01 — At a Glance

The Company That Built Half of India’s Grid Now Wants to Build Its Data Centers Too

Techno Electric & Engineering Company Limited (TEECL) is doing what every forty-year-old EPC contractor secretly dreams of: going full digital transformation while still making money off the old business. Q3 FY26 smashed expectations with ₹872 crore in quarterly revenue (up 37% YoY), ₹119 crore in PAT (up 24%), and ₹13 in EPS. The company trades at 27.5x P/E (industry median: 15.1x), a 43% premium you’d normally avoid. But hold on—they’re not just renovating their EPC business. They’re simultaneously building data centres with ₹40 crore capex per megawatt, deploying 2.24 million smart metres, and guiding for ₹50 standalone EPS in FY26. Meanwhile, the order book hit ₹10,200 crore, up from ₹9,957 crore in September. Management is becoming selective, turning away business, and targeting ₹3,000–₹3,500 crore new order intake annually. This isn’t growth-at-all-costs. This is growth-with-discipline. Return in 3 months: +0.24%. Return in 6 months: -23.2%. Stock’s down 23%, valuations are elevated, but the transformation thesis is genuinely fascinating.

Opening Statement: Techno Electric just announced a fundamental transformation from pure-play EPC to digital infrastructure platform. Nine months FY26 revenue of ₹2,209 crore is already 90% of full FY25. They’re not in a hypergrowth phase—they’re in a pivot phase. The stock price hasn’t caught up yet.

02 — Introduction

From Substation Kings to Data Centre Dreams

Techno Electric has been building India’s electrical grid since 1985. Literally. More than 50% of India’s national grid substations? Theirs. Sixty percent of 400+ kV substations? Also theirs. For four decades, they were the disciplined EPC player—take the contract, deliver on time, collect the margin, move to the next project. No glamour. No drama. Just execution.

