1. At a Glance – The Plot Twist Nobody Saw Coming

SMT Engineering Ltd is currently trading at ₹375 with a market cap of ₹620 crore. In the last 3 months alone, the stock has delivered a jaw-dropping 207% return. Six months? 884%. From ₹9.75 low to ₹375 high. This is not a rally. This is a financial IPL season.

Latest Q3 FY26 consolidated revenue stands at ₹26.88 crore with PAT at ₹2.32 crore. Sales are up 7,164% YoY. Profit up 5,700% YoY. Read that again. Not 57%. Not 570%. Seventy-one hundred sixty-four percent.

Stock P/E: 47

Industry P/E: 30

Price to Book: 8.67

ROCE: 4.46%

Debt to Equity: 0.95

Promoter Holding: 67.44% (down 6.33% recently)

So what’s happening here?

Is this a genuine engineering turnaround story?

Or is this a corporate makeover where a small shell suddenly became a machinery giant?

Let’s investigate.

2. Introduction – From Mercantile To Machinery

SMT Engineering Ltd was incorporated in 1984. But until recently, it was known as Adarsh Mercantile Limited.

Yes. Mercantile.

And then suddenly in April 2025 — boom. Name changed to SMT Global Engineering Limited. Registered office shifted from West Bengal to Madhya Pradesh. Borrowing limits increased to ₹500 crore. Main object clause modified to include manufacturing machinery, foundry operations, steel processing, metal fabrication, pipe manufacturing, and basically everything short of launching rockets.

This isn’t diversification. This is identity transformation.

On March 26, 2025, the company acquired 100% of Sai Machine Tools Pvt Ltd by issuing 94,64,134 shares worth ₹27.45 crore. Same day, preferential allotment of ₹22.65 crore was done. Then an open offer at ₹42 per share happened in July 2025.

Today the stock trades at ₹375.

From ₹42 to ₹375 in under a year. That’s not compounding. That’s teleportation.

Question for you: when a company changes name, state, business model, and scale within one year — are you looking at a turnaround… or a rebirth?

Let’s go deeper.

3. Business Model – WTF Do They Even Do?

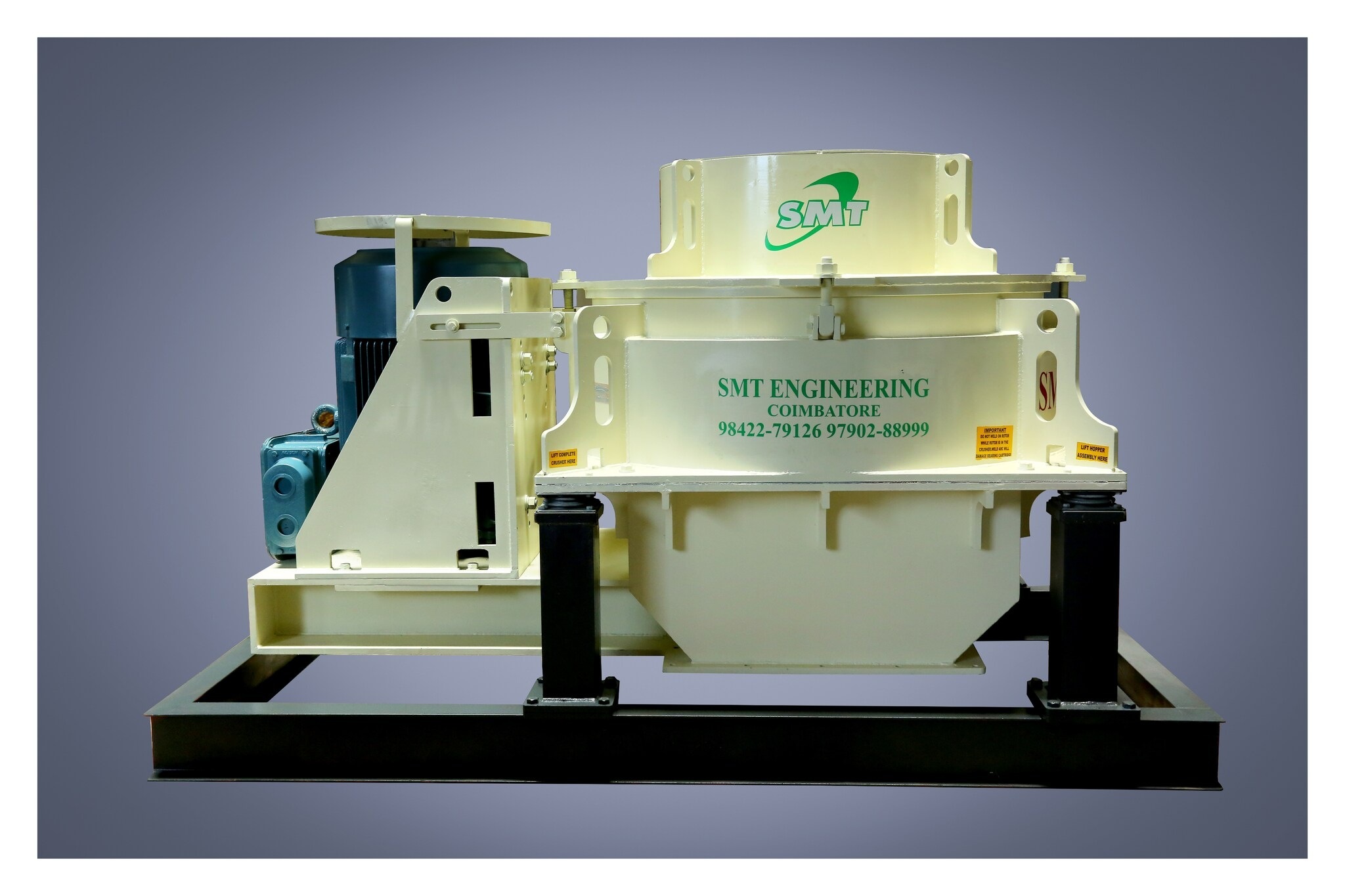

SMT specializes in plastic extrusion systems.

Translation: They manufacture machines that make plastic pipes.

HDPE pipe machines. PVC pipe machines. Drip irrigation machines. PPR, PEX, PE-AL-PE machines. Rain pipe machines. Vacuum cooling tanks. Pipe cutters. Pipe coilers.

Basically, if a pipe exists, they want to build the machine that builds it.

Their clientele includes Kisan, Signet, Prince Pipes, Supreme, Vectus, Mahindra EPC, Texmo and others.

So this is a B2B engineering equipment manufacturer serving irrigation, plumbing and industrial pipe manufacturers.

Sounds solid.

But remember — the financial explosion only started after March 2025 acquisition of Sai Machine Tools.

Before that?

Revenue was tiny.

Mar 2024 revenue: ₹3 crore

Mar 2025 revenue: ₹21 crore

TTM revenue: ₹108 crore

This is not organic growth. This is acquisition-driven consolidation.

Which brings us to the big question — how sustainable is this machine manufacturing business?

Are orders sticky? Are margins stable? Or is this project-based revenue that fluctuates like monsoon rainfall?

Let’s check numbers.

4. Financials Overview

EPS:

Q1 FY26: ₹1.42

Q2 FY26: