True Colors FY26: The Technicolor Dream with Monochromatic Cash Flow

Section 1 — At a Glance

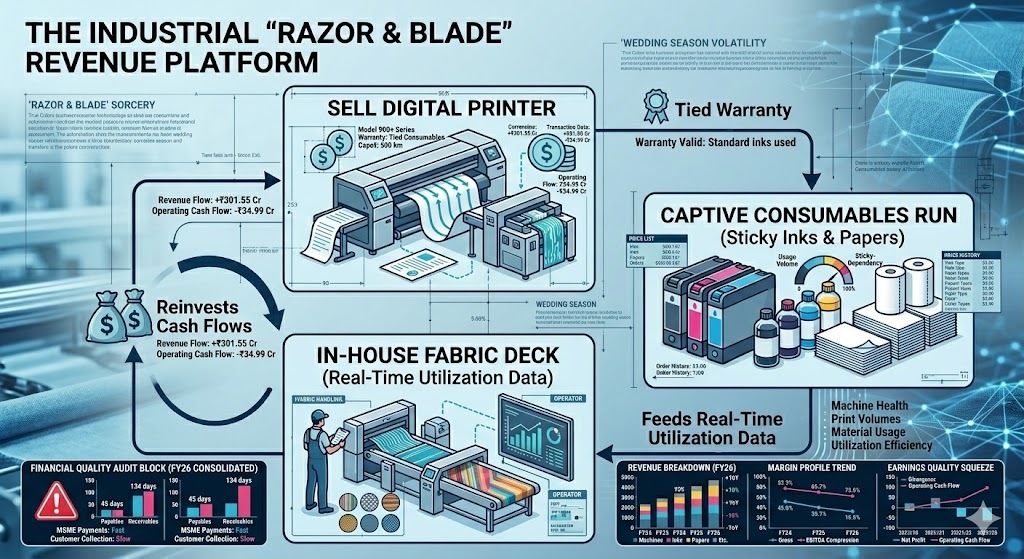

A sudden 155.19% explosion in machine sales revenue during FY26 has catapulted True Colors Limited into the visual center of India’s digital textile printing transition. Headline revenue scaled past the ₹301 crore milestone, clocking an impressive 29.22% year-on-year expansion. Yet beneath this vibrant exterior of top-line velocity and a widening field fleet of over 900 active digital printers lies a stark, less colorful financial paradox.

While reported net profit after tax surged to ₹31.16 crore, the company’s operating cash flow plummeted into deep negative territory, reversing from a positive ₹9.15 crore in the prior fiscal to an alarming negative ₹34.99 crore for the year ended March 31, 2026. This severe divergence exposes a critical operational bottleneck: a massive elongation in working capital cycles driven by an aggressive shift toward local vendor financing mandates and rigid upfront payment terms for imported premium consumables.

Revenue: ₹301.55 Cr (▲ 29.22% YoY) Net Profit: ₹31.16 Cr (▲ 28.60% YoY) Operating Cash Flow: -₹34.99 Cr (Severe Working Cap Drag)

The underlying quality of earnings has shifted materially as lower-margin transactional hardware deliveries momentarily outpaced high-margin recurring media lines, triggering a 194-basis-point compression in operating margins. In highly illiquid asset landscapes, explosive revenue growth unaccompanied by corresponding ledger collections is an open invitation to structural distress. Investors are left assessing whether the company’s ambitious forward integration into proprietary domestic chemical formulation will restore balance, or simply expand an already bloated collection pipeline.

Section 2 — Introduction

True Colors Limited, freshly minted on the public bourses following its September 2025 listing, operates in the sweet spot of specialized industrial automation. The company positions itself as an integrated, plug-and-play ecosystem orchestrator for micro, small, and medium enterprises making the multi-decade jump from slow, water-heavy traditional rotary screen printing to agile digital inkjet solutions. By establishing domestic production lines for specialized sublimation media alongside multi-brand hardware dealership agreements, the corporate playbook attempts to capture margin at multiple intervals of an operator’s daily production run.

Section 3 — Business Model: WTF Do They Even Do?

True Colors functions like an industrial razor-and-blade cartel, carefully disguised as a high-tech textile infrastructure partner. They sell multi-crore digital printing machines to textile mills, which is a fine transactional business. But the real corporate sorcery lies in their contract architecture: the hardware warranty is explicitly tied to the exclusive use of True Colors supplied inks. Swap their proprietary ink for a cheaper alternative from a rogue importer, and your multi-million-rupee printhead warranty vaporizes instantly.

If that contractual stranglehold isn’t enough, digital printing is fundamentally a make-to-order game where matching exact color profiles across repeated apparel runs is critical. Changing your ink formulation mid-season shifts the color tone just enough to turn a batch of festive garments into unsellable clearance stock. It is a beautiful operational trap. Once an operator buys a machine, they are effectively married to True Colors for their weekly ink and sublimation paper refills. The company even runs its own fabric job-work processing deck to utilize excess capacity and gather real-time data on localized fabric trends.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Headline Half-Yearly Trajectory

Metric

Latest Half (H2 FY26)

YoY (Same Half)

Previous Half (H1 FY26)

Revenue

150.43

6.86%

151.11

EBITDA

23.90

-28.10%

23.08

PAT

16.44

-24.13%

14.72

Reported EPS (₹)

7.54

-37.48%

7.76

Did Management Walk the Talk?

During their November 2025 investor briefing, management boldly guided toward a highly stable EBITDA margin corridor of 13% to 16%, emphasizing that “the 10% PAT margin threshold is now our standard baseline”. Reviewing the full-year closure of FY26, they technically kept their word—delivering a consolidated EBITDA margin of 15.58% and a PAT margin of 10.33%.

However, the sequential path to achieving these metrics tells a less steady story. H2 FY26 revenue effectively flattened out, down 0.45% compared to the first half of the year, while the segment mix shifted aggressively toward low-margin machine deliveries, forcing gross margins to swing violently by several hundred basis points between halves. Volatility in