1. At a Glance

Picture this: a company that literally sells colour—and still manages a ₹1,693 crore market cap. That’s Vidhi Specialty Food Ingredients Ltd, Asia’s second-largest and the world’s third-largest synthetic food-grade dye manufacturer. While most FMCG companies fight over shelf space, Vidhi’s colours are already inside the products you buy. From the red in your cola to the orange in your namkeen—there’s a high chance you’ve been eating Vidhi’s art supplies for years.

As of Q2 FY26, the stock trades at ₹339, down 11% in three months (apparently even colours can fade). But don’t be fooled—Vidhi’s Q2 FY26 PAT stood at ₹10.7 crore, up 2.98% QoQ, while revenue dipped 17.9% QoQ to ₹75 crore. Their OPM of 24% shows they know how to squeeze profit out of pigment. The stock’s P/E stands at 35.2x, compared to an industry average of 30.7x—clearly investors think “shade of blue” deserves a premium. Dividend yield? 1.46%, not bad for a smallcap that still has both elbows deep in chemicals.

So what’s the punchline? Vidhi may look like a small-cap, but it’s painting the global food map—one artificially enhanced hue at a time.

2. Introduction

If you ever looked at a pack of candy and thought, “How does this neon green even exist?”, well, meet the magician behind it—Vidhi Specialty Food Ingredients. The company’s pitch is simple: while you focus on taste, they handle your food’s Instagrammability. Incorporated in 1994, Vidhi has quietly built a pigment empire across Raigad and Bharuch, exporting to more than a dozen countries from Italy to Indonesia.

But don’t underestimate this “food colour” business—it’s a ₹371 crore revenue engine with EBITDA margins north of 20%. The beauty? Their top 10 countries alone contribute over 76% of revenue, proving this isn’t some random backyard dye operation. They’re exporting to Nestlé, Mars, Pedigree, and Sanofi—brands that care deeply about consistency (and colour).

In a world obsessed with “natural” everything, Vidhi manages to thrive with synthetic. Irony? Maybe. Profitability? Definitely. The firm’s expansion to Dahej SEZ and upcoming Roha plant suggests they’re gearing up for a saturation-proof future. The only question is—can they maintain these shades of margin when global raw material prices swing harder than Holi balloons?

3. Business Model – WTF Do They Even Do?

Let’s decode Vidhi’s world of food colouring.

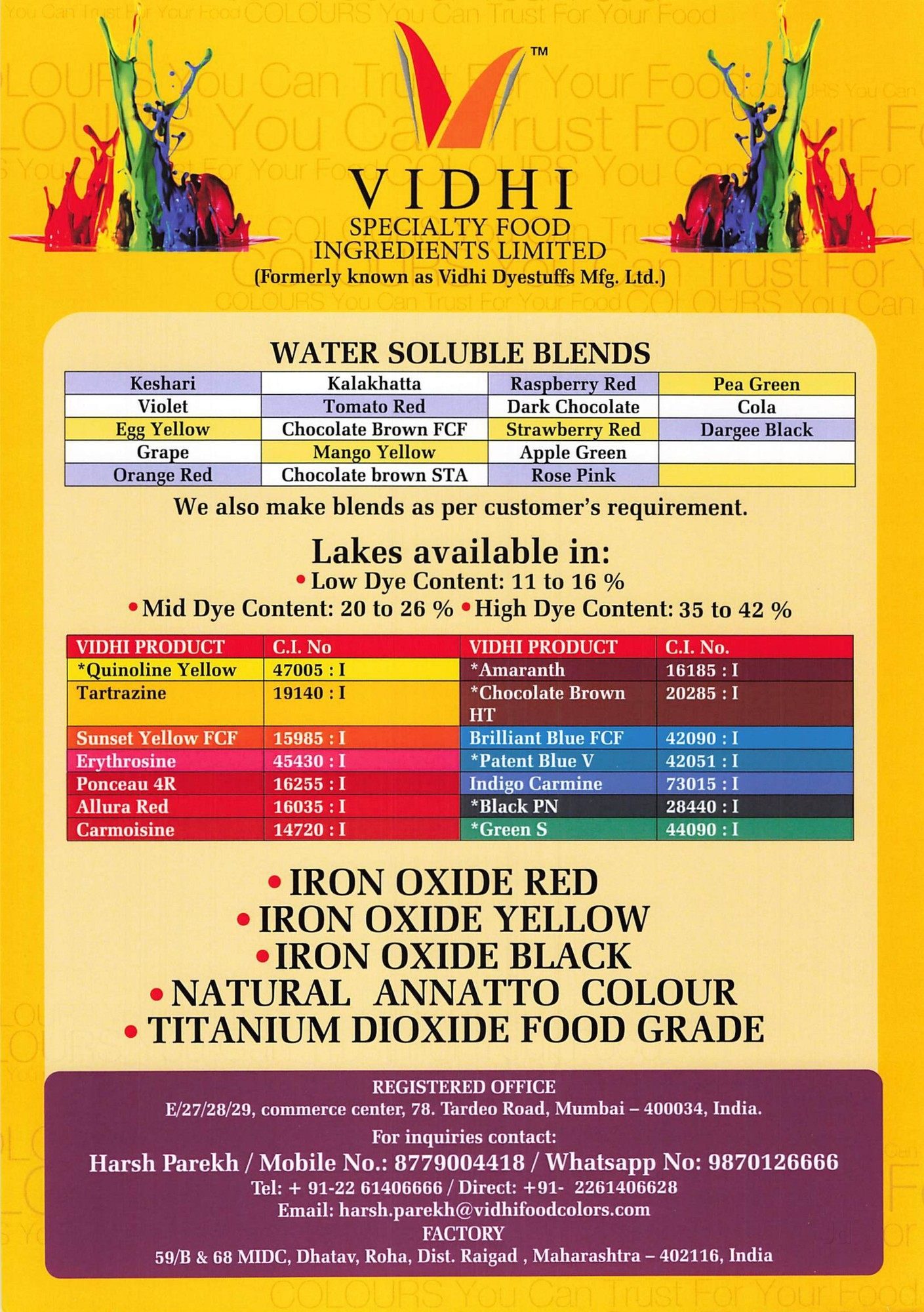

They make synthetic and natural food-grade colours—basically the chemicals responsible for making your orange soda orange, your strawberry jam pink, and your dog’s biscuit… somehow blue. Their seven-segment portfolio includes water-soluble colours, aluminium lakes (used for surface coatings), D&C colours (pharma and cosmetic grade), and custom blends for clients who want that perfect shade of ketchup red.

Applications? Everywhere:

- Food & Beverages – The core market (because nobody wants beige cola).

- Pharmaceuticals – Ever wondered why your syrup is red and not depression-grey? Thank Vidhi.

- Pet Foods – Dogs apparently judge food by colour too.

- Cosmetics, Home Care, and Inkjet Inks – Yes, they even supply colour for things that shouldn’t be eaten.

Their manufacturing scale is serious: 7,500 MTPA capacity across two plants (Roha & Dahej). They’re expanding both—with Dahej already operational since Dec 2023 and Roha on track to add 360 TPM by FY26. The entire expansion is self-funded—no debt binge, no dilution drama. Just pure internal accruals and some chemical wizardry.

So essentially, they’ve built a moat where competition can’t