Uravi Defence & Technology Ltd Q3 FY26: ₹10.20 Cr Sales, ₹0.33 Cr PAT, 94x P/E – From Bulbs to Bombs?

1. At a Glance – The Smallcap With Big Defence Dreams

Market cap of just ₹164 Cr. Current price ₹146. Stock down 67.9% in six months and 22.5% in three months. High of ₹588… now flirting with ₹143. That’s not volatility. That’s emotional damage.

Trailing 12-month EPS ₹1.54. P/E a majestic 94.2x. Industry median? Around 28x. Price to book 3.29x. ROE 4.99%. ROCE 7.33%. Debt ₹25.2 Cr. Interest coverage 2.66.

Latest quarter (Q3 FY26 – Dec 2025): Sales ₹10.20 Cr. PAT ₹0.33 Cr. EPS ₹0.29.

Yes, this is a ₹164 Cr company trading at 94x earnings while delivering quarterly profit of ₹33 lakh.

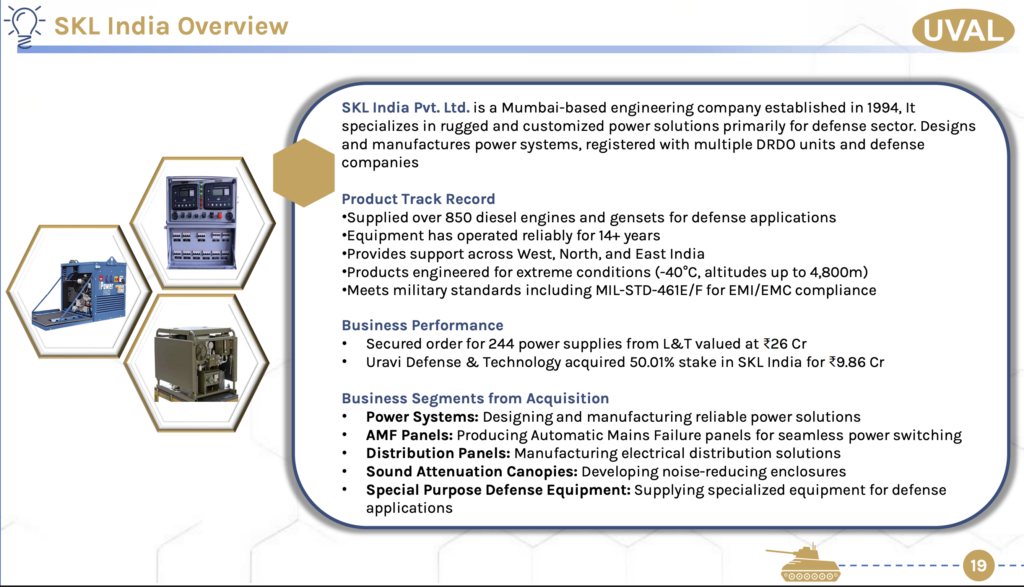

But wait — they’re not just selling bulbs anymore. They’re talking defence, DRDO vendors, UK acquisitions, and power systems for L&T.

Is this a lighting company trying to wear a camouflage jacket? Or is there actually a transformation underway?

Let’s switch on the light.

2. Introduction – The “From Halogen to Howitzer” Story

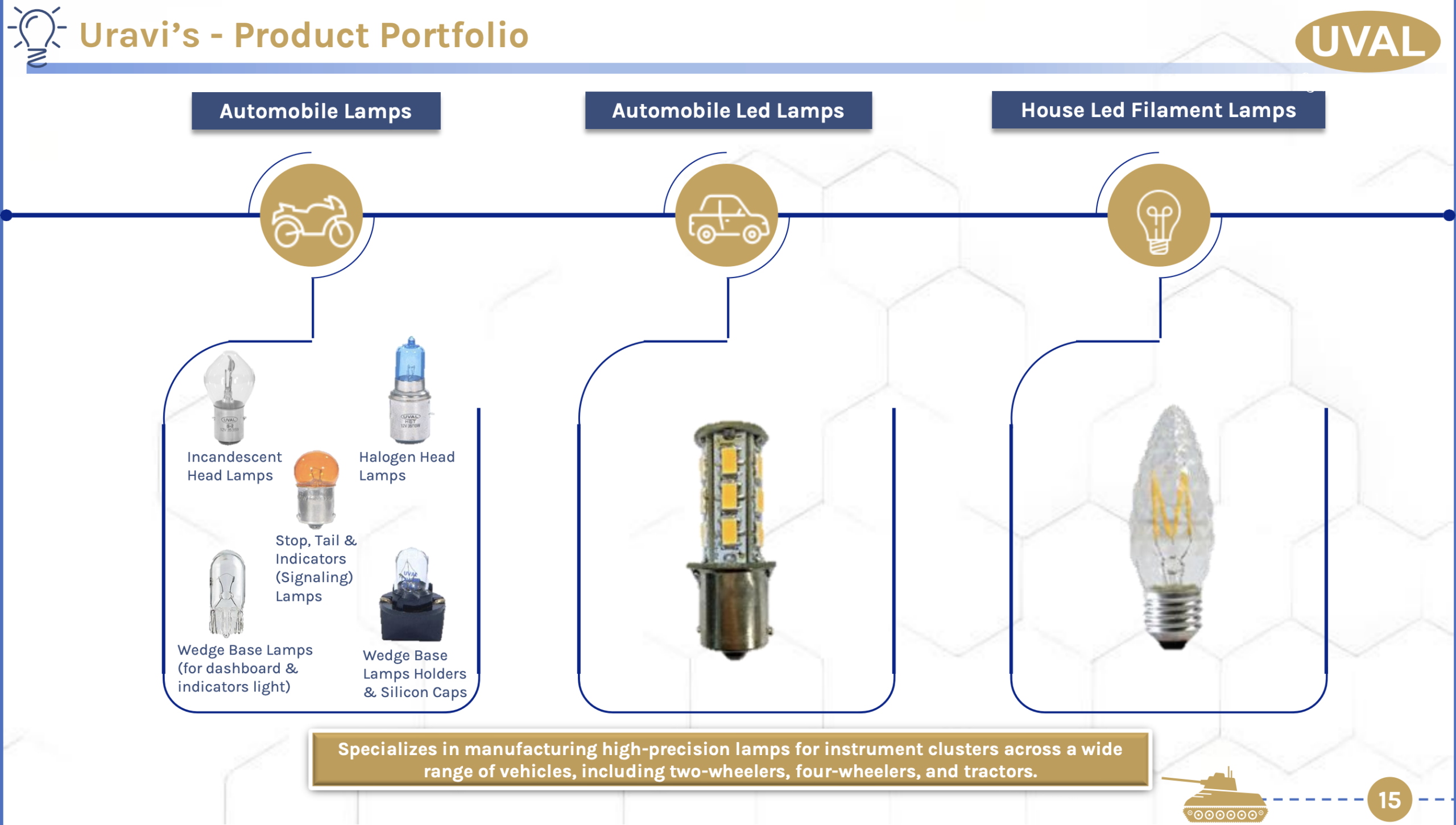

Once upon a time, Uravi was a simple automotive lamp manufacturer.