Wonder Electricals Mar 2026: Revenue Collapsed, Margin Steady, Debt Climbed

General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

1. At a Glance

Wonder Electricals reported FY26 revenue of ₹655 Cr—a 27% drop from ₹894 Cr in FY25, the steepest collapse in a decade. Net profit halved to ₹9.1 Cr from ₹19 Cr.

The quarter itself (Q4 FY26, Mar 2026) shipped ₹252 Cr in sales, down 19% YoY. The company’s margin—operating profit as a percentage of sales—remained flat at 4.3% across both year and quarter.

Borrowings swelled to ₹112 Cr from ₹85 Cr in FY25. The market cap sits at ₹1,240 Cr on a price of ₹92.9 per share. The P/E on annualised Q4 EPS is a dizzying 136x. Cash on the balance sheet is a rare bright spot: ₹28.5 Cr, up from ₹0.4 Cr in FY25. Receivables remain stretched at 139 days.

The company is hunting for growth—new products, capacity additions, a joint venture for PCBs—but the current year shows demand is weak, margins cannot expand under price pressure, and the execution risk is live.

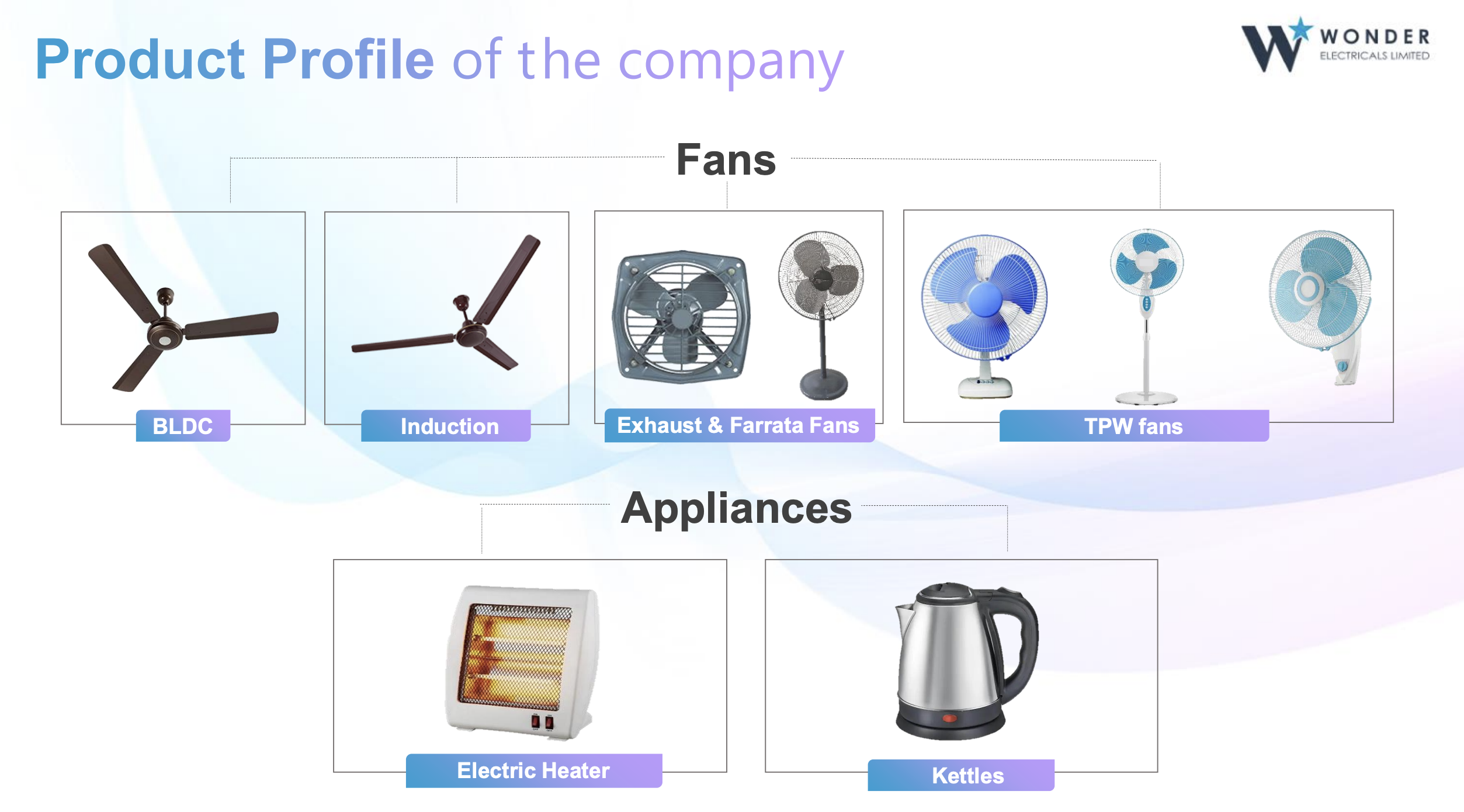

2. Introduction

Wonder Electricals is an original equipment manufacturer (OEM) and original design manufacturer (ODM) in the fan business, supplying ceiling, exhaust, pedestal, BLDC, and ancillary products to major Indian appliance brands. The company also exports to Gulf and neighboring countries.

The firm was incorporated in 2009. In July 2018 it migrated to the main boards of NSE and BSE. In late 2023, it acquired the manufacturing business of Uttaranchal Industries (UTI), a promoter-owned partnership, consolidating production under one roof.

The promoters—Harsh Anand, Yogesh Anand, and Yogesh Sahni—have over four decades of industry experience and retain 71.8% of equity. The company operates three manufacturing plants: Roorkee (9,500 sq m land, 640 kW solar), Haridwar (3,600 sq m land, 110 kW solar), and Hyderabad (7,200 sq m land, 128 kW solar). Total installed capacity is 12 million units per year.

Recent announcements flag new product lines (electric heaters, ventilating fans, kettles), a TPW (Table, Pedestal, Wall) fan expansion at Haridwar, and a 51%-owned PCB joint venture to support in-house BLDC motor production.

3. Business Model: WTF Do They Even Do?

Wonder Electricals manufactures fans on two models: OEM (customer-specified designs, built to order) and ODM (in-house design, marketed and supplied). The company supplies to 10+ branded players and handles exports.

