S P Apparels FY26: The ₹101 Crore Baby Clothes Empire Navigating a 30% US Tariff Trap

Section 1 — At a Glance

S P Apparels Limited concluded FY26 by navigating structural shifts in international trade policy, significant corporate acquisitions, and geographic capacity expansion. Consolidated revenue from operations for the full year reached ₹1,578.64 crore, representing a 13.2% year-on-year expansion from ₹1,395.13 crore in FY25. This growth was primarily sustained by the full-year integration of Young Brand Apparel Private Limited and incremental export volumes within the core garmenting division.

However, profitability metrics revealed structural compression during the final quarter of the fiscal year. Full-year consolidated profit after tax edged upward by 6.1%, closing at ₹100.95 crore compared to ₹95.10 crore in the preceding fiscal period. This single-digit bottom-line growth points to a sharp divergence from top-line performance, driven by a transition trough in Q4FY26. During this terminal quarter, consolidated sales experienced an 8.6% retraction to ₹364.91 crore, while quarterly net profit contracted by 38.8% to ₹18.59 crore.

This deceleration highlights the structural risk of geographic and client concentration, where the top three global retail customers anchor nearly half of total aggregate billing. Volatility in the US tariff framework during the fiscal year induced order hesitations, structural factory closures, and forced margin concessions to secure volume continuity. While short-term working capital efficiency showed material improvement—with the cash conversion cycle compressing significantly—the structural return on equity remains constrained at 11.2%. Strategic capital allocation over the coming fiscal periods must now absorb a multi-country machine footprint while transitioning from high-concentration infant wear to broader intimate and adult apparel segments.

Section 2 — Introduction

S P Apparels, founded in 1989 and anchored in the textile ecosystem of Tirupur, Tamil Nadu, operates as a vertically integrated manufacturer and exporter of knitted garments. The enterprise has historically positioned itself as one of India’s prominent specialized producers of infant and children’s wear—a segment traditionally insulated by high technical entry barriers, precise safety protocols, and low tolerance for structural defects.

The strategic architecture of the firm underwent a fundamental reconfiguration over the last 24 months. Through the complete acquisition of Young Brand Apparel Private Limited and structural operational expansions into Sri Lanka, management has attempted to transform a domestic export operation into a diversified multi-country manufacturing platform. This strategy aims to hedge trade-policy vulnerabilities across the US, UK, and European markets while expanding product capabilities into adult and intimate wear segments.

Section 3 — Business Model: WTF Do They Even Do?

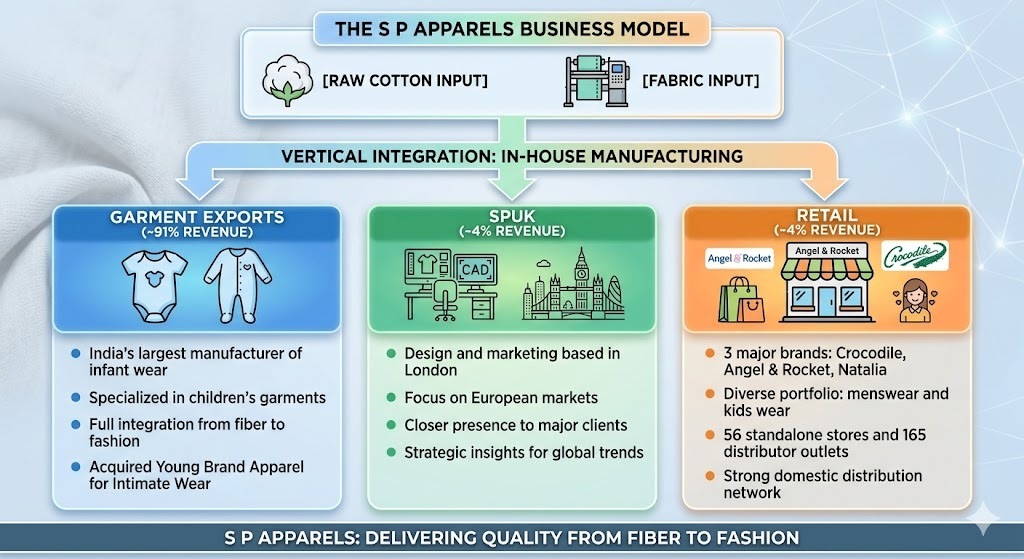

At its core, S P Apparels dresses global infants while attempting to survive the macro crosswinds of international trade agreements. The business model relies on absolute vertical integration: they ingest raw cotton and greige fabric at one end, run it through spinning, knitting, and automated embroidery lines in Tamil Nadu, and output baby bodysuits and sleepsuits at the other.

The revenue mix for 9MFY26 indicates that the Garment Export division—which includes the core operations, Young Brand Apparel, and Sri Lankan manufacturing—commands roughly 91% of the top line. The remainder is split equally between SPUK (a design and marketing office in London designed to look close to European clients) at 4% and a domestic Retail Division at 4% that manages brands like Crocodile and Angel & Rocket.

The underlying complication is extreme client concentration. The top three customers—marquee global labels like Marks & Spencer, Victoria’s Secret (PINK), and Jockey—historically account for 65% to 70% of absolute revenues. If an American or British retail buyer so much as sneezes due to local inventory gluts or tariff changes, S P Apparels is effectively forced to re-engineer its entire factory scheduling.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4FY26)

YoY (%)

QoQ (%)

Revenue

364.91

-8.59%

-4.72%

EBITDA / Operating Profit

44.64

-17.70%

1.45%

PAT

18.59

-38.83%

-2.16%

EPS (₹)

7.35

-39.26%

-2.12%

The financial trajectory for the quarter reflects an operational transition trough. The core garmenting division ran into a wall of US tariff ambiguity during the latter half of the year, leading to a temporary asset underutilization problem. Quarterly consolidated revenues shrank from ₹399.21 crore in Q4FY25 to ₹364.91 crore this quarter.

Divergences between headline top-line growth and quarterly margin preservation usually reveal a lack of pricing power under sudden regulatory or trade-policy shifts.

On the latest conference call, management noted that Q4 carried the maximum weight of this trade policy friction. In the words of the executive team, American buyers held back programs or aggressively renegotiated terms, leading to structural discounts to maintain customer continuity. The CEO noted that while “healthy re-engagement” has commenced following a newly