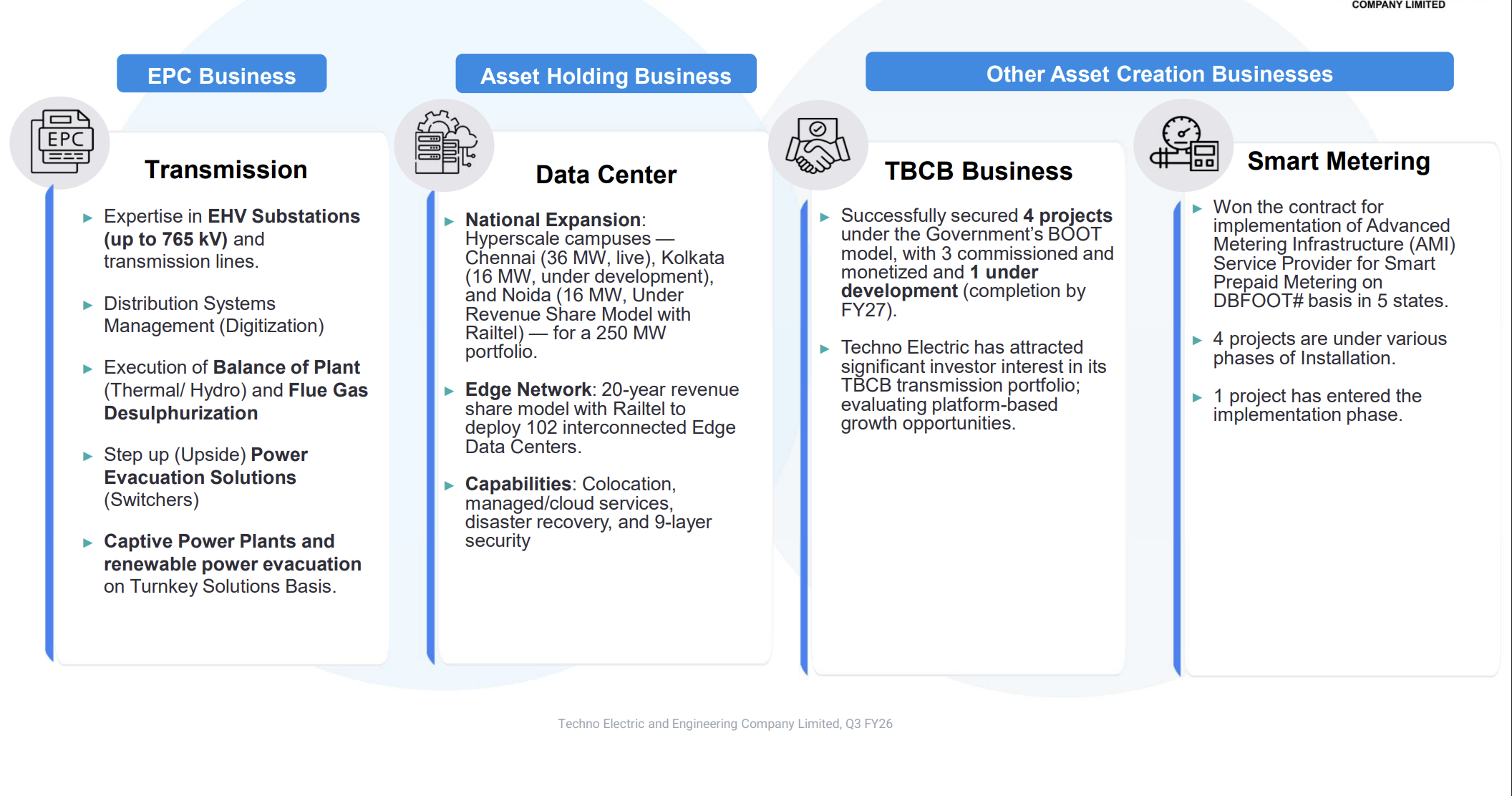

In December 2024, P.P. Gupta, the Chairman, went on the Q3 earnings call and basically said: “We’re done playing commodity EPC.” The company is now making strategic bets on data centres (36 MW in Chennai commissioned, 16 MW in Kolkata under construction, 100+ edge centres with RailTel), smart metering (2.24 million metres, O&M for 10 years), and network services (newly licensed in Chennai). The valuation stares back at you—27.5x P/E, a massive premium—but the transformation story is real. Management owns 56.9% of the company. Zero promoter pledge. ₹1,925 crore in cash. Near-zero debt. They’re basically giving themselves permission to take bets.

The biggest risk? Execution on data centres. The margins they’re guiding (14% EBITDA baseline, expanding with services) are compelling, but they’re new to this. The smart metres business is proven annuity income, but it’s also capital-intensive and dependent on state discoms paying on time. And the EPC business? Still the cash generator, but now they’re being deliberate about which orders they chase.

Concall Note (Feb 11, 2026): “We are leveraging our deep expertise in power sector to build high-value assets in data centers and smart metering. Our vision is to bridge the gap between traditional power infrastructure and the new digital economy.” — P.P. Gupta. Translation: We’re tired of selling labour and margin. We want to own assets and collect annuity cash flows.

03 — Business Model: WTF Do They Even Do?

Three Buckets. One Company. All Growing at Different Speeds.

Techno Electric now operates across three revenue streams, each with radically different unit economics.

Bucket 1: EPC Services (The Cash Cow). Engineering, Procurement, Construction for power infrastructure. In FY25, this was 99% of revenue. They design and build transmission substations (400 kV, 765 kV), FGD systems for thermal plants, smart metering installation, and one-off industrial projects. Order book is ₹10,200 crore. Margins are 13–15% EBITDA. Clients: Power Grid, NTPC, Adani, state utilities. Top five clients account for 56% of the order book. This is relationship-driven, execution-heavy, and cyclical. But it throws cash. FY25 operating CF was ₹453 crore.

Bucket 2: Data Centres (The Growth Story). They’re building and operating hyperscale data centres (Chennai: 36 MW, Kolkata: 16 MW) and edge data centres (100+ locations under a 30-year RailTel partnership). Chennai Phase 1 (6 MW) went live in September 2025 and is already operationally ready. PUE of 1.3 (industry-leading efficiency). Per MW capex: ₹40 crore. Revenue per MW: ₹8 crore for pure colocation, 3x that when you layer on bare metal and cloud services. Management expects ₹100+ crore revenue from data centre + edge business in FY27. By FY28–29, they believe digital infra will be the face of the company.

Bucket 3: Smart Metering (The Annuity Play). They install Advanced Metering Infrastructure (smart metres) for state distribution companies. 2.24 million metres on order (₹2,612 crore order value). Revenue comes as monthly grant + per-meter charges over 10 years, TOTEX model. EBITDA margins: ~20%. Capital investment to date: ₹1,000 crore. Total capex required: ₹1,500 crore. They’re 50% deployed. Indore and Ranchi complete by March–June 2026. Cash conversion takes years because cash flows are spread across 10-year concessions.

FY25 total revenue: ₹2,269 crore. EPC: ₹2,247 crore (99%). Other: ₹22 crore. By FY27–28? Management targets ₹300–₹400 crore from data centre alone. The mix is shifting. Not overnight. But shifting.

Strategic Inflection: EPC business will always be cash-generative. But data centres are where the ROI compounds. ₹40 crore capex per MW today; once operational, it generates ₹8–24 crore revenue per MW per year depending on service mix. Return profile is totally different—lower upfront margin, but 10+ year life, minimal capex replacement, and annuity predictability.

04 — Financials Overview: Q3 FY26

Nine Months Best in History. Q4 Expected to be Upside.

Continue reading with a premium membership.