Solar Industries India Ltd is the stock market equivalent of a Diwali rocket—bright, noisy, and a little overpriced. It makes mining explosives, grenades, propellants, and now drones. With a ₹1.27 lakh crore market cap and a P/E of 100, this “Nagpur-to-NASA” company is proof that investors will pay anything if you throw in words like “defence,” “rockets,” and “Modi Ji visit.”

2. Introduction

What happens when a mining-explosives company suddenly decides it can also make grenades, Pinaka rockets, and military drones? You get Solar Industries—the poster child of India’s “Make in India Defence” story.

This company is everywhere:

Blowing up rocks in Zambia.

Supplying propellants for ISRO rockets.

Delivering Pinaka systems to the Indian Army.

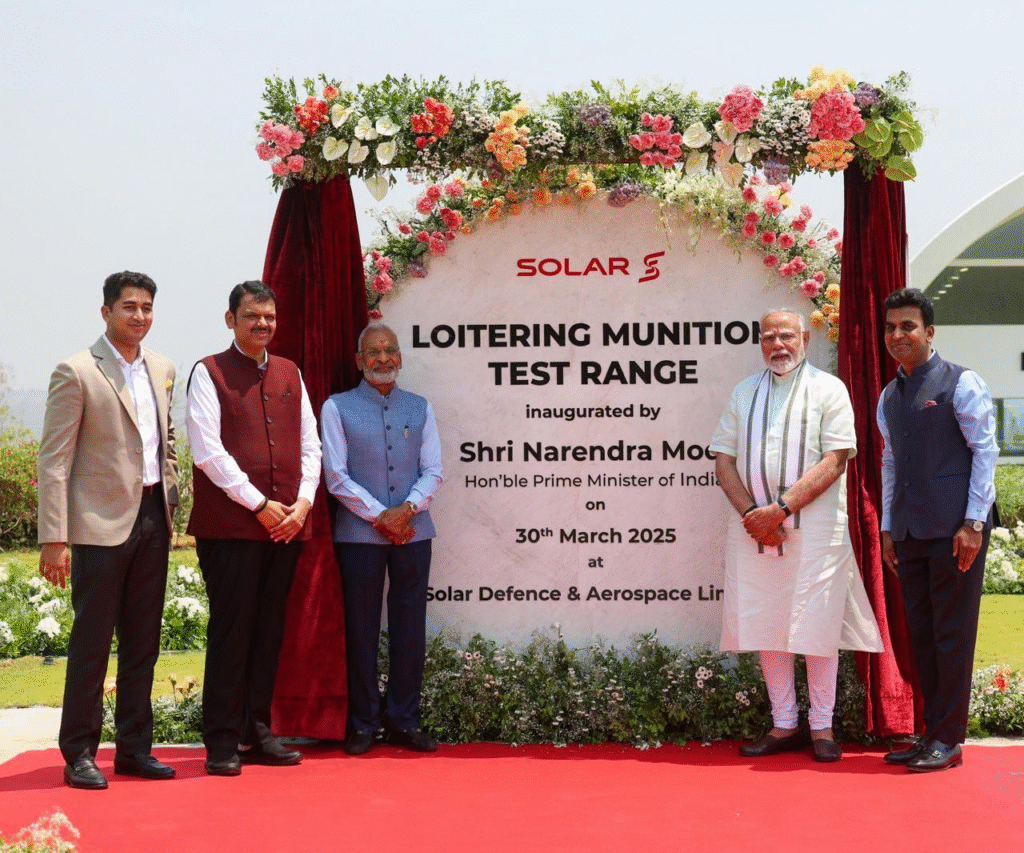

Pitching UAVs in Nagpur with a ₹12,700 Cr MoU.

The financials are equally explosive. Sales growth 28% CAGR over 5 years, profit growth 36% CAGR. ROE north of 30%. And yet, dividend yield is just 0.07%. Investors aren’t here for income—they’re here hoping for a “multibagger defence unicorn” story.

But the market is catching its breath: stock is down 16% in 3 months, because a P/E of 100 requires growth faster than ISRO’s Chandrayaan launch velocity.

3. Business Model – WTF Do They Even Do?

Let’s decode this fireworks factory:

Industrial Explosives (86%): Blasting coal, iron ore, highways, tunnels. Basically, making sure infrastructure projects don’t run out of dynamite.

Defence Products (14%): Hand grenades, mines, warheads, Pinaka rockets, propellants for Akash and BrahMos. The transition from “coal mines” to “land mines” is complete.

Global Exports (41%): 82+ countries, including subsidiaries in Turkey, Ghana, Nigeria, and even hyperinflationary Zimbabwe (where they had to restate numbers under Ind AS 29).

Question: How often do you see one company supplying both Coal India AND the Indian Army? That’s like Amul selling butter to both households and fighter jets.

4. Financials Overview

Quarterly Snapshot (₹ Cr)

Metric

Jun’25

Jun’24

Mar’25

YoY %

QoQ %

Revenue

2,154

1,685

2,167

27.9%

-0.6%

EBITDA

535

449

537

19.1%

-0.4%

PAT

339

301

346

12.6%

-2.0%

EPS (₹)

37.4

31.7

35.6

18.0%

5.1%

Commentary: Profits rising, margins at 25%+, but valuations already assume Solar will become India’s Lockheed Martin.

DCF: PAT ~₹1,300 Cr, growth 25%, discount 12%. Fair range = ₹9,000–₹11,000.

Fair Value Educational Range: ₹7,000–₹11,000 Disclaimer: This is for educational purposes only. Not investment advice. If you buy at ₹14,000 and it explodes, remember—it’s an explosives stock.

6. What’s Cooking – News, Triggers, Drama

Pinaka Boom: ₹6,084 Cr defence order—four years of revenue visibility and patriotic press coverage.

Nagpur MoU (₹12,700 Cr): Defence and Aerospace project—drones, counter-drones, and maybe aircraft. If even 50% materialises, it’s a blockbuster.

Export Orders: ₹2,150 Cr order in Feb 2025, plus multiple 200–400 Cr defence deals. Global customers trust Solar to deliver on time (and on blast).