1. At a Glance – The Quarter That Could Have Been ₹80 Crore

Thomas Scott India Ltd is currently sitting at a market cap of ₹435 Cr with a stock price of ₹296. In the last three months, the stock has corrected 10.7%. Over one year? Down 15.2%. But zoom out — three-year return stands at a muscular 94.3%.

Now let’s talk numbers that actually matter.

Q3 FY26 revenue came in at ₹66.25 Cr, up 45.93% YoY. PAT jumped 73.33% YoY to ₹4.97 Cr. OPM sits at 12.92%. ROCE is 20.4%. ROE is 16.4%. Debt to equity is just 0.21.

But here’s the masala: management claims a warehouse fire may have cost them 15–20% extra revenue. Meaning this could have been a ₹75–80 Cr quarter.

Own brand revenue surged 91% YoY in Q3. Contract manufacturing doubled.

And yet… receivables are bloated. Inventory is heavy. Promoter holding has fallen from 69% levels to 52%.

So the question is simple:

Is Thomas Scott a tech-enabled fashion rocket — or a fast-growing apparel business balancing on working capital steroids?

Let’s investigate.

2. Introduction – From Struggling Textile Kid to E-Commerce Fashion Nerd

Thomas Scott wasn’t always this glossy.

Go back a decade. Sales were under ₹20 Cr. Losses were normal. ROCE was negative. It looked like another small textile company trying to survive India’s brutal apparel market.

Then something changed.

Instead of competing in crowded physical retail, they went digital-first. Marketplace-focused. Data-driven.

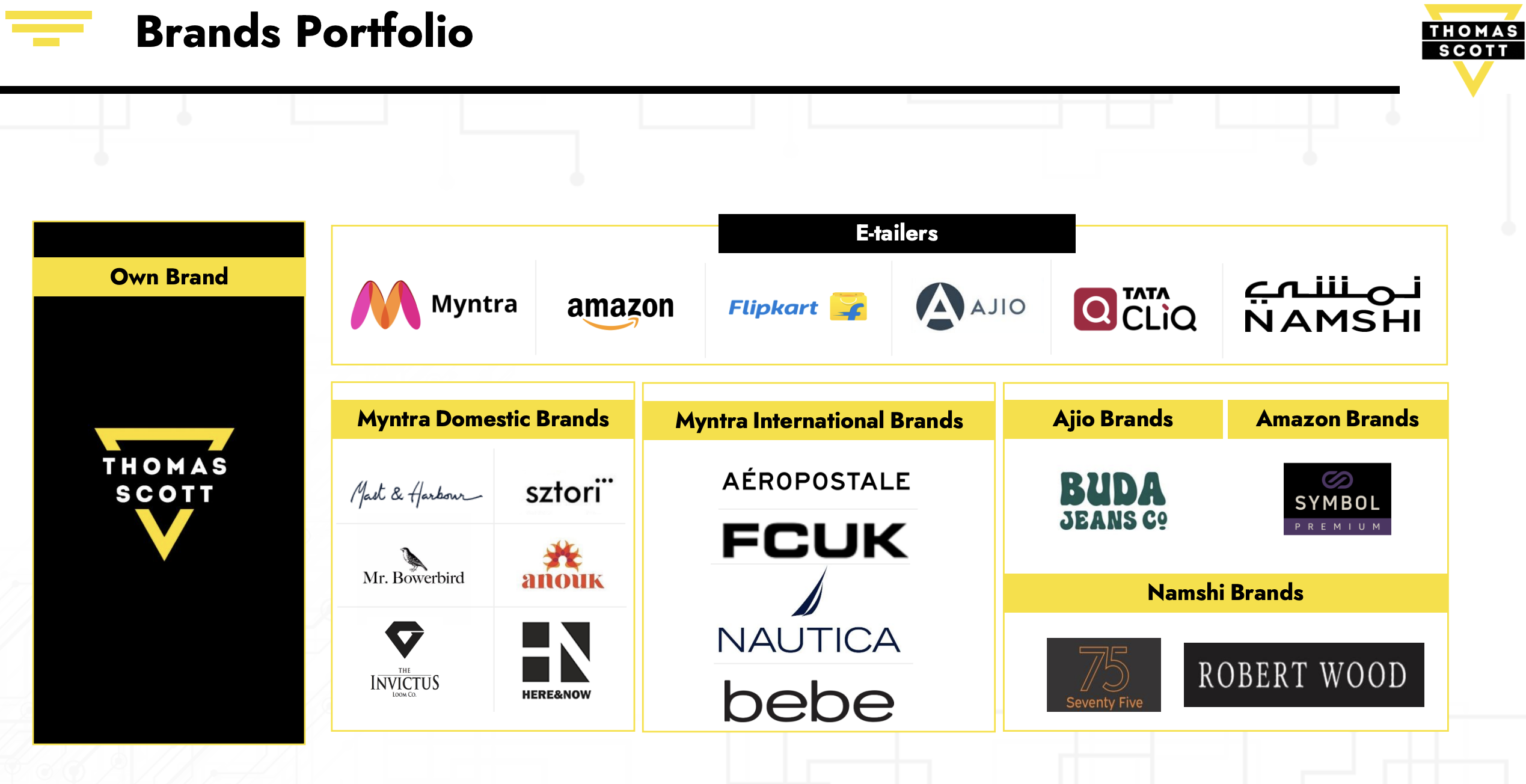

They built their business inside Myntra, Amazon, Flipkart, Ajio, Tata Cliq — basically inside your phone.

Today they operate 12+ brands and 22,000+ SKUs. In 9M FY26 alone, they referenced cumulative launches of 31,216 SKUs.

They describe themselves as a “technology-enabled fashion retailer.” And surprisingly, this isn’t just PPT jargon.

They built internal tools:

• thread.ai – GenAI fashion trend co-pilot

• catalog.ai – AI-powered visual & listing automation

Now here’s where it gets interesting.

They don’t bulk manufacture. They test. Small quantities. 100–120 units per style. Then scale only if it clicks.

That’s smart. That’s anti-inventory-risk.

But then… why is inventory still ₹77 Cr?

Hmm.

Are they masters of demand-driven scaling — or are marketplace accounting optics making things look better than reality?

Let’s decode the business model first.

3. Business Model – WTF Do They Even Do?

Imagine Zara had a smaller cousin who lived entirely inside Myntra and Amazon. That’s Thomas Scott.

They operate in three segments:

1) B2C – Own Brand (Thomas Scott)

Premium shirts, casual office wear, denims, winter wear. Target demographic: 25–40 years. Price points:

• Denims ~ ₹1,200

• Trousers ~ ₹1,200

• Shirts ₹800–1,000

They use high MRP + high discount positioning to access premium browsing pages. Classic marketplace hack.

2) B2C – Licensed & Other Brands

They handle brands like Mast & Harbour, Invictus, FCUK, Nautica, Bebe, Aeropostale, Symbol Premium and others across marketplaces.

They design, source, manufacture, distribute.

They are basically the backend muscle behind multiple digital labels.

3) Contract Manufacturing

Clients include Raymond, Max, Being Human, Shoppers Stop, Red Tape.

Capacity:

• Shirts: 60,000/month

• Bottoms: 60,000/month

• Bags: 20,000/month

• Daily fulfillment: 15,000 pieces

Now here’s the secret sauce.

High-width, low-depth strategy.

Instead of making 10,000