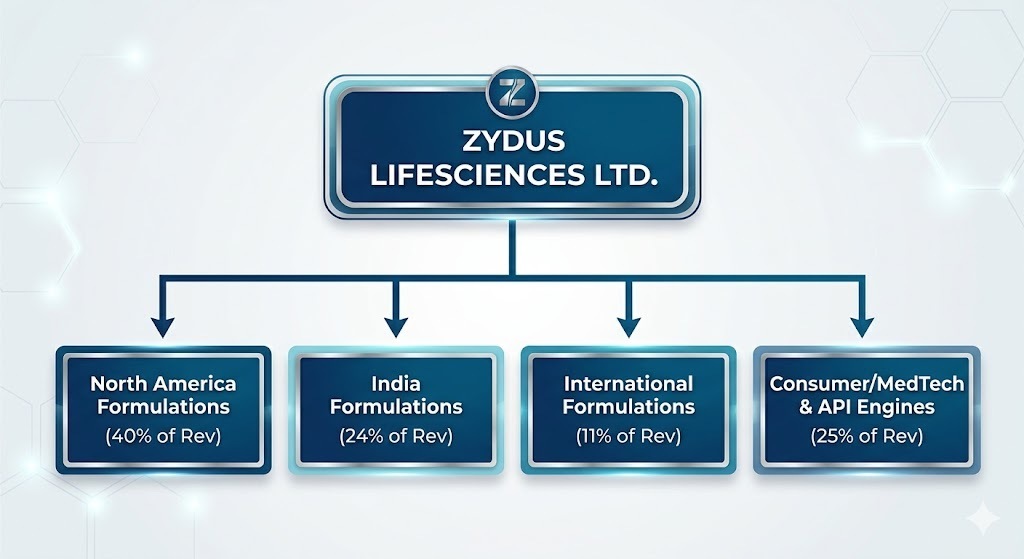

Section 3 — Business Model: WTF Do They Even Do?

At its core, Zydus is a diversified healthcare house that runs on three main engines and two experimental platforms.

The primary engine is North America Formulations (40% of Q4 revenues), where it sells over 200 generic products and ranks 3rd by generic prescriptions in the US. The domestic engine is India Branded Formulations (24% of revenues), targeting high-margin chronic therapies like cardiology, dermatology, and oncology. The third scale piece is Consumer Wellness (20% of revenues), retailing household wellness brands like Glucon-D, Sugar Free, and Nycil.

The two new pillars are International Formulations (11%) and an emerging MedTech and API segment (6%), which covers advanced medical equipment and raw ingredients. Zydus handles a sprawling supply chain of 4,500+ stock-keeping units across 43 manufacturing sites globally, backed by an R&D engine that swallows 7% to 8% of top-line revenue annually to discover new chemical entities and biosimilars.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Latest Quarter (Mar ’26)

YoY (%)

QoQ (%)

Revenue

₹7,587.0

+16.2%

+10.5%

EBITDA / Operating Profit

₹2,554.4

+20.2%

+40.6%

PAT

₹1,272.5

+8.7%

+22.1%

EPS (₹)

₹12.65

+7.7%

+22.0%

Note: Quarter-on-quarter and Year-on-year metrics calculated directly from the locked quarterly tables.

Did Management Walk the Talk?

Reviewing management’s historical guidance against the current financial output reveals accurate operational execution. In earlier discussions, management guided for double-digit US baseline growth and a structural expansion of EBITDA margins by 100–150 basis points over the FY24 base.

They delivered exactly on that roadmap. Full-year FY26 EBITDA reached ₹8,475.1 crore , with the operating margin moving up to 31.2%. The sequential jump of 720 basis points in EBITDA margins during Q4 FY26 (reaching 33.7%) highlights strong operational execution, though it was amplified by considerable foreign exchange gains of ₹644.9 crore during the quarter. Accounting profits can be temporarily enhanced by currency