Shilpa Medicare FY26: A ₹1,549 Crore Pharmacy Pipeline Powered by Hope, Hype, and Heavy Lifting

Date of Publishing -

Spotted a factual error — a wrong number, date, or fact? Tell us and we will check the source.

For the last three years, watching Shilpa Medicare has felt less like evaluating a pharmaceutical firm and more like tracking a multi-billion-rupee urban infrastructure project. Investors have watched management pour vast sums into concrete, steel, and state-of-the-art bioreactors, all while waiting for the profits to match the ambition.

In FY26, the company finally delivered a visible financial pivot. Group revenues reached a historic ₹1,549 crore, representing an 18% year-on-year increase that comfortably outpaced industry growth. Operating leverage began to exert its mathematical influence as consolidated EBITDA rose 30% to ₹445 crore, pulling margins up to 29%.

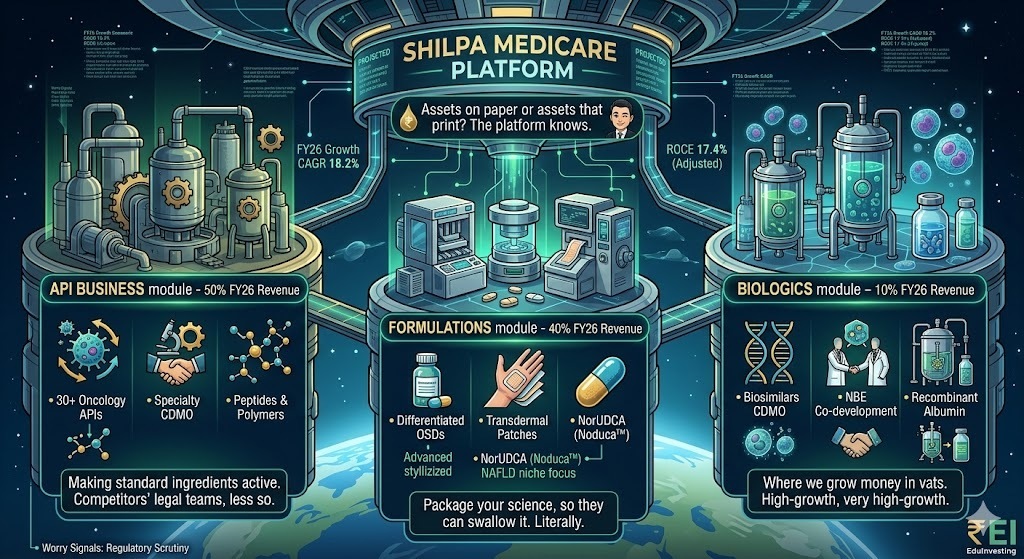

Beneath this operational acceleration, however, lies an intricately leveraged platform model. The company’s adjusted return on capital employed (ROCE)—calculated by excluding investments in long-gestation biologics and albumin—reached a strong 17.4%. Yet, the unadjusted, reported ROCE remains anchored at 11%, reflecting a balance sheet holding ₹884 crore of Capital Work-in-Progress (CWIP). This massive asset base represents a significant volume of unmonetized capital.

Furthermore, regulatory complexities continue to linger across the manufacturing footprint. Just hours before the annual book close, a USFDA inspection at the Unit VI facility in Bengaluru concluded with a Form 483 containing five procedural observations. Shilpa Medicare is currently functioning as a complex, multi-front scientific platform that has successfully demonstrated execution capability but remains exposed to stringent regulatory scrutiny.

Introduction

Shilpa Medicare Ltd, established in 1987 under the guidance of promoter Vishnukant Bhutada, has evolved from a conventional contract manufacturer into a highly specialized, vertically integrated developer of niche Active Pharmaceutical Ingredients (APIs) and advanced formulations. The company operates across a broad operational footprint that spans small molecules, oncology generics, novel drug delivery systems (NDDS), and complex biologics.

The organizational layout includes 10 regulatory-approved manufacturing and research facilities alongside a dedicated workforce of over 400 R&D specialists. Rather than competing directly in generic commodities, Shilpa has deliberately focused on high-barrier segments such as oncology treatments, transdermal patches, oral dissolving films, and antibody-drug conjugates (ADCs).

Business Model: WTF Do They Even Do?

To understand Shilpa Medicare, one must look past the standard definition of a generic drug company. The business operates as a sprawling, highly specialized scientific platform that attempts to span both small molecules and complex biologics simultaneously.

The small-molecule API segment remains the foundation of the organization, contributing 50% of total revenue. Within this space, the company manufactures more than 30 oncology APIs for global regulated markets, while running a specialty CDMO branch that handles advanced polymers and peptides.

The formulations division accounts for 40% of the revenue mix. Here, the strategy relies heavily on vertical integration, utilizing internal APIs to create oral solid dosages, injectables, and complex transdermal delivery systems.

The remaining 10% of the business resides within the biologics segment, operated through subsidiaries like Shilpa Biologicals. This division focuses on contract development for novel biological entities (NBEs) and the long-term development of recombinant human albumin, positioning the company across multiple distinct frontiers of pharmaceutical science.

Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4FY26)

YoY (%)

QoQ (%)

Full Year FY26

YoY (Full Year)

Revenue

439

30.0%

7.0%

1,549

18.2%

EBITDA

121

39.1%

5.2%

445

29.7%

PAT

85.4

147.8%

55.3%

233

165.0%

Reported EPS (₹)

5.51

290.8%

141.7%

12.44

211.0%

The full-year performance highlights a notable recovery in earnings quality. The expansion in EBITDA margins from 26% to 29% indicates that manufacturing volumes are beginning to cover the company’s fixed operating costs.

During the latest investor interactions, management emphasized that the financial turnaround is directly tied to improved asset utilization across the small-molecule blocks.

“We are transitioning from an intensive investment phase into a structural commercial phase,” noted the Managing Director. “As our differentiated product pipeline achieves global commercialization, operational leverage will naturally influence our return profile.”

Valuation Discussion

Shilpa Medicare’s capital structure consists of 19.6 crore outstanding equity shares. Based on the market close price of ₹499 on May 29, 2026, the company features a market capitalization of ₹9,759 crore and an enterprise value of ₹10,373 crore.