The product mix in 9MFY25 was heavily tilted to induction fans (44.37 lakh units), followed by exhaust/farrata/TPW fans (0.96 lakh units) and BLDC fans (3.86 lakh units). FY25 data shows 86 lakh fan units sold across all types.

The business is working capital intensive. Debtors sit at 139 days—which means cash is locked in receivables for 4+ months. Inventory turns within 42 days. Payables clock 115 days, meaning the company gets some float but not enough to offset the receivables drag.

The moat is thin: the company manufactures what customers specify, operates thin margins (4.3%), and competes on cost and delivery against large multinationals and smaller local players. BLDC fans are higher margin but depend on supply of BLDC motors and controllers—hence the PCB JV attempt to gain control. Price competition is brutal. Raw material and labor volatility are permanent headwinds.

The new appliance launches (heaters, kettles) suggest the company wants to diversify away from fans, but these are greenfield, unproven, and the base case remains ceiling fans for Indian appliance brands.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest FY (Mar 2026)

Prior FY (Mar 2025)

Change YoY

Sales

654.75

894.39

-27%

EBITDA

36.7

41.2

-11%

PAT

9.11

19.02

-52%

Annualised EPS (from Q4)

0.54

1.42

-62%

Quarterly Results (Q4 FY26, Dec 2025 – Mar 2026):

Sales in Q4 were ₹252 Cr, down 19.2% YoY from ₹312 Cr in Q4 FY25. Operating profit (EBIT) fell to ₹14 Cr from ₹17.5 Cr. Net profit was ₹7.18 Cr vs. ₹11.63 Cr a year ago. The quarter accounts for roughly 38% of annual revenue—seasonality matters, and Q4 shipped the bulk.

Result Type: Yearly. Basis: Consolidated. Unit: ₹ Cr.

The sharp drop in FY26 revenue signals demand weakness. The company’s own concall guidance (Sep 2025) estimated revenue in the range of ₹895–₹920 Cr for FY26, citing early monsoon onset and retail inventory destocking in H1. Actual came in at ₹655 Cr—below guidance. Management attributed the miss to unusually poor monsoon timing, wholesale channel corrections, and retail demand softness.

PAT fell harder than revenue, implying cost absorption issues. Operating margin (EBITDA/Sales) was 5.6% in FY26 vs. 4.6% in FY25 on a trailing basis, but because revenue crashed, absolute EBITDA (Operating Profit before D&A) was lower. The company could not grow profit despite margin stability because the revenue base evaporated.

5. Valuation Discussion: Fair Value Range (Educational Only)

What follows is a walkthrough of how three valuation methods work, using this company’s numbers as the example — not a