Wakefit Innovations Ltd FY26: The ₹98 Crore Phantom Tax Credit and the 30% Mattress Cost Time-Bomb

At a Glance

Wakefit Innovations Limited delivered a record-setting top-line performance for the full financial year ended March 31, 2026, with revenue from operations scaling to an all-time high of ₹1,488.94 crore. This represents a 16.9% year-on-year expansion, driven primarily by a robust 49% acceleration in its retail and offline channels.

Beneath this headline growth, a complex architectural shift is taking place in the company’s structural profitability. For the full year, the company reported a Profit Before Tax (PBT) after exceptional items of ₹91.10 crore, reversing a loss of ₹35.00 crore in the previous fiscal. However, the final Profit After Tax (PAT) swelled disproportionately to ₹189.18 crore. This dramatic bottom-line spike was heavily amplified by a one-time non-cash deferred tax asset credit of ₹98.07 crore recognized in the final quarter under Ind AS 12.

Operationally, the business is battling severe near-term structural pressures. The final quarter of FY26 witnessed massive hyperinflation in crucial chemical inputs like polyol and TDI, with spot prices surging between 30% and 160%. Management responded by implementing a cumulative 15% price increase across March and April 2026. This aggressive pass-through presents immediate execution risks regarding volume elasticity and market-share defense against nimbler, lower-cost direct-to-consumer competitors.

A sharp divergence between accounting earnings and true operational cash metrics highlights the current period. While the full-year reported EBITDA surged to ₹181.96 crore, management’s internally tracked operational EBITDA—which strips out Ind AS 116 lease accounting smoothing effects, non-operating income, and employee stock option charges—sat at a much leaner ₹112.26 crore, representing a true operating margin of 7.5%.

The structural health of earnings depends entirely on capital efficiency rather than accounting adjustments. Investors must carefully monitor whether the company’s multi-category, asset-light physical store strategy can sustain its structural returns before older, lower-cost raw material inventories are entirely exhausted.

Introduction

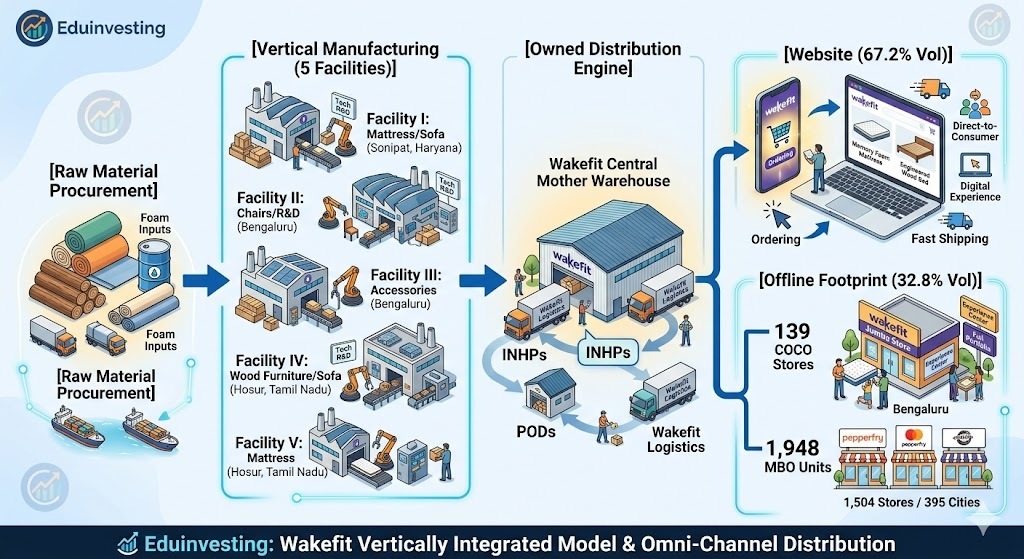

Wakefit Innovations Limited has spent the last decade executing a classic consumer pivot, successfully transitioning from a digital-first sleep shop into a sprawling, multi-channel home solutions brand. Founded in 2016, the company initially captured market share by cutting out intermediate supply chain layers to deliver compressed, roll-packed mattresses directly to consumer doorsteps.

The current fiscal year marks a major evolutionary transition for the firm following its public listing on December 12, 2025. Having raised ₹1,289 crore through its initial public offering—including a fresh issue component of ₹377 crore—Wakefit is aggressively shifting away from an exclusive reliance on third-party digital marketplaces.

The corporate objective has evolved from merely selling individual mattresses into building a centralized ecosystem capable of capturing a larger share of the Indian consumer’s home improvement wallet. The company is deploying capital to fund an expansive retail footprint across Tier 1 and Tier 2 cities while keeping its production engine consolidated within its manufacturing hubs across Karnataka, Tamil Nadu, and Haryana.

Business Model: WTF Do They Even Do?

At its core, Wakefit operates a full-stack, vertically integrated design-to-delivery model, which means they prefer owning the entire headache of the consumer value chain rather than outsourcing it. They control the engineering, prototyping, automated manufacturing, and final mile delivery of everything from memory foam slabs to engineered wood wardrobes.

The business relies on a multi-category product portfolio split into three distinct segments:

Mattresses: The legacy engine and margin anchor of the firm, accounting for 61.4% of total revenues in FY26.

Furniture: The physical scaling vehicle, contributing 29.3% of the top-line.

Furnishings & Décor: The long-tail accessory bucket, filling out the remaining 9.3%.

Wakefit splits its sales channels into “Owned Channels” (its proprietary website and company-owned, company-operated retail stores) and “External Channels” (third-party e-commerce marketplaces and multi-brand outlets). In FY26, owned channels climbed to 67.2% of total sales, up from 57.0% in FY25.

The strategic focus centers on using mattress sales as a low-cost customer acquisition tool, then utilizing cross-category recommendations to sell higher-ticket furniture items. This model works beautifully on paper, provided your input chemical costs do not behave like a speculative tech stock.

Financials Overview

Figures are consolidated, in ₹ crore.

Headline Performance

Metric

Latest Quarter (Q4FY26)

YoY

QoQ

Revenue

343.60

13.5%

-18.5%

EBITDA / Operating Profit

36.48

511.2%

-78.3%

PAT

121.75

Reversing Loss

280.5%

EPS (Reported)

3.69

Reversing Loss

280.4%

Did Management Walk the Talk?

During the post-IPO briefings late last year, management highlighted steady margin stabilization and non-disruptive offline store scaling. Looking closely at the full-year delivery, the business did hit its targeted top-line trajectory, clocking 16.9% annual revenue growth.

However, the late-quarter operational trajectory reveals distinct friction points. Management explicitly paused its retail store rollout around December 2025 to re-examine softening same-store sales growth (SSSG) and location metrics. This cautious approach directly contradicts the aggressive, uninterrupted rollout schedule initially detailed in their listing documentation.

Furthermore, while management previously downplayed the margin drag of competitive ad spend, Q4FY26 brand investments climbed to 7.3% of revenue, compressing operating margins down to 6.3% for the quarter.

What is Management Promising in the Coming Quarters?

Looking ahead into FY27, management is reiterating an aspirational annual top-line growth target of ~20%, though they carefully avoided issuing formal guidance. The operational focus is shifting to a major acceleration in physical retail, with plans to add more than 80 net new regular COCO stores over the next twelve months, specifically targeting underpenetrated Tier 2 territories.